Hey, millennials, which socialist nation is about to implode? Did you guess Venezuela? Because its Venezuela.

For those less in the know about what is happening to Venezuela, the country is nearing a total economic collapse, brought about by a decade and a half of total mismanagement by an old-school socialist dictator entirely in keeping with the historical context of South America.

Once hailed as a hero by such famous radicals as author Tariq Ali and professional curmudgeon Naom Chomsky, Hugo Chavez was the ideal socialist leader for a number of people who would never have to live under his dictatorial reign. Chavez nationalized oil companies and provided extensive programs for Venezuela’s extensive poor. But more than a decade on, and three years following his death Venezuela’s luck has seemingly run out.

Chavez’s hand picked replacement, President Nicolás Maduro, has kept on with Chavez’s well established tradition of blaming all of his nation’s problems on the United States since he took office in 2013. But the reality is that Venezuela has been a victim of it’s own poor planning and it’s outcome entirely predictable.

Having made the cornerstone of it’s economy the export of oil, the nation has suffered greatly for three reasons. First, Dutch Disease, or the result of a rising value of a domestic currency as a result of selling an extensive natural resource. Put simply, nations that sell a lot of oil tend to have a petro-currency, which makes domestic manufacturing less competitive on the global stage.

Second, cronyism; Chavez was old school in his commitment to creating a personality cult around him. Positioning himself as the savior of the poor he did many things to try and improve the lives (and earn the love) of Venezuela’s many impoverished people. But in the course of that he also removed anyone who might be his opposition. From the standpoint of the management of Venezuela’s oil reserves it has meant poor production and no new investment. Oil production fell 25% in the time Chavez ran the country.

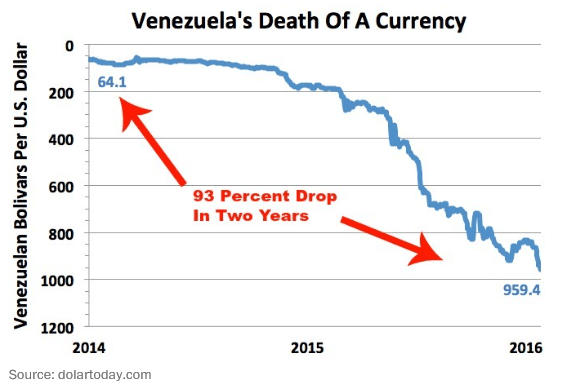

The last reason is of course the price of oil. As oil prices fell the fragility of the economic system made itself obvious. Today Venezuela is broke and the look of total economic collapse is depressing and scary. Inflation is out of control. Some estimates say inflation will hit 189% this year, while the IMF thinks it will be 720%. To fight the growing poverty, which is now 76% and up from 55% in 1998, the government has hiked the minimum wage by 30%; the twelfth such hike since President Nicolás Maduro took office. Real wages fell last year by 35% and their currency has lost over 90% of its value in two years.

The people of Venezuela now face a frightening prospect that any economic recovery will be decades away, and that the policies followed by their socialist government have made them an outlier from the largely positive trends that have been improving life across many developing nations. But this is not about hypothetical future problems, but current issues. There is no food in Venezuela, no toilet paper, no basic necessities and no prospect for reversing course. In January this year the government told people they would have to begin producing their own food, a follow-up from governments telling farmers that they would have to sell their food to the government at pre-determined prices.

Unsurprisingly, none of this bodes well for Venezuela’s population. Violence is a real potential and people are wondering when (or if) Maduro will step down, and whether a government change can occur without violence. So far he has resisted and despite the recent loss of congressional elections he still holds sway over the judiciary and economic appointments. In fact his current economic czar doesn’t believe in inflation. No really.

All this leads to some disquieting truths, most important of which is that economic realities catch up to everyone. Since the fall of the Soviet Union and the so called “End of History” there has been a growing warmness to socialism by a generation who has never experienced it. Venezuela is a good reminder that bad economic policies are always bad, and the economic challenges we all face, be it poverty, damaging wealth inequliaty, globalised manufacturing or predatory banking do not resolve themselves magically with a flip of the switch and friendly socialist rhetoric. Instead those problems must be solved within the system, not by destroying it.