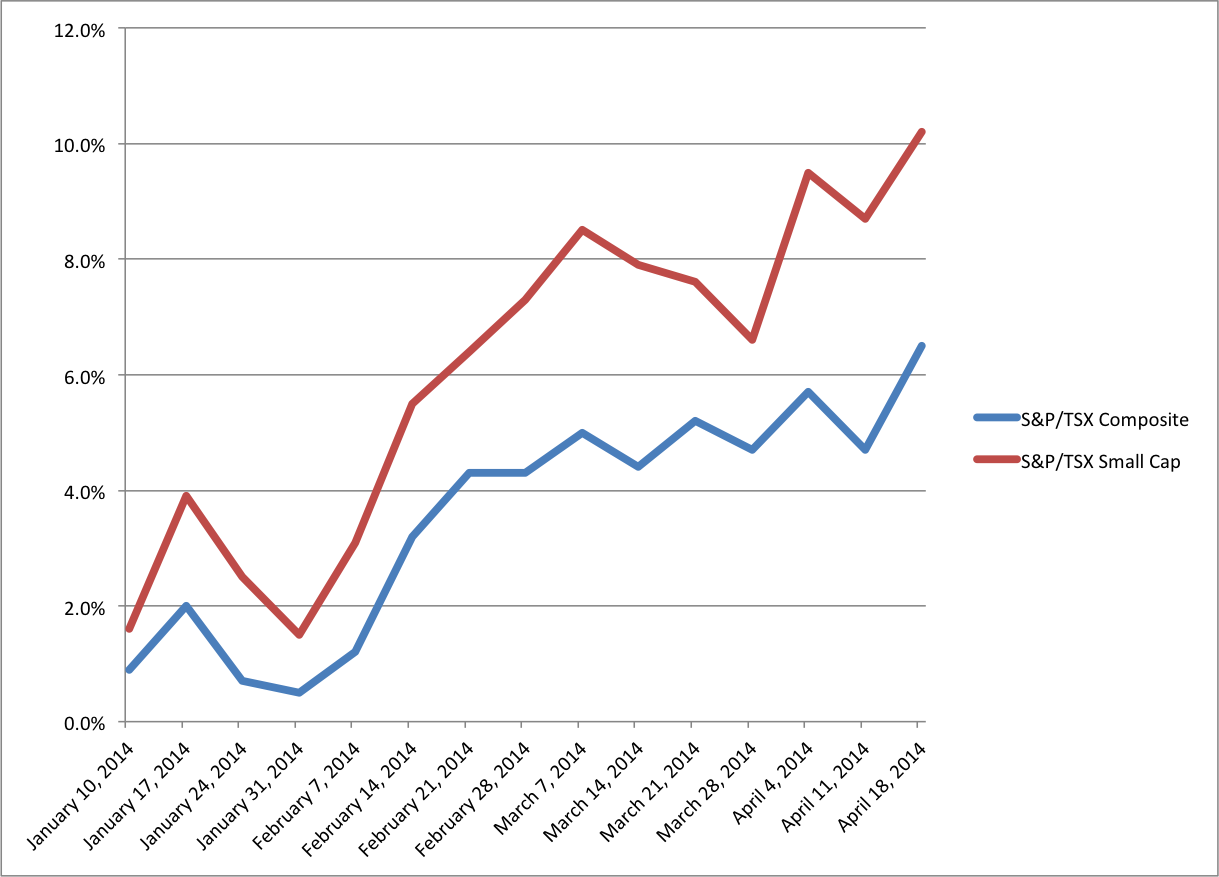

This year the Canadian markets have been doing exceptionally well. Where as last year the S&P/TSX had been struggling to get above 2% at this time, this year the markets have soared ahead of most of their global counterparts. In fact the Canadian market triumph is only half of this story, matched equally by the disappointing performance of almost every significant global market. Concerns over China have hurt Emerging Markets. The Ukrainian crisis has hindered Europe, and a difficult winter combined with weaker economic data has put the brakes on the US as well.

This year the Canadian markets have been doing exceptionally well. Where as last year the S&P/TSX had been struggling to get above 2% at this time, this year the markets have soared ahead of most of their global counterparts. In fact the Canadian market triumph is only half of this story, matched equally by the disappointing performance of almost every significant global market. Concerns over China have hurt Emerging Markets. The Ukrainian crisis has hindered Europe, and a difficult winter combined with weaker economic data has put the brakes on the US as well.

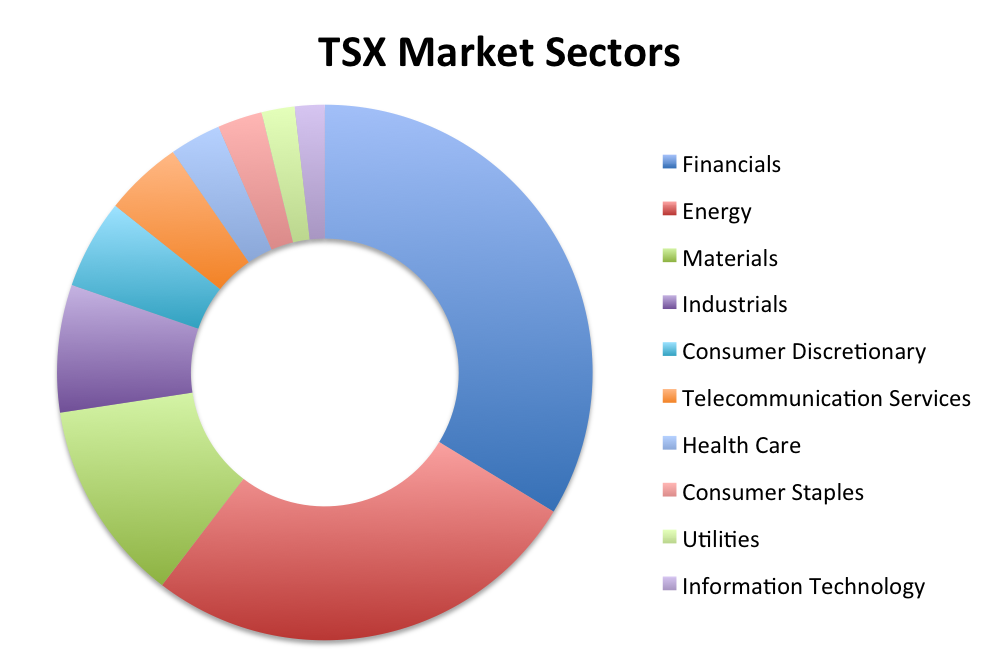

But this sudden return to form should not fool Canadians. It is a common trope of investing that people over estimate the value of their local economies, and a home bias can prove to be dangerous to a portfolio. Taking a peak under the hood of Canada’s market performance and we see it is largely from the volatile sectors of the economy. In the current year the costs of Oil, Natural Gas and Gold are all up. Utilities have also driven some of the returns, but with the Materials and Energy sector being a full third of the TSX its easy to see what’s really driving market performance. Combined with a declining dollar and improving global economy and Canada looks like an ideal place to invest.

But the underlying truth of the Canadian market is that it remains unhealthy. Manufacturing is down, although recovering slowly. Jobs growth exists, but its highly anemic. The core dangers to the vast number of Canadians continue to be high debt, expensive real-estate and cheap credit. In short, Canada is beginning to look more like pre-2008 United States rather than the picture of financial health we continue to project. Cheap borrowing rates are keeping the economy afloat, and it isn’t at all clear what the government can do to slow it down without upsetting the apple cart.

For Canadian investors the pull will be to increase exposure to the Canadian market, but they should be wary that even when news reports seem favourable about how well the Canadian economy might do, they are not making a comment about how healthy the economy really is. Instead they are making a prediction about what might happen if trends continue in a certain direction. There are many threats to Canada, both global and domestic, and it should weigh heavily on the minds of investors when they choose where to invest.