I wish to inform you about an exciting new profession, currently accepting applicants. Accurate recession prognostication and divination is an up and coming new business that is surging in these turbulent economic times! And now is your chance to get in on the ground floor of this amazing opportunity!

I wish to inform you about an exciting new profession, currently accepting applicants. Accurate recession prognostication and divination is an up and coming new business that is surging in these turbulent economic times! And now is your chance to get in on the ground floor of this amazing opportunity!

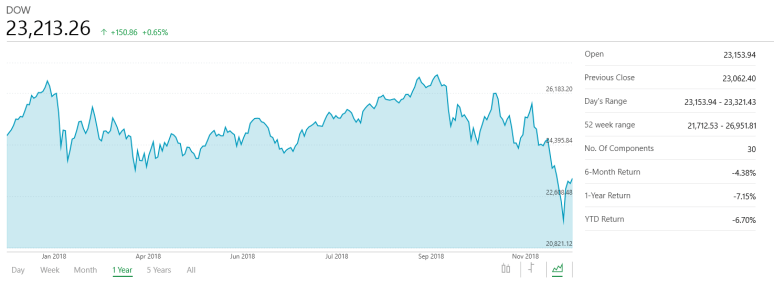

I am of course being facetious, but my satire is not without precedent. As 2018 has devolved into global market chaos, finally losing the US markets in October, experts have been marshalled to tell investors why they are wrong about markets and why they should be more bullish.

Specifically analysts and various other media friendly talking heads have been trying to convey to the general public that the negative market sentiment that has driven returns down is misplaced, and have pointed to various computer screens and certain charts as proof that the economy is quite healthy and that in this moment we are not facing an imminent recession. Market returns through the final quarter of 2018 indicate this message has yet to find fertile ground among the wider public.

While these experts, analysts and financial reporter types may not be wrong, indeed the data they point to has some real merit, I don’t think that investors are wrong to heavily discount their advice. For the wider investing audience, being right 100% of the time is not a useful benchmark to strive towards with investments ear-marked for retirement. Instead a smarter approach is to be mindful about risks that can be ill-afforded. Investment specific risk, like that of an individual stock may be up to an investor (how much do I wish to potentially lose?). On the other hand, a global recession that is indiscriminate in the assets that suffer may be more risk than an investor can stomach.

The experts have therefore made two critical errors. The first is assuming that what is undermining investor confidence is an insufficient understanding of economic data. The second is that there is a history, any history, of market analysts, economists and journalists making accurate predictions of recessions before they happen.

This last point is of particular importance. While I began this article with some weak humor on prognostication and divination, it’s worth noting that predicting recessions has a failure rate slightly higher than your local psychic and lottery numbers. That so many people can be brought forth on such short notice to offer confident predictions about the state of world with no shame is possibly the worst element of modern investment culture that has not been reformed by the events of 2008.

This doesn’t mean that investors should automatically flee the market, listen to their first doubt or react to their gut instincts. Instead this is a reminder that for the media to be useful it must think about what investors need (guidance and smart advice) and not more promotion of headline grabbing prognostication. The markets ARE down, and this reflects many realities, including economic concerns, geopolitical concerns and a host of other factors outside of an individual’s control. It is not a question of whether markets are right or wrong in this assessment, but whether good paths remain open to those depending on market returns.