*A quick note – next week I will be discussing the recent market events, but had this written already last week and didn’t want it to go to waste.

** Performance numbers presented here all come from Questrade’s own website. They also represent the most recent numbers available.

Questrade is Canada’s fastest growing online advisory service that has built its business on the back of a catchy refrain: “Retire up to 30% richer”. There ads are everywhere and the simple and straightforward message has landed with a punch. The principle behind their slogan is that, over enough time, the amount of money you can save in fees by transferring to their online platform can be worth a substantial amount when that saved money is able to compound.

Competing on the price of financial advice has become common place, especially as people have become increasingly comfortable doing more online. Online “robo-advisors” dispense with all that pesky one-on-one business through your bank and have focused on providing the essentials of financial planning with a comfortable interface. Champions of lowering the costs of investing have hailed the arrival of companies like Questrade and Wealth Simple, believing that they would unsure in an era of low-cost financial advice.

Such a time has yet to materialize. For one thing, traditional providers of investments, like mutual fund companies, have learned to compete heavily in price, while an abundance of comparable low-cost investment solutions have given financial advisors a wider range of investments to choose from while being mindful of cost. Meanwhile, because internet companies have a business model called “scaling” which encourages corporations to rapidly expand on the backs of investors before they become profitable, its not clear whether robo-advisors are actually all that successful. Wealthsimple, one of the earliest and most prominent such services has broadened their business to include actual advisors meeting actual people, a decidedly more retrograde approach in the digital age.

Nevertheless, efforts to win over Canadians to these low cost model continue apace, and the market leader today is Questrade. So, what should investors make out of Questrade’s signature line? Can they really retire 30% richer?

Probably not.

First we should understand the mechanics of the claim. Looking through Questrade’s website we can see through their disclaimers that for each of their own portfolios they have taken the average five year returns for categories that align with each portfolio, the average fees for those categories and added back the difference in the costs. So, for their Balanced Portfolio they refer to the “Global Neutral Balanced Category” and the five-year number associated with that group of funds (the numbers seem to be drawn from Morningstar, the independent research firm that tracks stocks, mutual funds and ETFs).

Figure 1 https://www.questrade.com/disclosure/legal-notice-and-disclosures/2018/08/08/questwealth-portfolios-calculator

Thus, they arrive at an assumed ROR of 6.21% for five years, and then project that number into the future for the next 30 years. They also calculate the fee of 2.22% (the average for the category) and subtract that from the returns. And using those assumptions Questrade isn’t wrong. Assuming you received the average return and saved the difference in fees, over 30 years you’d be 30% richer.

Except you probably wouldn’t.

Questrade actually already has a five year performance history on their existing investments, and we can go and check to see how well they’ve actually done. Unfortunately for Questrade, their actual performance in practice is not considerably better than the average return against the categories they are comparing. For the last five years, Questrade’s 5 year annualized performance is 4.92%, less than 0.3% better than the category average of 4.66%.

But wait, there’s more!

Keep in mind that Questrade’s secret sauce is not the intention to outperform markets, merely to get the average return and make up the difference in fees, but when put into practice it isn’t even 1%, let alone 2% ahead of their average competitors. In fact, we could go so far as to say the Questrade is a worse than average performer since if we assumed the same fees were to apply, Questrade’s performance would be significantly below the average return. In fact, for the purposes of their own history the above performance is shown GROSS of fees. Yes, if you read the fine print you discover that Questrade has not deducted its own management costs from these returns, meaning that the real rate of return would be 4.54%, officially below the average they are trying to beat!

Figure 3 https://www.questrade.com/questwealth-portfolios/etf-portfolios#balanced

Figure 4 This has been taken from Morningstar and compares the B Series Fidelity Global Balanced Portfolio performance against its category, Global Neutral Balanced. Performance for the individual fund is better than the 5 year average of Questrade’s comparable investment, and ahead of the five year average for the category of 4.66%. This should not be construed as an endorsement of Fidelity or any investment they have.

There is a temptation towards smugness and finger wagging, but I think its more important to ask the question “Why is this the case?” The argument for passive index ETFs has been made repeatedly, and its argument makes intuitive sense. Getting the market returns at a low price has shown to beat active management over some time periods. So why would Questrade underperform, particularly when markets have been relatively stable and trending up? I have my theories, but it should really be incumbent on Questrade to explain itself. What does stand out about this situation is that if you are unhappy with your performance THERE IS NOTHING YOU CAN DO ABOUT IT! Questrade’s portfolios represent their best mix, and do not allow you to make substitutions or even really get an explanation for the under-performance. The trade off in low cost alternatives is all the personalization, flexibility and face to face conversations that underpin the traditional advisor client relationship.

Given all the regulations that surround investing, I remain surprised that Questrade is able to advertise a hypothetical return completely detached from their actual returns, but that is yet another question that should be settled by people who are not me. Questrade has some benefits, not least is their low fees, but investors should be honest with themselves about how beneficial low fees are in a world when there are many options and the cost of navigating those options represents their best chance at retiring happy and secure.

As always, if you have questions, need some guidance or just a second opinion, please contact me directly at adrian@walkerwealthmgmt.com

Information in this commentary is for informational purposes only and not meant to be personalized investment advice. The content has been prepared by Adrian Walker from sources believed to be accurate. The opinions expressed are of the author and do not necessarily represent those of ACPI.

One explanation for this is that the labor participation rate has been very low and that the unemployment rate, which only captures workers still looking for work and not those that have dropped out of the workforce altogether, didn’t tell the whole story about people returning to the workforce. The result has been that there has been an abundance of potential workers and as a result there really hasn’t been the labor shortage traditionally needed to begin pushing up inflation.

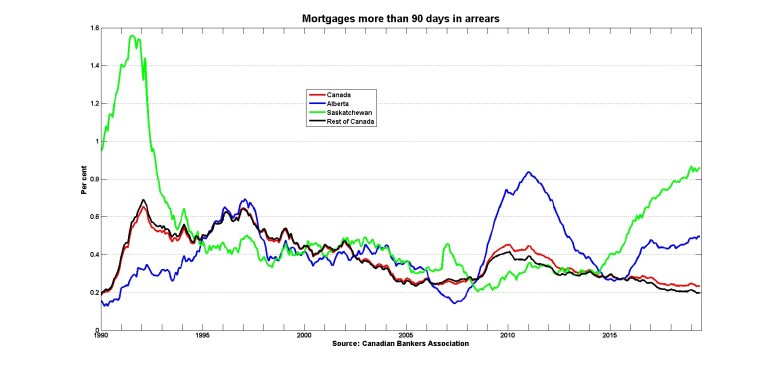

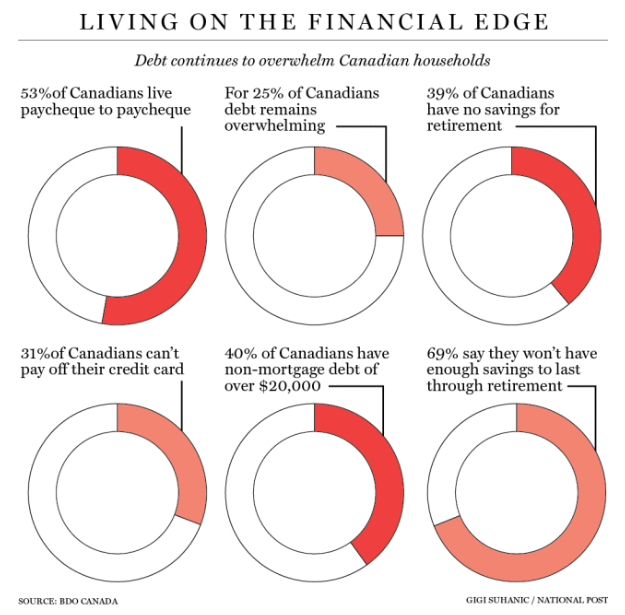

One explanation for this is that the labor participation rate has been very low and that the unemployment rate, which only captures workers still looking for work and not those that have dropped out of the workforce altogether, didn’t tell the whole story about people returning to the workforce. The result has been that there has been an abundance of potential workers and as a result there really hasn’t been the labor shortage traditionally needed to begin pushing up inflation. The short version of this story is that Canadians are heavily in debt and much of that debt is sensitive to interest rates. Following a few rate hikes, insolvencies

The short version of this story is that Canadians are heavily in debt and much of that debt is sensitive to interest rates. Following a few rate hikes, insolvencies  Walking hand in hand is the increasing cost of education, and the declining returns it provides. In the United States the fastest growth in debt, and the highest rate of default is now found in student debt. According to Reuters the amount of

Walking hand in hand is the increasing cost of education, and the declining returns it provides. In the United States the fastest growth in debt, and the highest rate of default is now found in student debt. According to Reuters the amount of

Efforts to hold off an actual recession though may have moved beyond the realm of political expediency. Globally there has been a slowdown, especially among economies that export and manufacture. But perhaps the most worrying trend is in the sector that’s done the best, which is the stock market. Compared to all the other metrics we might wish to be mindful of, there is something visceral about a chart that shows the difference in price compared to forward earnings expectations. If your forward EPS (Earnings Per Share) is expectated to moderate, or not grow very quickly, you would expect that the price of the stock should reflect that, and yet over the past few years the price of stocks has become detached from the likely earnings of the companies they reflect. Metrics can be misleading and its dangerous to read too much into a single analytical chart. However, fundamentally risk exists as the prices that people are willing to pay for a stock begin to significantly deviate from the profitability of the company.

Efforts to hold off an actual recession though may have moved beyond the realm of political expediency. Globally there has been a slowdown, especially among economies that export and manufacture. But perhaps the most worrying trend is in the sector that’s done the best, which is the stock market. Compared to all the other metrics we might wish to be mindful of, there is something visceral about a chart that shows the difference in price compared to forward earnings expectations. If your forward EPS (Earnings Per Share) is expectated to moderate, or not grow very quickly, you would expect that the price of the stock should reflect that, and yet over the past few years the price of stocks has become detached from the likely earnings of the companies they reflect. Metrics can be misleading and its dangerous to read too much into a single analytical chart. However, fundamentally risk exists as the prices that people are willing to pay for a stock begin to significantly deviate from the profitability of the company.

Australia, which has had years of heat waves, has recently faced some of the worst forest and brush fires imaginable (and currently bracing for more).

Australia, which has had years of heat waves, has recently faced some of the worst forest and brush fires imaginable (and currently bracing for more).

His party was a grab bag of disaffected curmudgeons and, unsettlingly, a number of quasi-racists who were obsessed with immigration.

His party was a grab bag of disaffected curmudgeons and, unsettlingly, a number of quasi-racists who were obsessed with immigration.

In their book “Revolt on the Right: Explaining Support For The Radical Right in Britain” by Matthew Goodwin and Robert Ford, the authors note that the rise of populist UKIP party is “not primarily the result of things the mainstream parties, or their leaders, have said or done…instead, is the result of their inability to articulate, and respond to, deep-seated and long-standing social and political conflicts”.

In their book “Revolt on the Right: Explaining Support For The Radical Right in Britain” by Matthew Goodwin and Robert Ford, the authors note that the rise of populist UKIP party is “not primarily the result of things the mainstream parties, or their leaders, have said or done…instead, is the result of their inability to articulate, and respond to, deep-seated and long-standing social and political conflicts”.

Many populists already exist in our politics. Issues around education, housing and debt remain hot buttons for the electorate. And yet our last election spent far more time focused on a speech by Andrew Scheer from over a decade ago. Does that seem like a political class articulating and responding to long standing and deep seated issues, or one that has learned to master the art of getting elected? Education costs continue to climb and yet the return to students is considerably lower, and prospects much worse for those with only high school diplomas. Debt in Canada has continued to rise, a story that seems evergreen, but insolvencies have also started climbing. Currently insolvencies remain low overall, but given the large amount of Canadian debt, what might it take to push people over the edge? Which politician can honestly say they’ve got a good plan to deal with these problems?

Many populists already exist in our politics. Issues around education, housing and debt remain hot buttons for the electorate. And yet our last election spent far more time focused on a speech by Andrew Scheer from over a decade ago. Does that seem like a political class articulating and responding to long standing and deep seated issues, or one that has learned to master the art of getting elected? Education costs continue to climb and yet the return to students is considerably lower, and prospects much worse for those with only high school diplomas. Debt in Canada has continued to rise, a story that seems evergreen, but insolvencies have also started climbing. Currently insolvencies remain low overall, but given the large amount of Canadian debt, what might it take to push people over the edge? Which politician can honestly say they’ve got a good plan to deal with these problems?

The temptation to assume that everything is about to go wrong is therefore not the most far-fetched possibility. Investors should be cautious because there are indeed warning signs that the economy is softening and after ten years of bull market returns, corrections and recessions are inevitable.

The temptation to assume that everything is about to go wrong is therefore not the most far-fetched possibility. Investors should be cautious because there are indeed warning signs that the economy is softening and after ten years of bull market returns, corrections and recessions are inevitable.