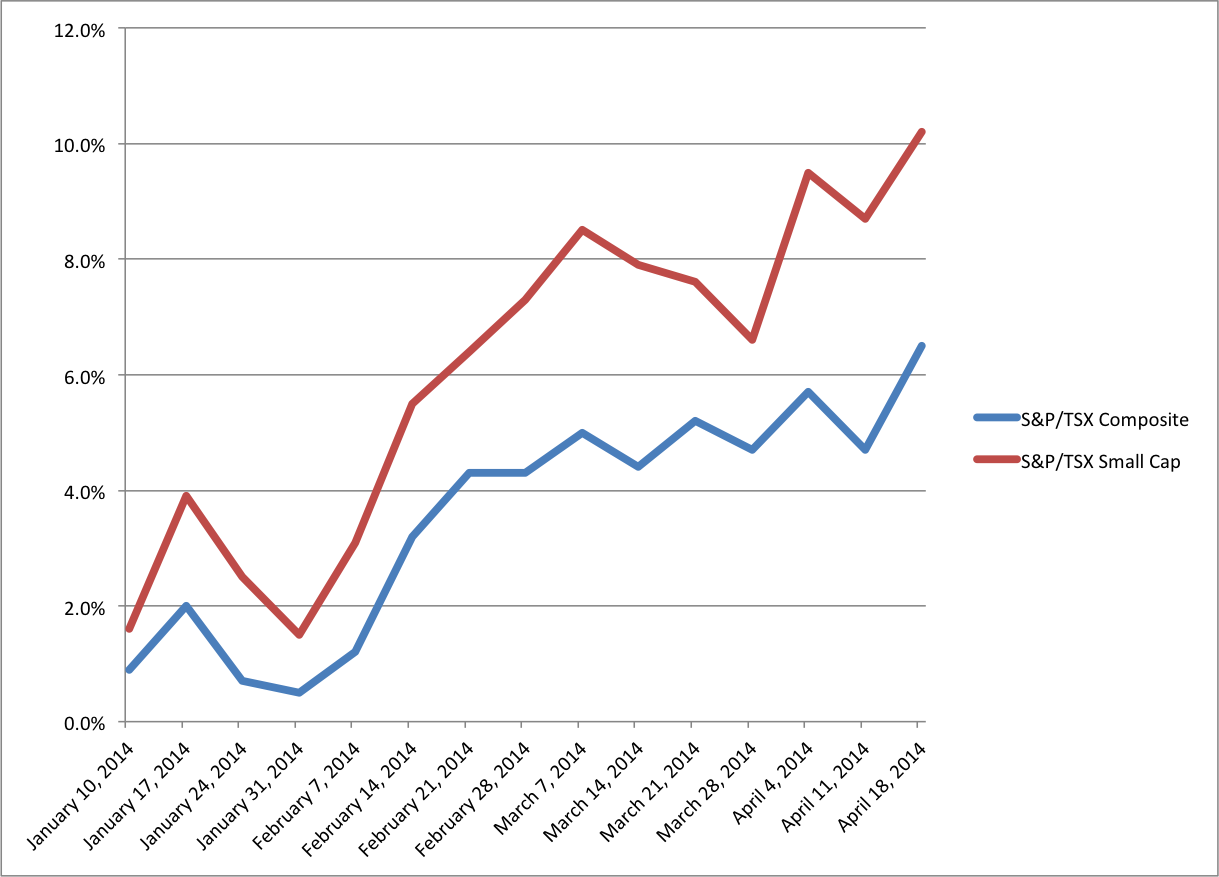

I am regularly quite vocal about my concern over the Canadian economy. But like anyone who may be too early in their predictions, the universe continues to thwart my best efforts to make my point. If you’ve been paying attention to the market at all this year it is Canada that has been pulling ahead. The United States, and many global indices have been underwater or simply lagging compared to the apparent strength of our market.

I am regularly quite vocal about my concern over the Canadian economy. But like anyone who may be too early in their predictions, the universe continues to thwart my best efforts to make my point. If you’ve been paying attention to the market at all this year it is Canada that has been pulling ahead. The United States, and many global indices have been underwater or simply lagging compared to the apparent strength of our market.

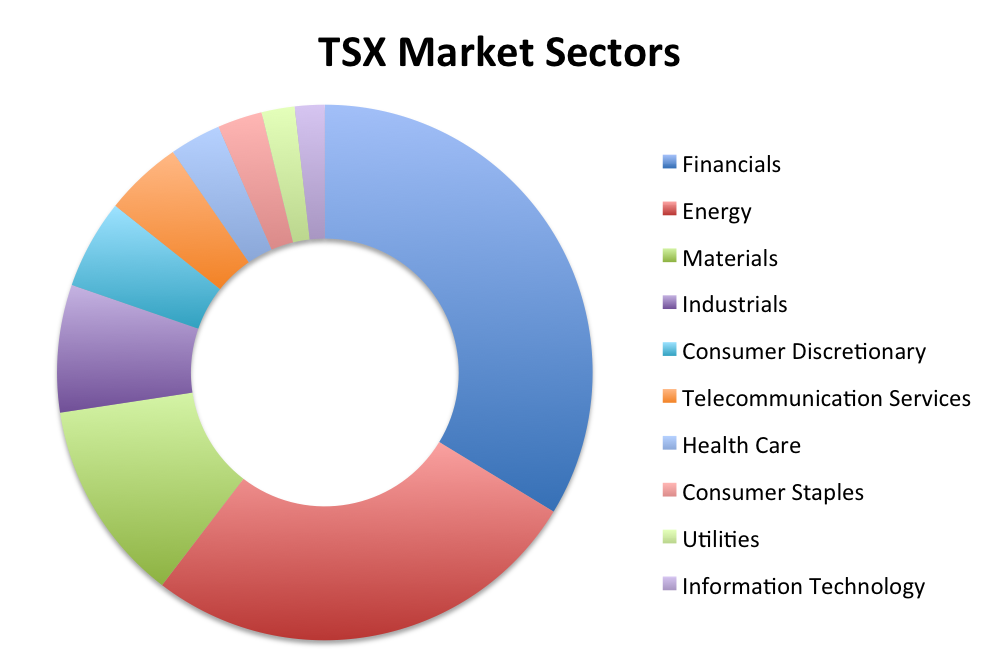

But fundamentals matter. For instance, the current driver in the Canadian market is materials and energy (translation, oil). But it’s unclear why this is, or more specifically, why the price of oil is so high. With the growing supply of oil from the US, costly Canadian oil seems to be the last thing anyone needs, but a high oil price and a weak Canadian dollar have conspired to give life to Canadian energy company stocks.

Similarly the Canadian job market has been quite weak. Many Canadian corporations have failed to hire, instead sitting on mountains of cash resulting in inaction in the jobs market. Meanwhile the weak dollar, typically a jump start to our industrial sector, has failed to do any such thing. But at the core of our woes is the disturbing trend of burdensome debt and the high cost of homeownership.

I know what you want to say. “Adrian, you are always complaining about burdensome debt and high costs of homeownership! Tell me something I don’t know!” Well, I imagine you don’t know just how burdensome that debt is. According to Maclean’s Magazine the total Canadian consumer and mortgage debt is now close to $1.7 Trillion, 1 trillion more than it was in 2003. That’s right, in a decade we have added a trillion dollars of new debt. And while there is some evidence that the net worth of Canadian families has gone up, once adjusted for inflation that increase is really the result of growing house prices and recovering pensions.

Today Canadians carry more personal credit card debt than ever before. We spend more money on luxury goods, travel and on home renovations than ever before. Our consumer spending is now 56% of GDP, and it is almost all being driven by debt.

Canadians have made a big deal about how well we faired through the economic meltdown of 2008, and were quick to wag our fingers at the free spending ways of our neighbours to the South, but the reality is we are every bit as cavalier about our financial well being as they were at the height of the economic malfeasance. While it is unlikely we will see a crash like that in the US, the Canadian market is highly interconnected, and drops in the price of oil will have a ripple effect on borrowing rates, defaults, bank profits and unemployment, all of which is be exasperated by our high debt levels.

On more than one occasion I have been quizzed about the future of some stock market-or-other to the lack of satisfaction of the quizzer. Invariably the conversation goes something like: “What with all the money being printed and the new highs of the stock market, shouldn’t it all come down?” And my answer is usually, “No.”

On more than one occasion I have been quizzed about the future of some stock market-or-other to the lack of satisfaction of the quizzer. Invariably the conversation goes something like: “What with all the money being printed and the new highs of the stock market, shouldn’t it all come down?” And my answer is usually, “No.”