A correction is typically defined as a drop of roughly 10% in the markets over a very short period of time. It’s often “welcomed” by investment professionals because it creates opportunities for new investments into liked companies that were previously trading above valuations considered appealing. Corrections are talked about as being necessary, beneficial and part of a normal and healthy market cycle, which all makes it sound somewhat medical. But in medical terms it falls under the category of being told your are about to receive 5 injections in short order and they are all going to hurt.

A correction is typically defined as a drop of roughly 10% in the markets over a very short period of time. It’s often “welcomed” by investment professionals because it creates opportunities for new investments into liked companies that were previously trading above valuations considered appealing. Corrections are talked about as being necessary, beneficial and part of a normal and healthy market cycle, which all makes it sound somewhat medical. But in medical terms it falls under the category of being told your are about to receive 5 injections in short order and they are all going to hurt.

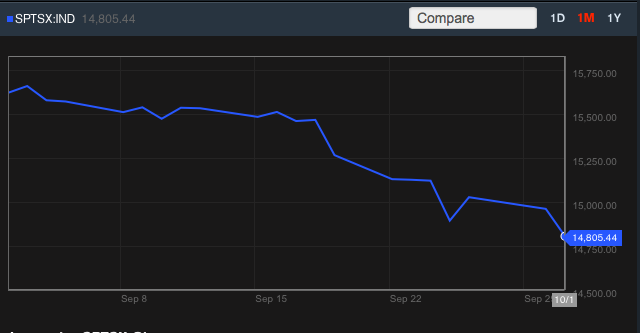

For investors the past couple of weeks in the market has felt like many such injections. The US markets have had a significant sell off, as have the global, emerging, and Canadian markets. All of it very quickly. The sudden drop has erased many of the gains in an already slow year and eaten dramatically into the TSX’s return which had been one of the best.

For many investors any sudden change in the direction of the markets can immediately give the sense that we are heading into another 2008. As Canadian (and American) investors are now 6 years older and closer to retirement the stakes also seem much higher. So here are some reasons why you shouldn’t be concerned about the most recent market volatility, and what you can do to make them work to your advantage.

1. Everyone is nervous.

For several months people have been calling for a correction. Investor sentiment is neutral and consumer confidence has dipped, meaning that overall atmosphere is somewhat negative for the markets. But that can be a good thing. Market crashes and bust cycles typically show up when people are exuberant and feel euphoric about markets. Bad news is swept aside and the four most dangerous words in investing “This time it’s different” become the hallmark of the new bubble. It’s rare that negativity breeds an over exuberant market.

2. The Economy isn’t running on all cylinders.

There certainly have been encouraging numbers in the United States, and even recently Canada has had some improved economic numbers, but by and large there hasn’t been a big expansion yet in the economy. Unemployment is still high, especially in Europe and the labour force has shrunk (which can skew the unemployment numbers) while corporations continue to sit on enormous piles of cash, to their detriment. A market crash usually follows an overheated economy that begins to over-produce based on faulty views about future growth potential. That isn’t where we are yet.

3. Corporations are really healthy, and so are investors.

Canadians may still have bundles of debt, but the US is a different story. American corporations and households have been heavily deleveraging since 2008. In fact corporations in the US look to be some of the healthiest in decades, showing better earnings to debt ratios than previously thought. Crashes have as much to do with over-production as they do with out-of-control borrowing. The two go hand in hand and both factors are currently missing from the existing economic landscape.

4. Energy is cheap. Like, really cheap.

Remember when oil was more than $100 a barrel? High energy prices, and the expectation of future high energy prices can really put the kibosh on future returns and throw cold water all over the market. As we’ve previously said, energy is the lifeblood of civilizations and a steady supply of affordable energy is what separates great economies from poor ones. (Look, we tweeted this earlier! See, twitter is useful. Follow us @Walker_Report)

https://twitter.com/Walker_Report/status/517604263493894145

The arrival and growth of American gas production combined with changing technologies and increasing efficiencies on existing energy use means that global demand is slowing, while global supply is increasing. In fact in March of last year, the head analyst for energy at Citigroup published a paper describing exactly this trend of improved efficiency with new sources as a mix for lower energy prices in the long term. Whether this proves true over the next two decades is hard to say, but what is true is that cheap energy helps economies while expensive energy hinders it. Since economies have already adjusted to the higher price over the last few years, a declining price is a tailwind for growth.

Does this mean that there aren’t any risks in the market? Absolutely not. Europe is having a terrible year as a result of persistent economic problems and Russian intransience, and many Emerging Markets are showing the strain of continued growth, either through corruption or exceeding optimism about the future. Those pose real risks, but taken in the grand scheme of things our outlook remains positive for the markets.

How can I make this all work for me?

So what can you do as an investor to make a correction benefit you? The first piece of advice is always the same. Sit tight. Dramatic changes to your investments when they are down tends to lead to permanent losses. Secondly, rebalance your account periodically as the market declines. On the whole equity funds will lose a greater proportion of their value than fixed income, leaving a balanced portfolio heavier in conservative than growth investments. Rebalancing gives you a chance to buy more units of growth funds at a lower price while adding greater potential for upside as the market recovers. Lastly, if you have money sitting on the sidelines, down markets are great opportunities to begin Dollar-Cost-Averaging. For nervous investors this is a great way to ease into the markets even as markets look unstable. You can read about it here, but I recommend watching the movie below for a nice visual explanation. Now, take your medicine.