Since 2008 (that evergreen financial milestone) central banks have tried to stimulate economies by keeping borrowing rates extremely low. The idea was that people and corporations would be encouraged to borrow and spend money since the cost of that borrowing would be so cheap. This would eventually stimulate the economy through growth, help people get back to work and ultimately lead to inflation as shortages of workers began to demand more salary and there was less “slack” in the economy.

Such a policy only makes sense so long as you know when to turn it off, the sign of which has been an elusive 2% inflation target. Despite historically low borrowing rates inflation has remained subdued. Even with falling unemployment numbers and solid economic growth inflation has remained finicky. The reasons for this vary. In some instances statistics like low unemployment don’t capture people who have dropped out of the employment market, but decide to return after a prolonged absence. In other instances wage inflation has stayed low, with well-paying manufacturing jobs being replaced by full-time retail jobs. The economy grows, and people are employed, but earnings remain below their previous highs.

Recently this seems to have started to change. In 2017 the Federal Reserve in the United States (the Fed) and the Bank of Canada (BoC) both raised rates. And while at the beginning of this year the Fed didn’t raise rates, expectations are that a rate hike is still in the works. In fact the recent (and historic) market drops were prompted by fears that inflation numbers were rising faster than anticipated and that interest rates might have to rise much more quickly than previously thought. Raising rates is thought to slow the amount of money coursing through the economy and thus slow economic growth and subsequently inflation. But what is inflation? How is it measured?

One key metric for inflation is the CPI, or Consumer Price Index. That index tracks changes in the price or around 80,000 goods in a “basket”. The goods represent 180 categories and fall into 8 major groupings. CPI is complicated by Core CPI, which is like the CPI but excludes things like mortgage rates, food and gas prices. This is because those categories are subject to more short-term price fluctuation and can make the entire statistic seem more volatile than it really is.

Armed with that info you might feel like the whole project makes sense. In reality, there are lots of questions about inflation that should concern every Canadian. Consider the associated chart from the American Enterprise Institute. Between 1996 – 2016 prices on things like TVs, Cellphones and household furniture all dropped in price. By comparison education, childcare, food, and housing all rose in price. In the case of education, the price was dramatic.

Armed with that info you might feel like the whole project makes sense. In reality, there are lots of questions about inflation that should concern every Canadian. Consider the associated chart from the American Enterprise Institute. Between 1996 – 2016 prices on things like TVs, Cellphones and household furniture all dropped in price. By comparison education, childcare, food, and housing all rose in price. In the case of education, the price was dramatic.

Canada’s much discussed but seemingly impervious housing bubble shows a similar story. The price of housing vs income and compared to rent has ballooned in Canada dramatically between 1990 to 2015, while the 2008 crash radically readjusted the US market in that space.

The chart below, from Scotiabank Economics, shows the rising cost of childcare and housekeeping services in just the past few years, with Ontario outpacing the rest of the country in terms of year over year change when it comes to such costs.

My desktop is littered with charts such as these, charts that tell more precise stories about the nature of the broader statistics that we hear about. Overall one story repeatedly stands out, and that is that inflation rate may be low, but in all the ways you would count it, it continues to rise.

In Ontario the price of food is more expensive, gas is more expensive and houses (and now rents) are also fantastically more expensive. To say that inflation has been low is to miss a larger point about the direction of prices that matter in our daily lives. The essentials have gotten a lot more expensive. TVs, refrigerators and vacuum cleaners are all cheaper. This represents a misalignment between how the economy functions and how we live.

In Ontario the price of food is more expensive, gas is more expensive and houses (and now rents) are also fantastically more expensive. To say that inflation has been low is to miss a larger point about the direction of prices that matter in our daily lives. The essentials have gotten a lot more expensive. TVs, refrigerators and vacuum cleaners are all cheaper. This represents a misalignment between how the economy functions and how we live.

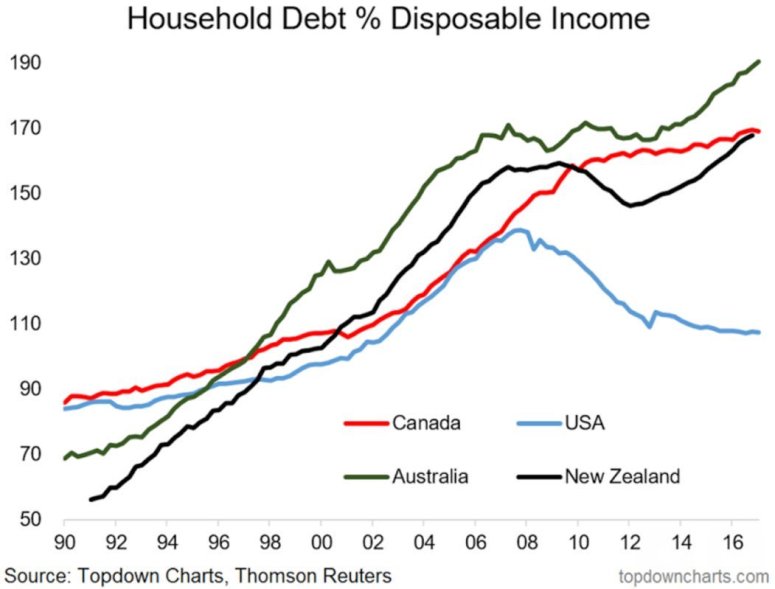

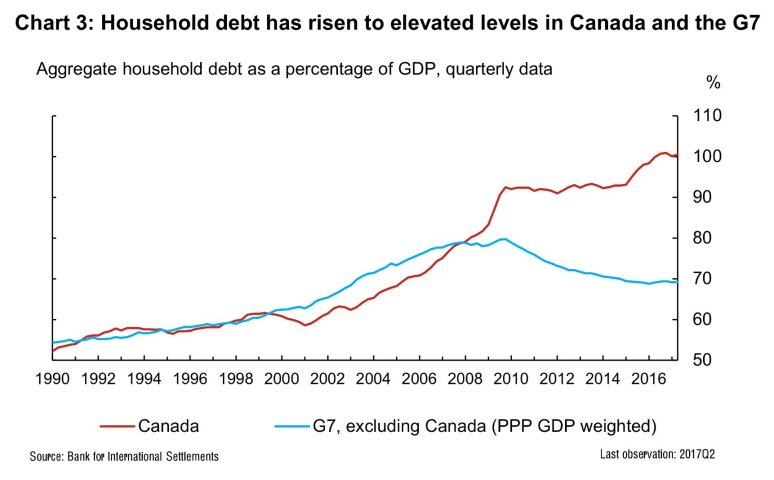

Economic data should be meaningful if it is to be counted as useful. A survey done by BMO Global Asset Management found that more and more Canadians were dipping into their RRSPs. The number one reason was for home buying at 27%, but 64% of respondents had used their RRSPs to pay for emergencies, for living expenses or to pay off debt. These numbers dovetail nicely with the growth in household debt, primarily revolving around mortgages and HELOCs, that make Canadians some of the most indebted people on the planet.

Economic data should be meaningful if it is to be counted as useful. A survey done by BMO Global Asset Management found that more and more Canadians were dipping into their RRSPs. The number one reason was for home buying at 27%, but 64% of respondents had used their RRSPs to pay for emergencies, for living expenses or to pay off debt. These numbers dovetail nicely with the growth in household debt, primarily revolving around mortgages and HELOCs, that make Canadians some of the most indebted people on the planet.

In the past few years, we have repeatedly looked at several stories whose glacial pace can sometimes obscure the reality of the situation. But people seem to know that costs are rising precisely in ways that make life harder in ways that we define as meaningful. When we look at healthcare, education, retirement, and housing it’s perhaps time that central banks and governments adopt a different lens when it comes understanding the economy.