For the past few weeks I’ve been struggling to capture what’s been happening in markets since late January. There has simply been so much that it is hard to succinctly cover it all in a single blog post.

So instead, toady I hope to touch on one thing that should stand out to us, the potential end of an investing strategy that is so standard it is reflected in almost every corner of the financial services world, from mutual fund companies to robo-advisors to banks.

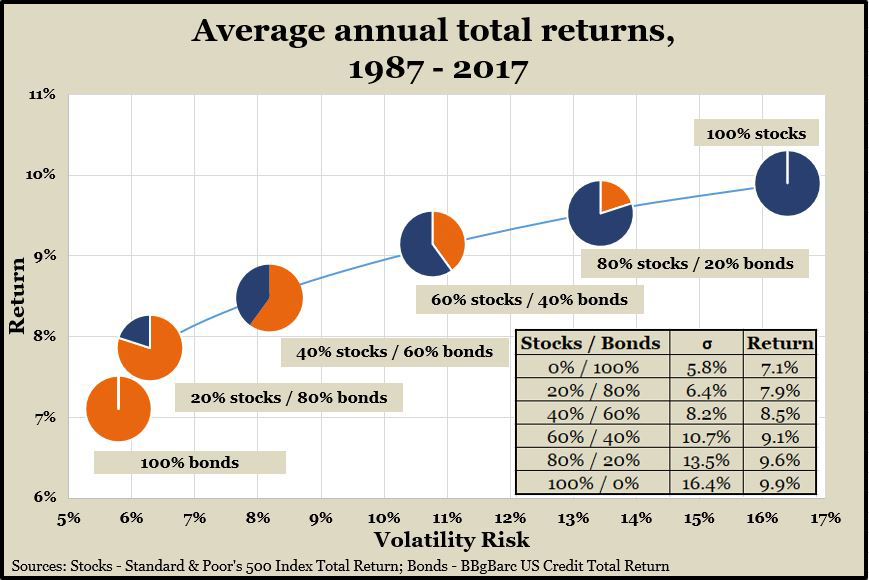

The 60/40 split, or balanced portfolio, is the general go to solution for steady returns. The principle is simple: 60% of a portfolio is weighted towards equities, that is stocks in companies, mutual funds or ETFs, and the remaining 40% goes towards fixed income; a collection of bonds or other “safe” investments that pay some income in the form of mutual funds or ETFs.

This is a wide space to play in. Within the stock or equity portion, a portfolio may have exposure to any number of companies, sectors, or geographies. Similarly, the fixed income component can have government debt, corporate bonds, T-bills, mortgage securities, either domestic or foreign, in short or longer durations. The individual positions may have short term impacts on performance, as some investments will outperform for limited stretches, but the general architecture of the portfolio should see relatively stable and consistent returns over time with an acceptable level of risk for the majority of investors.

This wasn’t just speculation. It had some math behind it, explained in the form of the “Efficient Frontier”, a curve that showed the relation of risk to return and aimed to help identify an optimum portfolio based on these two metrics. The goal was to maximize the amount of return for the risk undertaken. Its easy to get lost in the weeds here, but if you’re ever interested you can read up on Modern Portfolio Theory or Harry Markowitz. Put simply, the lesson the industry took was that a diversified portfolio of investments, with rough weightings of 40% in fixed income and 60% in equities would largely suit most people.

It’s worth asking why this is. And the answer has a lot to do with buying a house in the late 1970s and early 1980s.

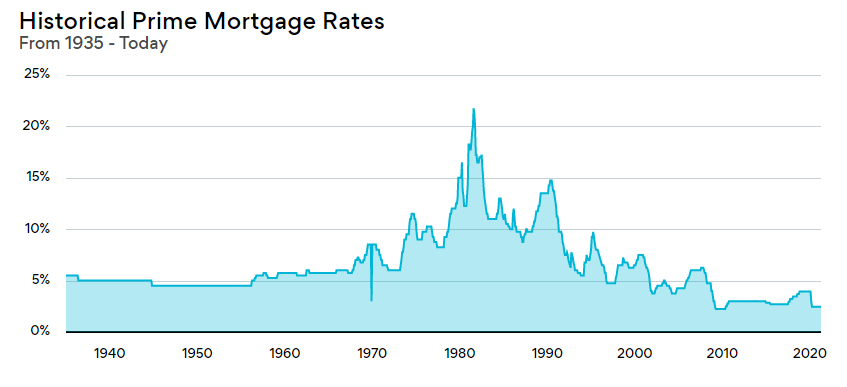

As anyone who remembers 8-tracks will tell you, buying a house in the early part of the 80s was expensive. 5-year fixed rates were 20%, or more. According to the website ratehub.ca, the prime lending rate in Canada peaked at around 21.75% in August of 1981. By comparison, my current 5-year mortgage is a whopping 1.8%. In 1981, you could buy a Government of Canada 10-year bond with a coupon rate of 15.3%, and a 5-year GIC with a rate of 15.4%. Today a 10-year government of Canada bond has a yield of 1.51% and the most generous GIC I can sell is 1.96% from Haventree Bank with a minimum deposit of $50,000.

Okay, so what’s the connection?

The issue here is not just that buying a house cost more when it came to lending in the 1980s, but that the cost of lending itself has been falling for the last 40 years. We tend to think of bonds as an investment you buy, when in reality they are a loan you are making that can be traded on an open market. So imagine you were building a bond portfolio in the early 1980s, and the average yield of that portfolio (the interest you will receive based on what you paid) is 15%. It’s very safe, made entirely of Canadian 10-year bonds. Now, three years pass and a new 10-year bond from the GoC has a rate of 12.3%, what’s the effect on your bond portfolio?

It’s good news! It’s worth more, because for the next 7 years your bonds will pay 3% more than any new bond issuance. By 1986 a 10-year bond was paying 6% less per year than your portfolio. For the last 40 years the cost of borrowing has continued to decline, and the result has been to make bonds issued in previous years more valuable. And so, while there may have been fluctuations in returns over short periods of time, by and large a portfolio of bonds returned not just income, but also capital gains as older bonds were worth more with each decline in the cost of lending.

Today the cost of lending is low. Very low. Central bank lending rates for Canada, the United States, and the ECB are 0.25%, 0.25% and 0% respectively. A 30-year government of Canada bond has a current yield of 1.948%. In other words, were you to buy that bond today, the most you would earn is 1.948% on whatever you paid for the next 30 years.

But remember, bonds are traded on an open market. This means that the value of a bond fluctuates with its demand, and with it the return the bond gives. So, if you think that 1.948% is not enough interest to warrant buying the bond and the broad market agrees with you, the price of the bond should fall enough to push up the yield (for reference, the yield is the interest paid by the bond, divided by its price) until it pays enough interest to warrant investing. And that is what has been happening this year. Government bonds in the United States have been dumped as investors expect stock markets to do well and bond yields are considered too low. And as the bond price falls, the yield the bond pays goes up in relation to the decline of the price, and with it sets a borrowing rate investors are more comfortable with.

What this means for portfolios is that the 40% allocated to bonds is now very vulnerable to both investor sentiment and future rate hikes by central banks. With borrowing rates already at rock bottom both of these risks seem likely, and it’s left the traditional “balanced portfolio” exposed when it comes to reducing risk through different asset classes.

You might assume that this is a new problem, but it isn’t. Risk has been growing and portfolios have been evolving in complexity to meet the needs of investors for the last few decades. Much of this has happened on the equity side of portfolios, with investors demanding, and ultimately gaining access to a much wider range of investable products since the 90s. The period where you could have a portfolio made up of just Canadian dividend paying stocks ended long ago, and in its place, portfolios now hold a variety of investment products with access to large cap, small cap, US, North American, global, international, Emerging Markets, Frontier Markets, sector specific investing, thematic investing, commodities, dividends, value, growth, and growth at a reasonable price. Bonds have undergone a similar transformation, with investors moving from government bonds, to corporate bonds, to junk bonds (bonds with lower quality ratings and potentially higher default rates) both domestically and globally.

Today, to achieve a return of about 6.5%, the average investor is taking on risk at a much higher rate than they would 20 years ago. In 2000 a 6.5% return could be achieved with a portfolio of exclusively bonds. 20 years later a 6.5% return would require a much larger range of positions, including US stocks (large and small cap), real estate, private equity and would have a relative level of risk of more than double (almost three times!) the 2000 level. The above changes to the bond market will only mean more risk and more volatility for investors.

I’m reluctant to ever declare something “dead” or “over”. That language betrays too much confidence about tomorrow, but financial history is much longer than most people appreciate and is filled with disruptions and the ending of economic certainties followed by the arrival of new paradigms. Whether it is the bankrupting of the Medicis, or the popping of a tulip bubble, economic realities can change. The “balanced portfolio” with its 60/40 mix, has been a cornerstone of simplified investing, a “go-to” solution that has made mass investing using discount platforms affordable and easy.

In an ideal world we might wish that investing was more “set it and forget it” than not, but long-term data and averages obscure the reality for many people. In the last ten years we’ve seen two serious “once in a lifetime” events that have shaken markets and governments. Investors, no matter what their stripe, whether they prefer robo-advisors, bank products or a personal financial advisor like myself, should be cautious that the rules to successful portfolio building are immutable.

Fantastic review of portfolio theory placed in today’s interest rate environment. Reassuring that the efficient frontier is still a valuable theoretical tool.

Thanks