As a rule I dislike large majority governments. Far from believing that minority or coalition governments are unworkable, we have a good history of weak governments focusing on practical solutions that usually avoid the trappings of their respective ideological ends. Because the thing that worries me most about governments is not the promises they won’t keep, but the promises they will.

As a rule I dislike large majority governments. Far from believing that minority or coalition governments are unworkable, we have a good history of weak governments focusing on practical solutions that usually avoid the trappings of their respective ideological ends. Because the thing that worries me most about governments is not the promises they won’t keep, but the promises they will.

The resounding victory for the Liberal Party and Justin Trudeau means that the big worry for Canadians should be exactly this. Trudeau has promised rollback TFSA contributions, decreases in the planned rise of OAS, and add a new tax on people earning more than $200,000. Tax hikes haven’t been a popular part of political platforms over the past few decades, yet Trudeau’s platform was successful for precisely that, tackling perceived inequalities benefiting “millionaires” and a promised difference in governing style from the more insular and autocratic Harper.

While I may personally quibble over defining (and vilifying) “millionaires” as people earning more than $200,000, we must acknowledge that an upper tax rate of 33% on income over $200,000 isn’t so cumbersome that we should start panicking and freaking out. That is until you add in the provincial taxes.

Assuming that everything goes to plan, the top tax bracket in Ontario will be 54% sometime next year. That won’t even make Ontario unique. More than half of the provinces will have a top tax bracket in excess of 50%, with the highest being New Brunswick, clocking in at an impressive 59%. And what of the tax cut for earnings between $45,000 to $90,000? While it is estimated to put around $670 back into your pocket, it’s relief may be short lived in Ontario.

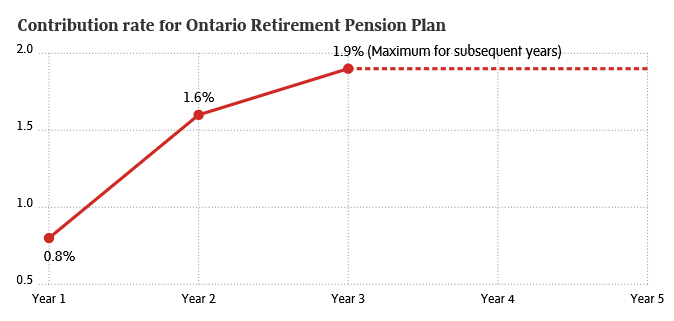

Hot on the heels of that cut will be the new ORPP, or Ontario Retirement Pension Plan, which will take about 1.9% of your salary by 2017, easily eating up whatever tax savings you were just given and then some.

It’s easy to lose perspective on taxes and become an annoyance at family dinners, complaining about your money being stolen by evil government officials. But that shouldn’t mean that we aren’t vigilante about how much we pay in taxes either. On the docket across the country tax hikes are poised in every corner. In Alberta the NDP has raised taxes on corporations, even as the economy weakens. In Ontario the Liberals have decided to allow each municipality to set their own land transfer tax, representing a likely hike for many cities. And of course federally, the ending of income splitting, the rolling back of TFSA contribution room and the aforementioned new tax bracket all represent new costs for citizens.

I have an open dislike of Trudeau’s use of the term “millionaires” and “the wealthy” to talk about people earning $200k, it seems like a semantic trick. Few of us, after all, can muster the courage to defend an income that many will never see. But as unsympathetic as we may be to the “1%”, we should be mindful that taxes go up to cover costs, and if the economy slows or debt balloons, we may find that the “millionaires” encompasses an increasing number of us.