*From Adrian: I began writing this on the weekend when I first learned of the conditions of the retirement residence in Dorval. Since then it has been revealed that nearly 50% of COVID-19 deaths in Canada are in long term care facilities. You can read more about that here from The Globe And Mail: Outbreak at senior’s homes linked…

Canada’s demographic story is neither unique nor surprising. Like many other nations (most nations in fact) its largest demographic is rapidly aging and requiring an increasing number of services in both health care and assisted/retirement living. Like many other nations its only population growth is through immigration as people have largely stopped having enough kids to grow the next generation. It is a slow moving story, but also an inevitable one.

This is both well known and uncontroversial. Long before John Ibbitson and Darrell Bricker had written Empty Planet, before Hans Rosling was using a clever moving chart at TED Talks to explain population trends, Canadian professor David K. Foot had written his book Boom Bust and Echo, detailing the future of the Canadian population. Finally those predictions are starting to be realised, and investors like myself are eagerly looking for ways to capitalize on an enormous demographic change.

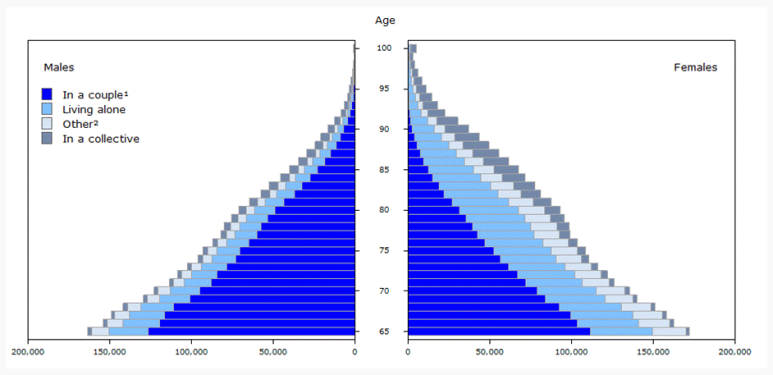

One such way will be in Senior’s Residences, Assisted Living and Long Term Care Facilities. With Canadians living longer Statistics Canada points out that 7.1% of Canadians over 65 live in “collective dwellings” like retirement residences, a number that jumps to 31.1% for people 85 and older. That number holds true when we look at special care facilities, with 29.6% of people 85 and over.

The logic is appealing and direct. In 2016 16.9% of Canadian were 65 or older, and 2.2% were 85 or older. That was a 20% increase since 2011. With more Canadians approaching 65 and 85 than ever before the need for retirement residences, assisted living and long term care facilities will be greater than ever. Given the time it takes to secure and build new facilities, resistance at local levels to having them built and the high costs of creating and managing these businesses plus the government oversight, the business is as close to a sure thing that investors could hope to find. How could this go wrong?

I’ve been writing about demographics for a while. Here are some of the other things I’ve had to say:

Enter 2020, a year that continues to feel like being slapped in the face by a large fish. Investors are accustomed to thinking very little about the business practices and oversight of the companies they invest in, but perhaps that should change, especially when they invest directly. Scandals, abuse and personal harm are matters for owners, and owners, even if removed from the daily running of a business should remain engaged. This remains especially true if the business deals in the wellness of people.

To my point, behold the unfolding scandal at a privately run senior’s residence in Montreal. I apologize at how graphic these details are and if you are at all squeamish please feel free to jump to the next paragraph. When health officials were finally called into the residence it was described as a “concentration camp”. Some residents had fallen on the floor and been left there. Others hadn’t been fed. Two people were found dead in their beds and hadn’t been recognized as such. Reportedly there were only two orderlies for the entire 134 bed facility. Some patients were so dehydrated they were unable to speak. Patients had been left in diapers, unchanged for several days. One in triple diapers with feces leaking out. These details are beyond horrific and have no place in a story about a Canadian senior’s residence. In total there had been 31 deaths over the previous few weeks.

As an investor, what should you think about such a discovery? Beyond its horror show details, more suited to a zombie apocalypse movie than real life, how should a lone investor think about their role in this?

One thing to consider is that due diligence should begin to increase the more certain an investment looks. Businesses with very high barriers to entry (the ease or difficulty of getting involved in a sector of the market), that are part of effective oligopolies or are essential services are not “set it and forget it” services. If anything the risk of abuse, neglect or corruption is higher the more essential and irreplaceable the businesses becomes. For the average person at home this may not be a feasible or realistic thing to do, and an individual investor may not be in a position to attend annual general meetings, or even be aware of how to solicit and get answers from corporate boards.

This is one reason to consider using a mutual fund, or an investment that functions like a mutual fund that dedicates energy to analyzing and understanding businesses. It is also a reason for investors working with a financial advisor to ask questions about the nature of the investments they are buying, especially if they seem like “no lose” scenarios. If something makes intuitive sense to do, we should be clear as to why more aren’t doing it. Lastly, if you are investing in a private investment sold through an offering memorandum you should make sure someone is paying close attention to the details. There will always be blind corners in businesses, things you can not know, but you should have comfort that someone is providing verifiable oversight.

An aging population creates new investment opportunities, and senior’s living will be one of them. A business that’s cash rich and necessary, the appeal is obvious. But businesses that are responsible for providing care and looking after people’s well being also have the pull to maximize their profits, squeezing returns wherever they can. That push and pull should sit on everyone’s mind as they consider the new opportunities coming into focus.

Information in this commentary is for informational purposes only and not meant to be personalized investment advice. The content has been prepared by Adrian Walker from sources believed to be accurate. The opinions expressed are of the author and do not necessarily represent those of ACPI.