To say that Canadians aren’t financially literate may seem a touch unfair, but everywhere you look we find testaments to this unavoidable fact. Credit cards, car loans, mortgage rates and even how returns are calculated are a confusing mess for most people. The math that governs these relationships is often opaque and can feel misleading, and its complexity assures that even if some do understand it, the details will only be retained by a tiny minority.

To say that Canadians aren’t financially literate may seem a touch unfair, but everywhere you look we find testaments to this unavoidable fact. Credit cards, car loans, mortgage rates and even how returns are calculated are a confusing mess for most people. The math that governs these relationships is often opaque and can feel misleading, and its complexity assures that even if some do understand it, the details will only be retained by a tiny minority.

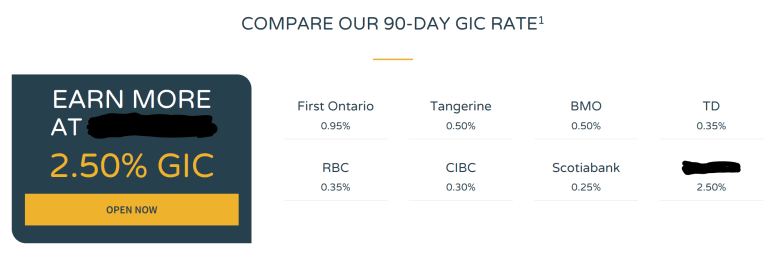

Even relatively straightforward investments can be terrifically misleading. Take for instance a well-known credit union offering a (limited) 90-day rate of 2.5% on a GIC. This advertised rate is not simply featured in the windows of its various locations but is promoted online and on the radio.

Banks and credit unions frequently offer improved GIC rates for a limited time to drive deposits. But how those rates are advertised can be misleading. The aforementioned “2.5% 90 Day GIC rate” has its own website where it contrasts its deposit rate against other major financial institutions, all of them paltry compared to the prominently displayed 2.5%.

At the very bottom of the website there does exist a footnote however. That 90-day GIC rate? It’s an annualized number, meaning that the interest you will earn at the end of that 90 days is 0.62% not 2.5%. The most egregious part perhaps is that it compares its misleading return to the far more understandable 90 day return of other GIC providers.

Other innovations in obfuscation abound. Exploring their website and we find a “linked GIC” which offers to protect your principle while giving you market returns linked to a custom index. The marketing material promises to “give you exposure to the Canadian stock market” and offers you a chance to see it performance results. But if you click to learn more of the details you find out that returns on the 3 year product are capped with cumulative returns of 15%. Not bad until you remember that traditionally returns are annualized in Canada. The maximum returns the product will offer is 4.77% regardless of what the market does in that time. Better than a 3 year GIC perhaps, but potentially far worse than what the market may deliver.

As always, the details are available for those interested. They’re just a scroll farther down, an additional click, or perhaps another page over. So, if there exists full disclosure, what am I complaining about?

The answer is best illustrated in every search you do on Google. At the top of the page are the websites that have sought to be promoted. 67% of clicks are on the top five results on a google search. 95% of clicks are exclusively for the first page only. Things on the next page barely warrant looking at. It’s just not of interest. Disclosure details may only be a click away, but from the point of view of an average person looking over the details, they may never get around to reading them.

GICs are considered the safest investments for Canadians looking for security, but their function is to provide banks with low cost loans to help finance their own business activities. Every investment made in a GIC may help bring someone comfort at night, but they’ve really entered a business relationship with a bank. Framed as such it seems that better and clearer disclosure should be the primary order, but because our thinking is that GICs are a form of product they are treated as such.

Importantly, I must stress that these banks, credit unions, and other financial institutions are not lying. They are doing what they are allowed to do under the various laws that govern financial institutions. That such rules fall short is precisely why its always smart to talk to an independent financial advisor like myself. Providing context, clarity and advice free from the conflict of corporate proprietary products is how we help people every day, and its what makes us unique.

If you have questions about this article, or wish to discuss an important financial matter please call or email us!