While protests may not be, strictly speaking, market-based news, the size and scope of the protests regarding police violence and black lives makes them hard to ignore regardless of context. So far, these massive public demonstrations have not had an impact on markets (though they may yet on the spread of Covid-19), and have garnered a mixed reaction in the wider society. Whether police will be held to a level of greater accountability for actions that result in death remains to be seen, and regardless of what reforming actions are taken by police departments its quite obvious that it will take years to overcome distrust of authorities in some communities.

A more interesting aspect of the protests have been calls to “defund the police”, a rallying cry that either means exactly what it says, or sparks 15 minutes of explanations as it “doesn’t mean quite what it sounds like”. The arguments for it do make some sense though, and within some police departments there is sympathy for the idea that too much is asked of the police, resulting in a hodgepodge of policy goals foisted on a group simply not equipped to handle them. Currently the same people who have to deal with a domestic disturbance and oppose criminal gangs are the same people that have to help those with serious mental health issues and spend their days collecting revenue for cities. Not all these jobs should likely fall on the same person.

This raises an interesting point, which is how our political class has largely sidestepped any of the blame aimed at police departments. Police only enforce the laws that they have on the books, and true to any bureaucratic industry, we have lots of laws on the books. So many laws in fact that it is practically impossible to know what they all are. By-laws are added with little consideration for what has preceded it, speed limits seem set arbitrarily and may be subject to change, some laws are posted while others invisible. Which laws are enforced and where is left to the discretion of the police at the time. Many laws end up serving an unintended dual function, launched ostensibly to combat thing A, but end up serving issue B.

Consider that in 2008, Ontario passed a law making it illegal to smoke in a car in the presence of a minor, someone under the age of 16. This was part of a long campaign aimed at discouraging smoking in public that bore some superficial resemblance to other laws that discouraged smoking by making it harder to do in social settings. But where as smoking in public on patios and bars limited where you could go, this new law invited police into a citizen’s private space and criminalized behavior that was, at least under the laws of the province, still kind of legal. But the real issue here is who the law inadvertently targets.

Despite continued drops in the number of people smoking, those people that do smoke are statistically more likely to be poorer with more minimal education. According to the CDC 30% of people below and 25% of those at or just above the poverty line smoke, while those at more than double the poverty level only smoke at a rate of about 15%. In short the people most likely smoking in their car won’t be found in Leaside, but might be found in one of Toronto’s less affluent but already heavily policed neighborhoods. This law isn’t intended to target minorities or the poor, but put in the hands of police who are already tasked with policing higher crime areas (again areas that tend towards being poorer and with higher populations of minorities and new Canadians) it puts another class of previously non-offending people into potential confrontations with the police.

You may remember the death of Eric Garner in 2014. Another black American who died in the arms of a police officer that was caught on camera, Garner had been placed in a choke hold and had died from lack of asphyxiation. Garner’s crime, that had led him to this confrontation with multiple police, was for selling “loose cigarettes”. As part of a style of policing called “broken windows”, police had been instructed by the highest levels of authority within civilian politics to crack down on minor crimes to scare off larger criminal enterprises. Tackling the “loose cigarette” problem ultimately involved “the deployment of special plainclothes unit, two sergeants, and uniformed backup” to arrest a man selling cigarettes for a dollar who had been arrested 12 previous times. At no point did anyone wonder if this was a useful deployment of resources, or whether re-arresting a man who had already been arrest 12 times might finally break his habit.

You might be tempted to imagine that police would simply look the other way when silly or impractical laws find their way onto the books, but this too is a problem. Indeed, we know that the police can sometimes be given directives to enforce some laws over others. But the law cannot function effectively when it is applied only at the discretion by those in authority. If a law cannot be practically enforced or only enforced unevenly, it probably shouldn’t be a law at all.

Politicians remain responsive to their voters, particularly so at municipal levels. That can put enormous pressure on them to pass laws that are intended to fix social ills for moral reasons, but our politicians should be mindful that every law passed puts potentially puts citizens into conflict with the police. So long as the police remain the first line of citizen’s interaction with the state’s power, whether it be for jay walking, speeding, parking illegally, domestic disturbances, assault, or more serious illegal activity, any action can theoretically become fatal. Recently two young people died during police interventions in the GTA. The first was a young woman named Regis Korchinski-Paquet, who fell from a balcony during a mental health crisis when police showed up to take her to CAMH. The second, D’Andre Campbell was shot by police in his home in Brampton when police were called because he was having a schizophrenic episode. How culpable the police were in these events is the subject of much debate, but families in both instances have wondered aloud whether it is the police that should be the people who come during a mental health crisis.

While Canada’s problems are mercifully not those of the United States (the proliferation of guns and the militarization of police are fortunately not major issues here), that shouldn’t excuse politicians who make noise about police excesses while being quick to use the law to fix minor grievances. While the police continue to do their own reviews and consider reforms, politicians should perhaps begin considering an audit of the numerous laws that we keep and whether it still makes sense to be ticketing people for jaywalking, working out in a park, or issuing fines to children who run a lemonade stand, especially when these laws can not be enforced with any consistency. Whether our politicians can rise to meet even this challenge remains to be seen.

*In addition to the linked articles within this post, I have also referenced the book The End of Policing by Alex S. Vitale for anyone interested in the arguments of defunding or abolishing the police.

Information in this commentary is for informational purposes only and not meant to be personalized investment advice. The content has been prepared by Adrian Walker from sources believed to be accurate. The opinions expressed are of the author and do not necessarily represent those of Aligned Capital Partners Inc.

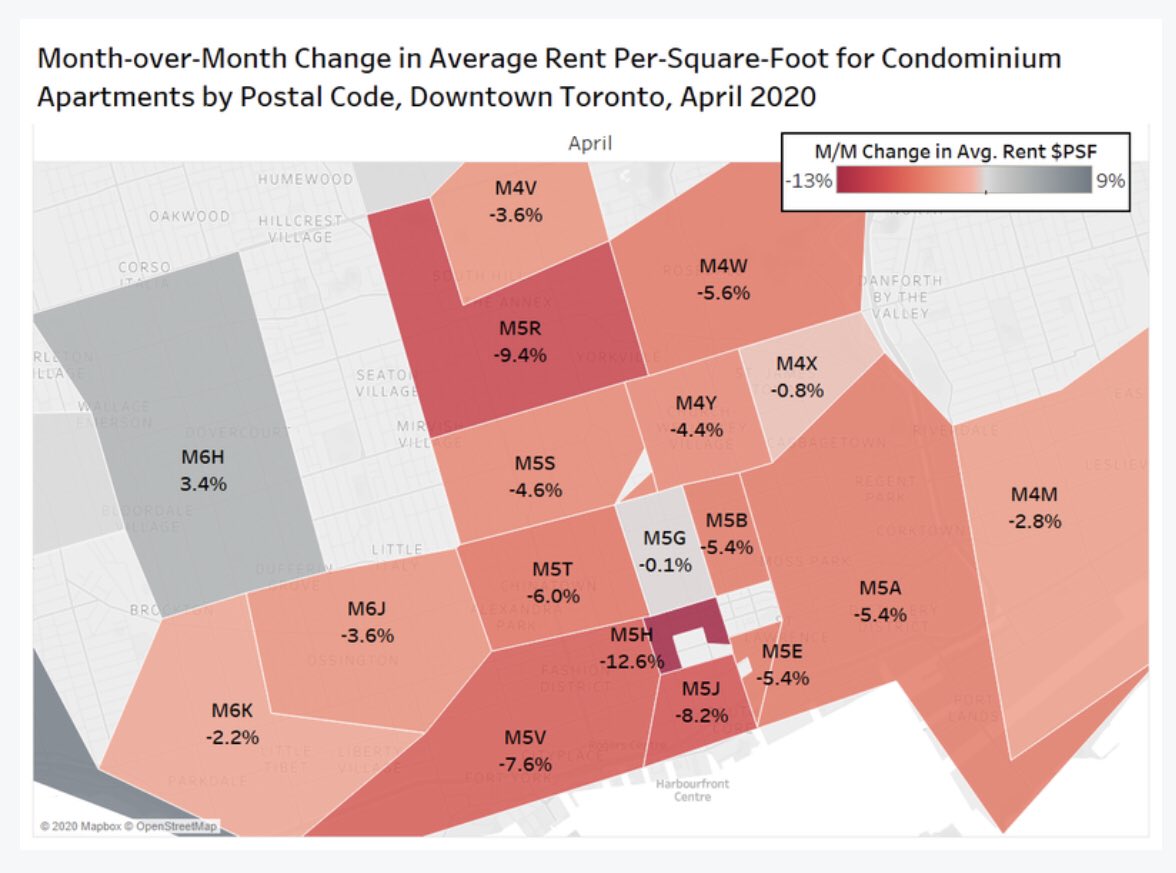

Real estate remains at the heart of the Canadian economic story for the last 20 years. Appreciating housing prices are the chief source for growth in Canadian families’ net worth. Borrowing to buy houses and borrowing against home equity remain our chief sources of debt. Our politics revolves around the tension of needing more housing in certain highly desirable areas while preserving those areas from over development. That dynamic has revolved around a status quo that seemed to have no conceivable end. The pandemic may have radically altered the Canadian real estate landscape regardless of how people feel about it or what they want. Whether we can walk back changes of this magnitude remains very much unknowable. For now we can only watch the changes our society and economy are undergoing and hope that what we are witnessing will be for the best, those changes that have happened, and those yet to come.

Real estate remains at the heart of the Canadian economic story for the last 20 years. Appreciating housing prices are the chief source for growth in Canadian families’ net worth. Borrowing to buy houses and borrowing against home equity remain our chief sources of debt. Our politics revolves around the tension of needing more housing in certain highly desirable areas while preserving those areas from over development. That dynamic has revolved around a status quo that seemed to have no conceivable end. The pandemic may have radically altered the Canadian real estate landscape regardless of how people feel about it or what they want. Whether we can walk back changes of this magnitude remains very much unknowable. For now we can only watch the changes our society and economy are undergoing and hope that what we are witnessing will be for the best, those changes that have happened, and those yet to come.

But what of the predictions we keep hearing about? That life will be forever changed by the events we’re living through? While I have a great deal more to say about the nature of prognostication, I’ll keep my comments here brief. In general history shows that humans don’t tend towards radical changes following big, but temporary upheavals. Instead, crises like the one we are living through emphasize existing weaknesses within the society.

But what of the predictions we keep hearing about? That life will be forever changed by the events we’re living through? While I have a great deal more to say about the nature of prognostication, I’ll keep my comments here brief. In general history shows that humans don’t tend towards radical changes following big, but temporary upheavals. Instead, crises like the one we are living through emphasize existing weaknesses within the society.