About 12 months ago I had reflected on a summer of global heat waves and how rising global temperatures would ultimately be inflationary as citizens and governments would be stressed in a multitude of ways to tackle heat waves, flooding, and health issues. But as it turns out there were other (not considered) ways that global warming might become an inflationary issue for countries.

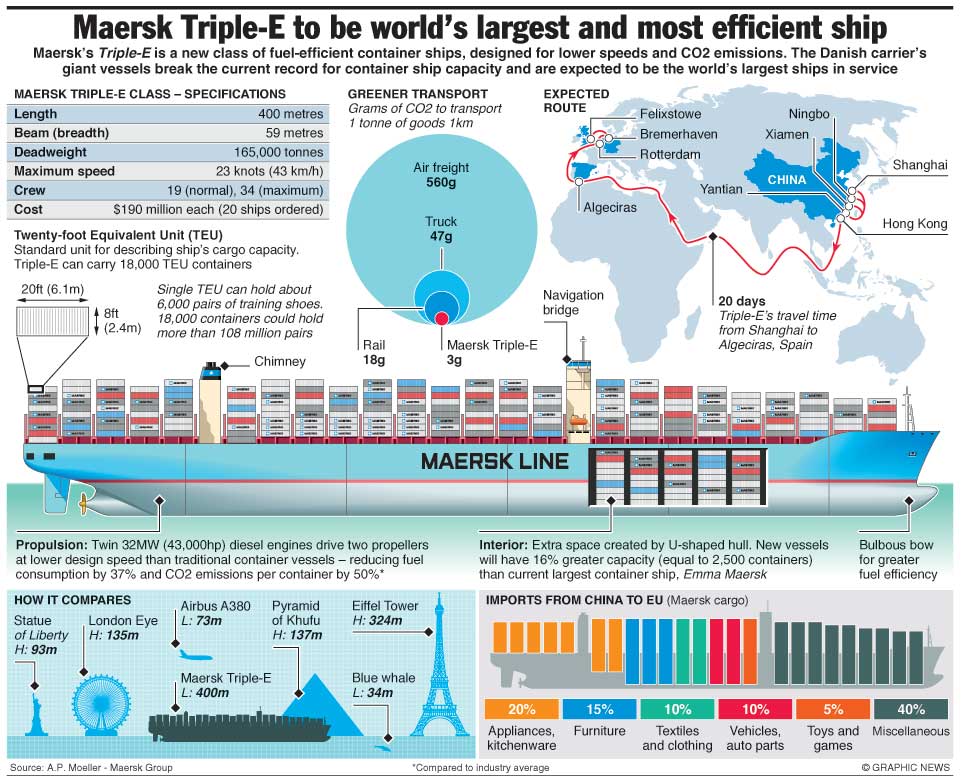

If you’ve never stopped to look into global shipping, you’re missing out on one of the most impressive global logistical challenges that has been tackled by human civilization. The ubiquity of cargo containers and the ships that move 90% of everything we use across oceans, renders both the novelty of this achievement and its impressiveness invisible. It wasn’t that long ago that shipping things (anything) was a cumbersome and wasteful endeavor where the distance something could be shipped, its speed in getting there, and the amount that would arrive unspoiled was a pitiful fraction of what travels today. The creation of standardized shipping containers and the development of ever larger ships to carry them has been a cornerstone of globalization.

But the speed of shipping is also dependent on two enormous infrastructure projects of significant historical importance; the Suez Canal and the Panama Canal. The histories of these mega projects are impressive and they retain essential roles in cutting down transportation times for ships crossing from one side of the planet to the other, speeding raw materials and finished goods to markets faster and for less money.

As I like to point out, most stories involving global warming are really stories about water. The Panama Canal, though it connects two oceans, is in fact a freshwater canal and relies on tributaries and rainfall to maintain its depth. But 2023 has delivered a serious drought to Panama and left tributaries and rivers dry, leading to a shallower draft in the Panama Canal. The managers of the canal have taken several measures to deal with this, the most notable has been reducing the draft limit of ships by six feet.

Six feet may not sound like a lot, but each foot reduced equates to a reduction of between 300 to 350 cargo containers per ship. Six feet is about 2000 fewer containers per boat, or around 25% of a typical cargo ship. This has meant that ships have to carry less cargo, or manufacturers are paying a premium to ensure their cargo is on an earlier scheduled ship. Other options include unloading and shipping some of the cargo by train and reloading it at another port, or travelling around the southern tip of South America, adding weeks to the voyage.

As if this wasn’t enough, lower water levels have also meant fewer ships allowed to transit the canal, with daily transits dropping from 40 to 36 to 32 trips a day, while fees for those crossings have risen to $400,000 per trip. For ships that have set travel times and book passage through the Panama Canal in advance, the impact of these changes has been less pronounced, but other types of shipping, like bulk and gas carriers that must wait for a slot in the canal are now waiting an average of 10 days (an increase of 280% since June) to make it through.

Inflation has many sources, but one we’ve been assumed would recede quite quickly was inflation due to infrastructure and shipping. Initially global supply chain stresses came from China, pandemic shutdowns, and backlogs. But time would ultimately fix these issues as China reopened and ports cleared the backlog of ships. The challenges of the Panama Canal show that climate change will likely remain a source of inflation, unanticipated and requiring considerable money to manage. Since water infrastructure is something that we typically underfund, there is almost no place, rich or poor, that isn’t looking at considerable future costs to improve and maintain existing infrastructure, let alone new infrastructure.

As we head into the winter, its very likely that the drought in Panama will ease, and shipping costs may come down while transportation times shorten. But this marks another change in the environment that may become a reoccurring pressure point on economies, and one that may become so regular as to recede into the background even while it impacts our daily lives. The lesson to investors should be that global warming remains inflationary and will demand ever more money for infrastructure.

Walker Wealth Management is a trade name of Aligned Capital Partners Inc. (ACPI)*

ACPI is regulated by the Investment Industry Regulatory Organization of Canada (www.iiroc.ca) and a Member of the Canadian Investor Protection Fund (www.cipf.ca). (Advisor Name) is registered to advise in (securities and/or mutual funds) to clients residing in (List Provinces).

This publication is for informational purposes only and shall not be construed to constitute any form of investment advice. The views expressed are those of the author and may not necessarily be those of ACPI. Opinions expressed are as of the date of this publication and are subject to change without notice and information has been compiled from sources believed to be reliable. This publication has been prepared for general circulation and without regard to the individual financial circumstances and objectives of persons who receive it. You should not act or rely on the information without seeking the advice of the appropriate professional.

Investment products are provided by ACPI and include, but are not limited to, mutual funds, stocks, and bonds. Non-securities related business includes, without limitation, fee-based financial planning services; estate and tax planning; tax return preparation services; advising in or selling any type of insurance product; any type of mortgage service. Accordingly, ACPI is not providing and does not supervise any of the above noted activities and you should not rely on ACPI for any review of any non-securities services provided by Adrian Walker.

Any investment products and services referred to herein are only available to investors in certain jurisdictions where they may be legally offered and to certain investors who are qualified according to the laws of the applicable jurisdiction. The information contained does not constitute an offer or solicitation to buy or sell any product or service. 16 Past performance is not indicative of future performance, future returns are not guaranteed, and a loss of principal may occur. Content may not be reproduced or copied by any means without the prior consent of the author and ACPI.