Many of you won’t know this, but my father used to sky dive. He’d stopped by the time I was born (reportedly because my mom had a natural aversion to life threatening hobbies) but in many ways his hobby would be a reoccurring source of guidance for life lessons.

For instance, whenever I was nervous about doing some BIG THING, my dad would let me know that once you were doing THE BIG THING, your anxiety would drop considerably. Sky divers know this, as they are only nervous until they jump out of the plane, and then get very calm. The fear is in the anticipation, not the actual doing.

2016 had a lot of anticipation, but not an actual lot of doing. Brexit happened, but hasn’t really happened. Donald Trump has been elected, but hasn’t been sworn in. The Canadian housing market continued its horrific upward trend and news stories began to abound about the looming robot job-pocalypse. 2016 was full of anticipation, but little action.

2017 will begin to rectify some of these issues. Next week we will see the arrival of President Donald Twitterbot™, finally ending speculation about what kind of president Donald Trump will be and seeing what he actually does. So far markets have been reasonably calm in the face of the enormous uncertainty that Trump represents, but his pro-business posture seems to have got traders eager for a more unregulated market with greater earnings for the future. Right now bets are that Trump might really jump start the economy, but there are real questions as to what that might mean. Unemployment is already very low and inflation looks like it is actually beginning to creep up. Housing prices (amazingly) are back to 2007 levels and the economy seems to be moving into the later stages of a growth cycle.

2017 will begin to rectify some of these issues. Next week we will see the arrival of President Donald Twitterbot™, finally ending speculation about what kind of president Donald Trump will be and seeing what he actually does. So far markets have been reasonably calm in the face of the enormous uncertainty that Trump represents, but his pro-business posture seems to have got traders eager for a more unregulated market with greater earnings for the future. Right now bets are that Trump might really jump start the economy, but there are real questions as to what that might mean. Unemployment is already very low and inflation looks like it is actually beginning to creep up. Housing prices (amazingly) are back to 2007 levels and the economy seems to be moving into the later stages of a growth cycle.

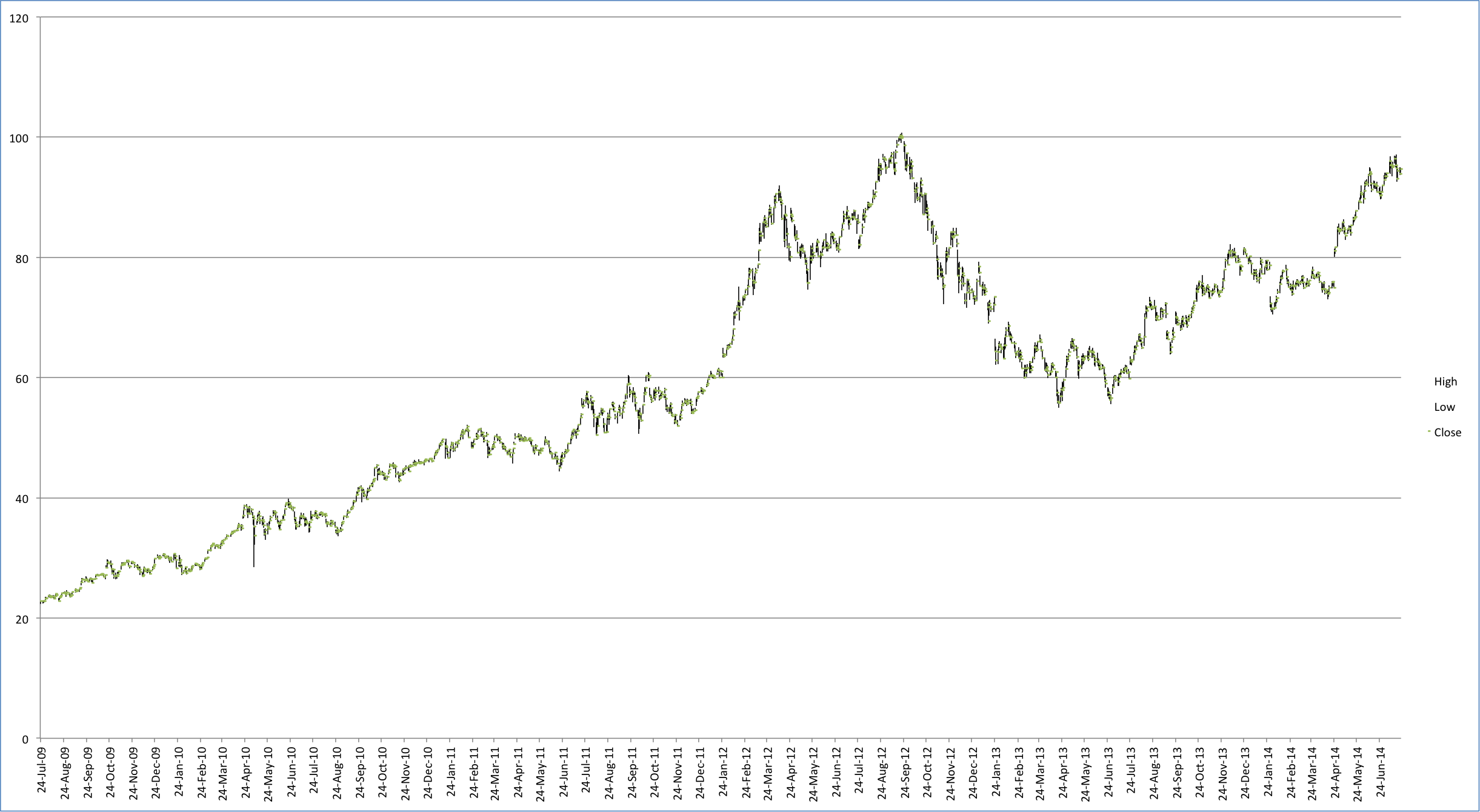

2017 will likely not be the year that the Canadian housing bubble/debt situation comes crashing down, but its also unlikely to be the year that the situation improves. Economically the short term outlook for Canada is already kind of bad. The oil patch is already running second to a more robust energy story from the United States. Canadian financials had a very healthy year last year, but as we’ve previously written while the TSX was the best returning developed market over 2016, in a longer view it has only recently caught up with its previous high from 2014.

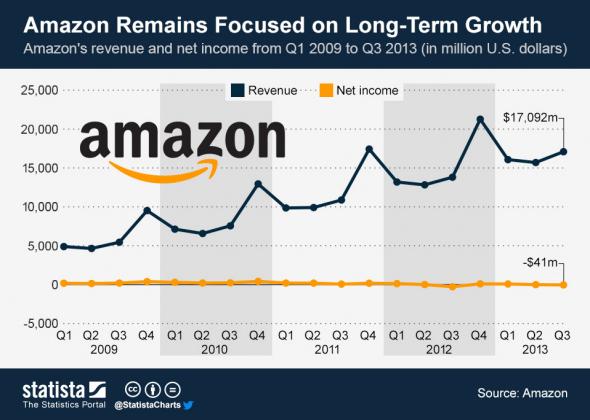

2017 may be the year that automation starts being a real issue in the economy. Already much of Donald Trump’s anger towards globalisation is being challenged by analysis that shows its not Mexico that steals jobs, but robots. But as robots continue to be more adept at handling more complicated tasks there is simply less need for humans to do much of that work. Case in point is Amazon’s new store Amazon Go, currently being opened in Seattle.

While many point to this as Amazon’s foray into the world of groceries (and a better shopping experience) Amazon’s real business is in supply management. The algorithms they use and the new technology they’ve developed are not designed to be one offs, but ways to handle high volumes of business traffic with as few people, and as low a cost as possible. Combined with driverless cars (currently being tested in multiple cities & countries)and our growing app economy, we will be pushing more people out of steady work across multiple sectors of the economy in coming years.

2017 will also be the year that Brexit will begin, though it will be two years before it is complete. Many people will be watching on how Teresa May’s government handles the Brexit negotiations, how confident England looks on its position, and how hostile or open Europe seems to be to conceding to Britain’s views. Either way it should provide lots of turbulence as it unfolds over the coming years.

But despite all this, there is a kind of calm in the markets. We’ve crossed the line on these issues and there’s nothing to do but continue ahead. Trump will be President Donald Twitterbot™, Brexit will happen, regardless of how many people remain opposed and markets will either go up or down as a response. Perhaps the new normal is a great deal more similar to the old normal than we all thought.

Then again…

That’s just its phone division. The iPad, whose sales numbers are definitely plateauing if not declining is still a valuable business netting $5.9 billion in revenues, greater than Facebook, Twitter, Yahoo, Groupon, and Tesla combined.

That’s just its phone division. The iPad, whose sales numbers are definitely plateauing if not declining is still a valuable business netting $5.9 billion in revenues, greater than Facebook, Twitter, Yahoo, Groupon, and Tesla combined.