Pandemics, plagues and other disasters have previously heralded major changes to economic and social landscapes. Most notably, the Black Death had the effect of badly eroding the existing feudal structure. Literally so many people died that feudal lords had to entice serfs to come and work their land or risk it sitting fallow. The Irish potato famine, which reversed the demographic trends in Ireland and made it an outlier in European population growth, also drastically improved the lives of those that survived the famine. This pandemic will be no different, changing the fortunes of many by the time it is gone.

While I wait for books on our current situation, governments aren’t sitting idly by. Faced with an unprecedented crisis, politicians have cried havoc and let slip the public purse strings, passing huge relief bills and providing large social support to ease the monetary impact of global shutdowns and the sudden halt to economies.

This marks a serious departure from what might be considered “peace time” economic management. In normal times, and for much of the past 40 years, control of the economy has been left in the hands of central banks who have manipulated the overnight lending rates (or key interest rates) to encourage or retard economic growth. Even if you haven’t paid much attention to the work of central banks you are likely familiar with some of the most notable names. Alan Greenspan in the 1990s, Ben Bernanke through the financial crisis, and Mark Carney as the Governor of the Bank of Canada and then Governor of the Bank of England have all helmed a central bank and were a staple of economic news and forecasting.

The job of setting rates was to encourage growth and mange inflation; increasing the cost of borrowing should slow economic growth and curb inflation, while cutting rates should make borrowing cheaper and speed up economic growth. But since 2008, with rates hovering at near zero and now a global pandemic destroying wealth, governments have had to take a more active roll in direct economic management.

Enter Modern Monetary Theory, or MMT, the new(ish) idea that governments can largely spend their way out of problems and that fiscal deficits may be the cure for what ails us. The theory has been nicely (and optimistically) covered in the book “The Deficit Myth” by Stephanie Kelton, who argues that our understanding of money and taxes are wrong and as a result we have misunderstood the best way to deal with wealth inequality and job creation.

Kelton’s book is well written, but natural criticisms of her argument feel conspicuously absent. The crux of her thesis is that so long as you’re a “monetary sovereign”, that is a nation that issues its own currency and issues debt in its own currency, its impossible to go bankrupt. In addition, concerns that printing your own money might lead to inflation are not well grounded and that governments are not running deficits large enough to get to full employment. Some of this makes sense, indeed for many years we’ve seen countless countries like Canada, the United States and Japan all run very large deficits with no serious repercussions. But much of the language in the book feels unusually precise, navigating us around large objections with clever rhetorical sleight of hand. Where anyone with a passing understanding might wonder how it is that countries that have previously succumbed to too much debt and hyperinflation didn’t reap the benefits of MMT, the book is quick warn that you don’t want to have the “wrong” type of deficit and that too much spending can be detrimental, before rushing the reader off to see what can be done with MMT to fix pressing issues.

Whether this is a good idea or not, MMT has found a champion in Justin Trudeau, a prime minister for whom spending money as a political solution is as constant as the northern star. Reportedly our new finance minister Chrystia Freeland may be a fan too, a departure from the more traditional Bay Street pedigree of Bill Morneau. But even if our most senior politicians do not have any explicit endorsement of MMT, the direction of spending and the behavior of the Bank of Canada suggests the Modern Monetary Theory is central to current government policy.

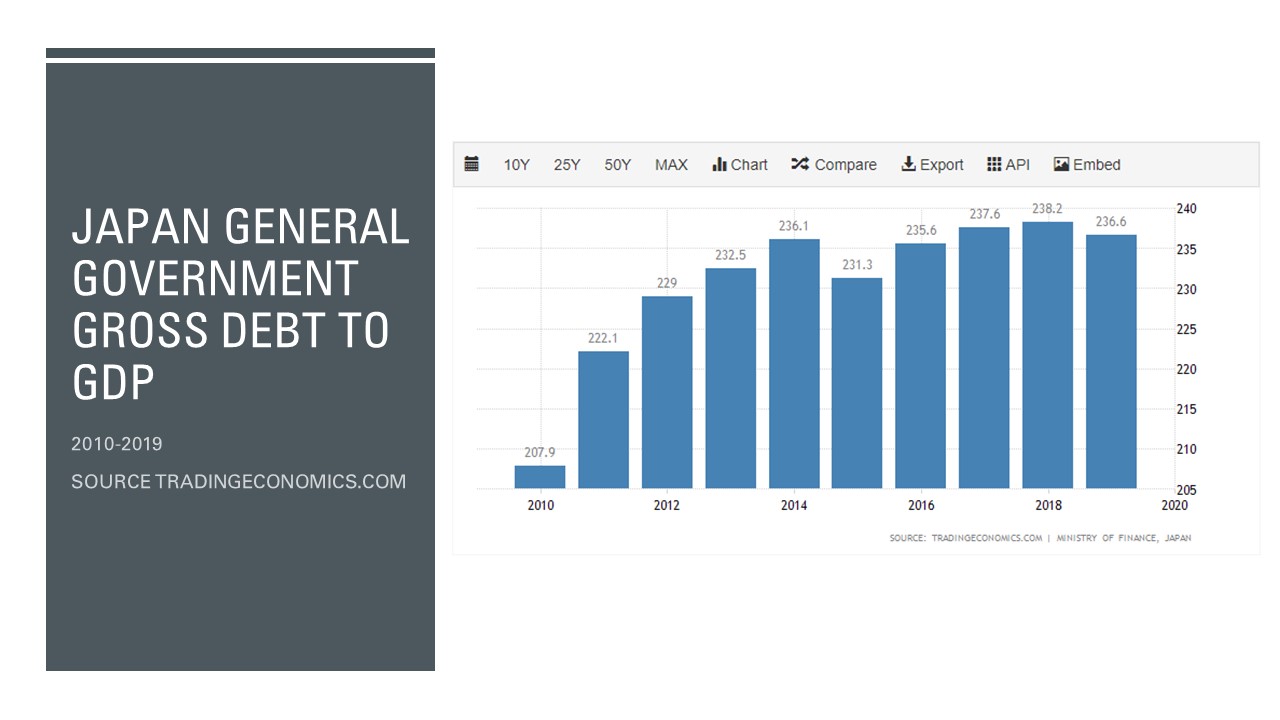

Since March, the Bank of Canada has purchased the vast bulk of Canadian government issuances, particularly at the long end of the yield curve (debt that matures in over 11 years), and by the end of 2021 the BoC is expected to hold 60% of all outstanding Government of Canada securities. Intentional or otherwise, this is what MMT looks like, with the government effectively issuing debt to itself so it can spend more. And currently Canada is on track to run the largest deficits of any country, developed or otherwise, in the world.

Governments frequently run deficits but have relied on efforts of slowed spending and economic growth to reduce the long-term debt burden. In fact, it has very rarely been the case that governments ever cut spending, more frequently simply reducing future promised spending below predicted rates of inflation. Yet despite the fact that no government I can think have has run a surplus over the last decade, the belief that we haven’t spent enough will likely only be a reassuring message to governments looking for opportunities to improve their standing in the polls.

Under MMT, politicians like Donald Trump actually look very good (this goes unacknowledged by Kelton, but its impossible to miss). Trump’s lavish spending and huge deficits did seem to have the desired impact of reducing unemployment to below 4%, much lower than the previously believed “natural” rate of unemployment of 5%. And as a result of the pandemic, the US deficit moved from an expected $1 Trillion in 2020, to about $3.7 Trillion for the year. It’s currently an open-ended question how much more needs to be spent before the deficit will be large enough to offset the impact of Covid-19, let alone all the other ills that society faces. Given that most economists are calling for even more spending into 2021 and maybe even 2022, its hard to imagine how big a cheque will need to be written.

A central tenet of our society has been that debt makes us weaker, and that unconstrained spending, either by a household or a government will inevitably become a problem if left unchecked. Modern Monetary theory turns this on its head, and while the theory is serious it would likely not have found mainstream consideration were it not for the pandemic. Like feudal lords forced to consider paying serfs to work their lands, politicians are having to make peace with running huge deficits and manage ballooning debts.

But MMT remains untested, its ideas about money, debt and financial sovereignty are theoretical. Our relationship to debt and our ideas about preserving wealth are very old and persistent, while those that have broken the bond of fiscal prudence, be it Greece in 2011, Zimbabwe in the 1990s, the Weimer Republic in post war Germany or Revolutionary France, have always ended in defaults and hyper-inflation.

I remain skeptical of ideas like MMT, but open to new approaches where old ones seem to be failing. Covid-19 will likely be with us until 2022, putting pressure on all levels of government for the immediate future. Politically, Western nations weren’t doing well prior to the pandemic, plagued with populist political insurgencies, a retreating liberal order and lack luster economic growth. Now with a mountain of new problems, MMT offers perhaps a path to saving economies and people’s livelihoods by freeing us from previous assumed constraints, but carries with it awesome risk. Will our political class be able to resist borrowing or printing too much? We may have no choice but to embark on this path, into an undiscovered country.

Information in this commentary is for informational purposes only and not meant to be personalized investment advice. The content has been prepared by Adrian Walker from sources believed to be accurate. The opinions expressed are of the author and do not necessarily represent those of Aligned Capital Partners Inc.