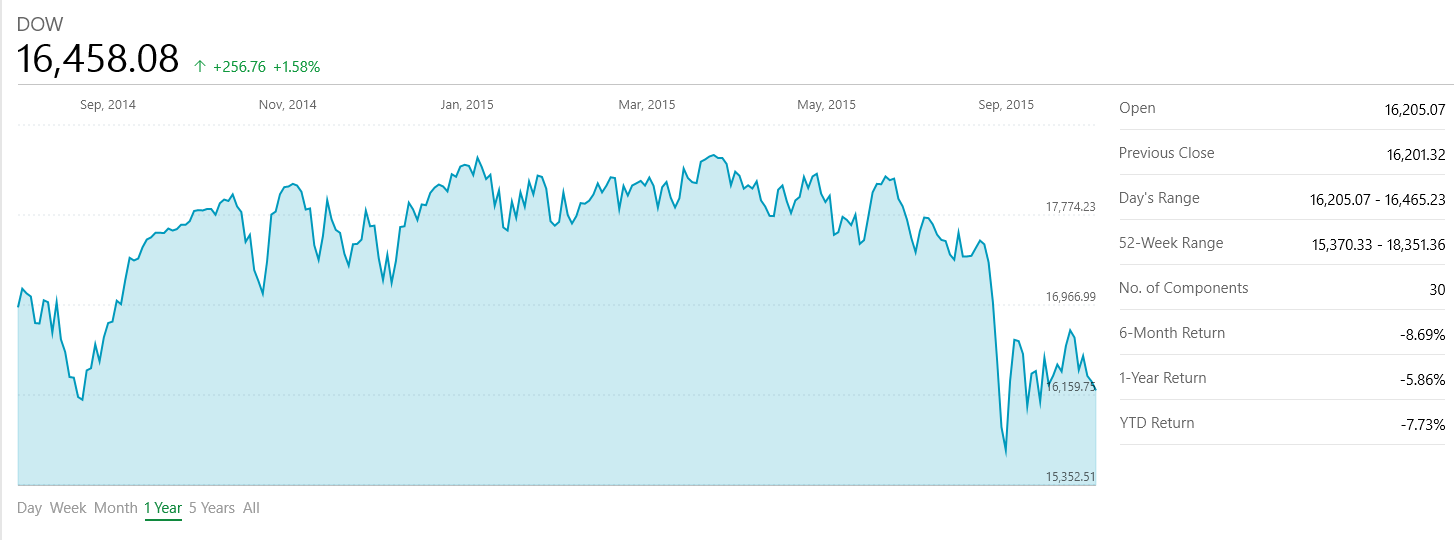

Over the past month it would seem that all hell has broken loose on global markets. A generous explanation might use the phrase “increased volatility” while a more pessimistic reading would say that we are heading for another global recession. Either way, people are nervous and money is being pulled out of the market by investors in droves. Year to date returns off of major indices are all negative. The TSX and the Dow are both -8% for the year while the S&P 500 is -5.5%. So what is happening?

The earliest threads for the most recent round of economic confusion date back to last year, when the price of oil began to fall. Normally falling oil is a welcome sign but in the economic climate we are in, one desperate to see some inflation, falling oil just meant more deflationary pressure. The plummeting oil price also hit a number of economies quite hard. Resource rich economies like Canada, Russia and Venezuela all took it on the chin. The falling price has been exasperated by the Saudi price war against the burgeoning US shale production.

For many investors a falling oil price also seemed to shine a light on a declining need for oil, not one born of environmental concern, but of a falling global demand. That leads us to the current problem with China. China’s problems are likely vast and not well understood yet. There is secrecy around the Middle Kingdom when it comes to economic matters, but it is likely that the Chinese are not immune to the same kind of avarice, greed and hubris that usually underlies most market bubbles. The Chinese have had a stock market collapse that has been followed by increasingly grim statistics and a revisit of the overbuilding narrative that has followed on the heels of China’s economic success.

The final piece of this puzzle was the looming interest rate hike from the United States. Interest rates are closely tied to rates of inflation and are important tools for governments in trying to mitigate recessions. Since the United States has had a near 0% interest rate there is some eagerness to push the rate up and give the Fed some options if the market sours. But critics have spent most of the year worried about a rate hike, citing the strengthening dollar and weak inflation rate as reasons not to do it. When the Federal Reserve took that advice though and opted to postpone the rate hike last week, the response of immediate joy was overwhelmed by the sudden realization that perhaps the US economy was not strong enough to withstand a rate hike and the global economic picture was far worse than previously thought.

Whether this means we are actually heading for a recession, it’s too early to say. No one knows what is really going on, but the sentiment, what people believe is going on, is resoundingly negative. Combined with an aging bull market and the highly liquid nature of investing has meant that there is simply more volatility in the markets than before.

Looking over the business news is little more than a guessing game informed by various analysts about what is (or is not) happening. But the best question that investors should be asking themselves is what do they need to have happen to their investments? While no one is looking to lose money, retirees and pre-retirees need to give real thought as to whether their investments suit their financial needs over the coming few years, and what kind of financial storm they could weather. So the smartest thing you can do regarding your investments is call up your advisor and discuss your investment strategy going forward.