While I rarely get the chance to watch late night TV anymore, I’m sure there will be a few segments on The Daily Show and Colbert Report about “inversion” – the process by which American companies buy another foreign firm and relocate their head-office there to avoid paying taxes, over the next couple of days.

The arrival yesterday of the Burger King/Tim Horton’s deal has a number of lawmakers and journalists screaming about lack of loyalty, tax dodging and America’s uncompetitive corporate tax rate. But being quick to anger isn’t the smartest way to understand why one company might wish to purchase another and pull up stakes.

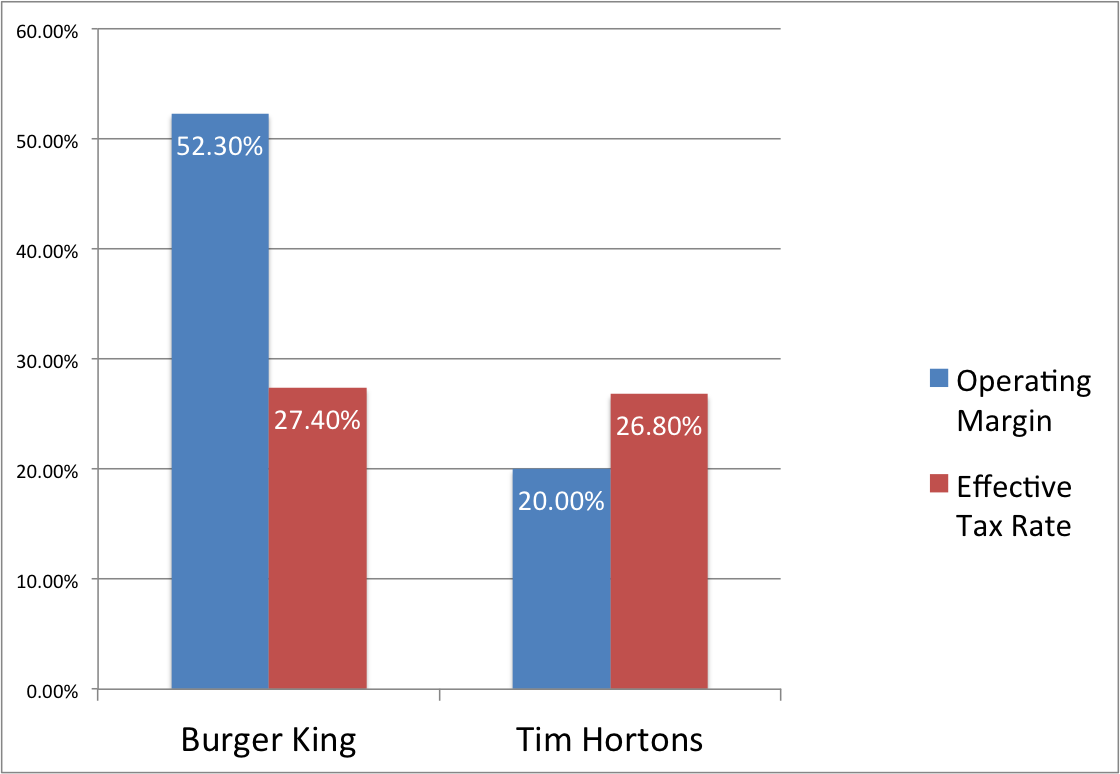

For instance, despite claims that Burger King intends to avoid substantial taxes in the United States in favour of Canada’s more moderate tax rate isn’t actually that true. As reported this morning by the Financial Times, the two companies both pay a very similar effective tax rate, literally only points apart from each other. So relocating a company like Burger King may indeed yield some benefits in taxation, but likely so small as to not make the deal worth while.

So why do it? It may have more to do with the Burger King itself and how it was acquired in 2010. According to the Financial Times, Burger King was purchased in a leveraged buyout, meaning that those doing the buying borrowed a great deal of money to do so. But interest expense is tax deductible. Since 2010, Burger King has been restructured and deleveraged, and since it went public in 2012 has had an 85% return in stock value. In other words, the people who own Burger King have done well. But buying Tim Hortons means that the consortium will once again have to borrow substantially to do the buying, creating further tax right-offs for the newly merged company.

There are other reasons for this merger that actually make sense. Burger King is struggling to gain market share and is under pressure from the growing business of “fast-casual” restaurants like Chipotle. But despite that it has a strong operating margin, 52%, which shows that the restructuring has been effective at making the business profitable. Meanwhile Tim Hortons has an operating margin of only 20%, an opportunity for improvement in the eyes of Burger King. Together they will form the third largest fast food business in the world and open a new front into the coveted and notoriously difficult breakfast market.

There may be other synergies and reasons for this merger and subsequent inversion, and the tax benefits that come from borrowing could do with some scrutiny, but it would seem from the outset that avoiding taxes is hardly the exclusive driving force behind this deal.