On Tuesday the Conservative government effectively outlined their election campaign in their federal budget, and the most contentious issue (so far) has been the expansion of the annual TFSA contribution room from $5500 to $10,000. The TFSA is still a small part of the makeup of most Canadians savings, and yet the proposal of this program has already prompted Justin Trudeau to denounce it and promise to roll back the reform.

The growth of TFSAs definitely will hit tax revenues for the government. This year alone it is estimated to reduce revenue by $85 million, and in a few years that number will be over $350 million. By 2035 estimates put it will be close to $650 million in lost tax revenue. However we should be wary about attaching too much importance to long term estimates. Economic growth, population trends, even the price of oil will play a larger role in government revenues than the TFSA. We can barely get a fix on the price of oil over the next six months, so there is little use in getting worked-up over decade scaled predictions.

This leaves the other chief complaint about the TFSAs, that they only benefit the wealthy. There is some truth to this. The wealthiest Canadians are certainly in a better place to capitalize on multiple different forms of tax sheltering. But that is always the case. The wealthiest among us are able to capitalize on all things more effectively, from designer purses to sports cars. The question for average Canadians is can we also benefit from TFSAs?

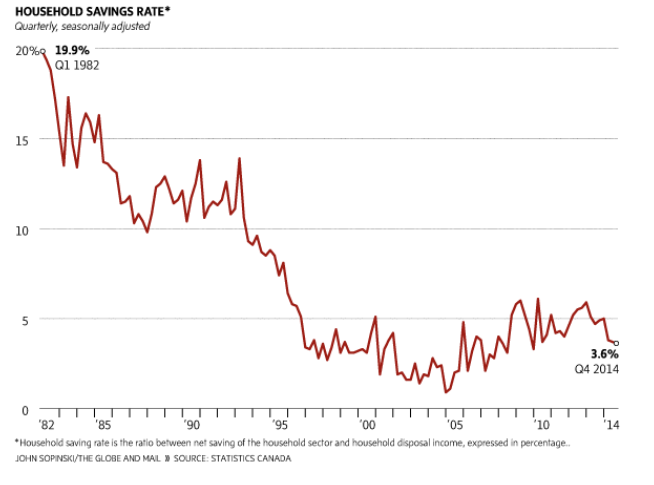

But we should all keep in mind how often a dollar that is earned, invested and spent again will be taxed. Income taxes come off your earnings, capital gains and dividend taxes will be carved from your investments, and sales taxes will be collected when it is spent again. TFSAs promise to relieve only one part of this equation, we should welcome even this small relief. Canadians in particular have need of it. Our savings’ rate is pitifully small, and has been declining for decades. The number of Canadians without pensions and suitable retirement funds is alarmingly high, and we have no simple solution to fix any of it. Decreasing long term tax revenues in favour of creating better savings opportunities isn’t a crime, it’s a blessing, one that we can all benefit from.

Great article. Justin Trudeau is a joke!!!

Sent from my iPad

>