Since 2008 governments the world over have tried to fight the biggest banking collapse since the great depression with modest success. Eight years on and you would be loath to say that the world has turned a corner, ushering in a return of unrestrained economic growth.

Since 2008 governments the world over have tried to fight the biggest banking collapse since the great depression with modest success. Eight years on and you would be loath to say that the world has turned a corner, ushering in a return of unrestrained economic growth.

Why this is the case is a question not just unanswered by the average layman, but by experts as well. Huge amounts of money have been printed, financial institutions have been patched and repaired, interest rates are at all time lows, what more can be done to fix the underlying problems?

It turns out that nobody is really sure, but as we begin 2016 global markets are reeling on the news that the Chinese economy has even greater problems than previously thought. Only a few days into the week and most markets are down in excess of 2-3%, giving rise to concerns that a Chinese led global recession could be on it’s way.

The difference between now and 2008 is that much of the resources used to try and stem the problems from nearly a decade ago have already been deployed, and there is little left in the tank for another round. Central bakers have been trying to get enough inflation into the system to raise interest rates up from “emergency” levels to something more “normal” but outside of the US this seems to have largely failed.

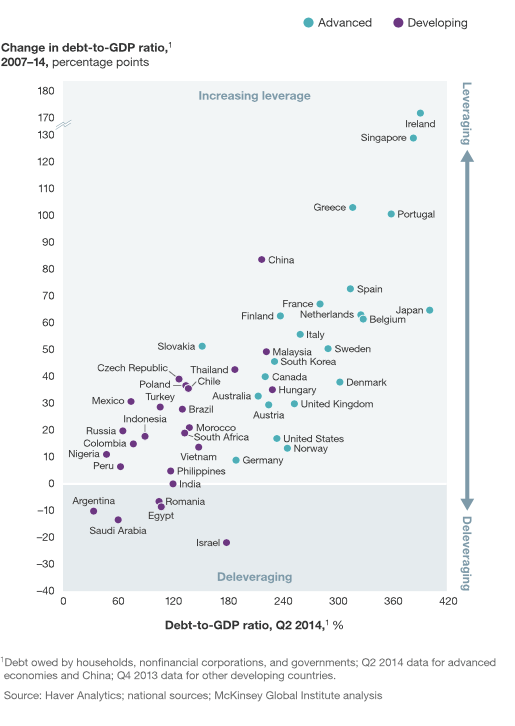

One of the saving graces after 2008 was that the Emerging Markets were seemingly unaffected. In fact, since 2008 the developing world has become more than 50% of global GDP but in that time the rot that often accompanies success has also set in. EM debt is now considerable, putting many countries that had once extremely healthy balance sheets heavily into the red. Borrowing by these nations has increasingly moved away from constructive economic development and more into topping up civil servants and passing on treats to voters.

For some, myself included, it has been encouraging that the Chinese have not proven to be the economic übermensch that some had feared. The rise of the state directed economy with boundless growth had many people concerned that China might represent an economic nadir for the planet. To see it every bit as bloated, foolish and corrupt may not be good for markets, but at least takes the bloom off the rose about Chinese economic supremacy.

Still, this all of this leads to a couple of frightening conclusions. One is that we have yet to come across any rapid comprehensive solution to a global financial crisis like 2008 that can undo the damage and return us to an expected economic prosperity. The second is that we may have been going down the wrong path to resolve the economic problems we face.

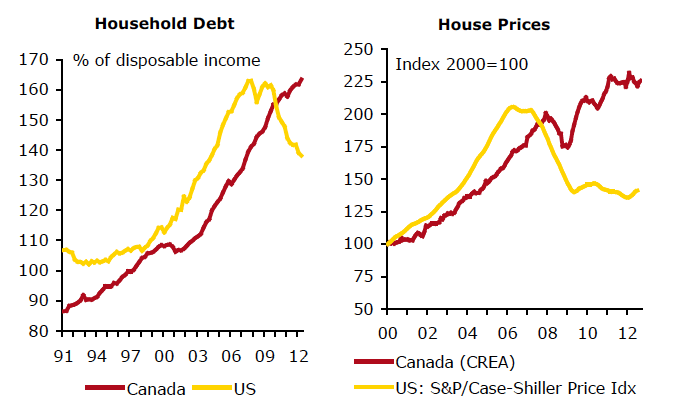

If debt was the driving force behind 2008, you couldn’t argue we’ve done much to alleviate the problem. At best we have merely shifted who holds it. In the United States, the US government took on billions of dollars of debt to stabilize the system. In Europe, despite attempts to reduce balance sheets across the continent, every country has taken on more debt as a result, regardless of whether they are having a strong market recovery, or a weak one. In Canada, arguably one of the worst offenders, private debt and public debt have ballooned at a frightening pace with little to show for it. Rate cuts and government spending are no match it seems for a plummeting oil price and a lack lustre manufacturing sector.

Having faced the problem of restrictive debt, putting much of the world’s financial markets in grave danger, our response has been to simply acquire more. Greece owes more, Canada owes more, and now the Emerging markets owe more. It was as though while trying to right the economic ship we forgot that we should keep bailing out the water.

None of this is to say that every decision since 2008 has been wrong. Following Keynesian policy saved countless jobs and businesses. But at some point we should have also expected to tighten our belts and dispose of some of the debt weighing us down. Instead central banks attempted to stimulate inflation by juicing the consumer economy with incredibly low interest rates. But as we have seen there is only so much that can be done. A combination of persistent deflation, an aging population and extensive debt have largely upended the best efforts to restart the economy on all cylinders.

This shouldn’t be a surprise. Debt makes us financially fragile. It is an obligation and burden on our future selves. But if we found ourselves drowning in debt eight years ago, it is curious we thought the solution would be to add rocks to our pockets and expect to make the swimming easier.