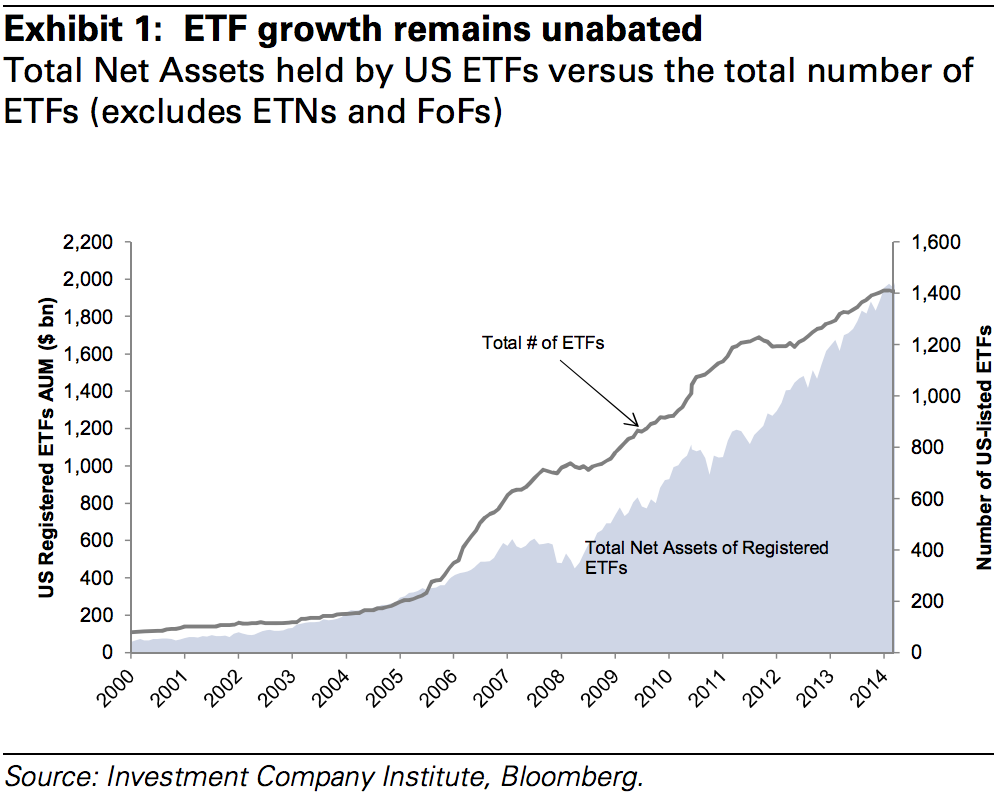

Over the past few years, the growing chorus from the media about Exchange Traded Funds (ETFs) and their necessity within a portfolio has approached a near deafeining volume. In case you’ve forgotten, ETFs are the low cost investment strategy – frequently referred to as passive investments – that mimic indices, providing both the maximum up- and down-sides of the market.

I continue to harbour my doubts about the attractiveness of such investments, though I do use them from time-to-time when the situation calls for it. On the whole, though, I find it interesting that Canadian investors have been reluctant to walk away from their mutual funds, despite the assurance by talking heads that costs are too high and that ETFs are more attractive.

This isn’t the first time that Canadians have been encouraged to broaden their investment horizons and adopt “better” vehicles for their money. Hedge funds were once an investment option for only the most wealthy, but eventually they found their way into the mainstream of investment solutions. The result was a flood of new money, which made some star managers household names, extensively broadened their investment reach and lined their pockets. The industry, once a niche, became far more commonplace. And why wouldn’t Canadians want a slice of an investment strategy that promised to be able to make money regardless of the market conditions? There has been a regular supply of managers promising to short stocks, juggle derivatives, and leverage cash to deliver positive returns regardless what was transpiring in the world. All of them (or almost; I will assume that there were some lucky ones) have fallen decidedly short. Canadians were largely let down by the last “big thing”.

The appeal of investments that are not mutual funds is understandable. Mutual funds are boring, and ubiquitous. Canadians have a lot of them, and almost without exception they make up the majority of any average portfolio. The workaday nature of these investments gives people the nagging feeling that the wealthiest among us very likely have something different, something better than what can be bought at any bank or offered by any financial advisor.

In some respects, this is true: more money does, in fact, open doors to different investment opportunities. However, people might be surprised at how small a percentage they make of any portfolio, even those that belong to the wealthiest 0.01% of Canadians, and before seeking to participate in these, we should be mindful of the lessons associated with the broadening hedge fund market. For the last three years, hedge funds have been badly underperforming in Canada, well out of line with either mutual funds or indexes. The reasons for this are not immediately obvious, as hedge fund managers offer many explanations as to their lacking performance while giving a mix of investment bombast and optimistic views about “next year.”

One idea, floated back in 2013, was that hedge funds were good because they were smaller, when money was limited but opportunities seemed abundant. As more money has poured into the hedge fund world, that balance has shifted. Now there is too much money and the opportunities are too sparse. This is an explanation that I think has merit, but will unlikely be echoed by the proprietors of such products.

ETFs, of course, are a different animal altogether and are therefore unlikely to befall the same existing fate of hedge funds and their rock star managers. But the ease and cost effectiveness of these funds has inspired a slew of new products that either invest in smaller, more volatile markets, or are so complicated that they cannot be properly understood, and thereby expose investors to risk they may not be prepared for.

A colleague of mine described the coverage in the press as being one of “getting all the facts right and still drawing the wrong conclusion”. Canadians don’t continue to stick with Mutual funds because they are oblivious to higher costs, but because volatility and the fear of loss is of much greater concern and poses a bigger set of risks for investors than the cost of their holdings. And while it is true that, over time, ETFs may perform slightly better than actively managed funds, most of us cannot afford to be approaching our investments on a decade-by-decade level. In bad markets people are loath to sit back and simply “wait it out” as their portfolio value continues to drop without alternative. As a result, this “passive investment” strategy, while seemingly attractive, is not realistically an appropriate alternative to the traditional “active management” strategy of mutual funds, which provide an opportunity to deal with risk and keep people invested – which, to my mind, is what truly counts for long term success.

{kind=link}