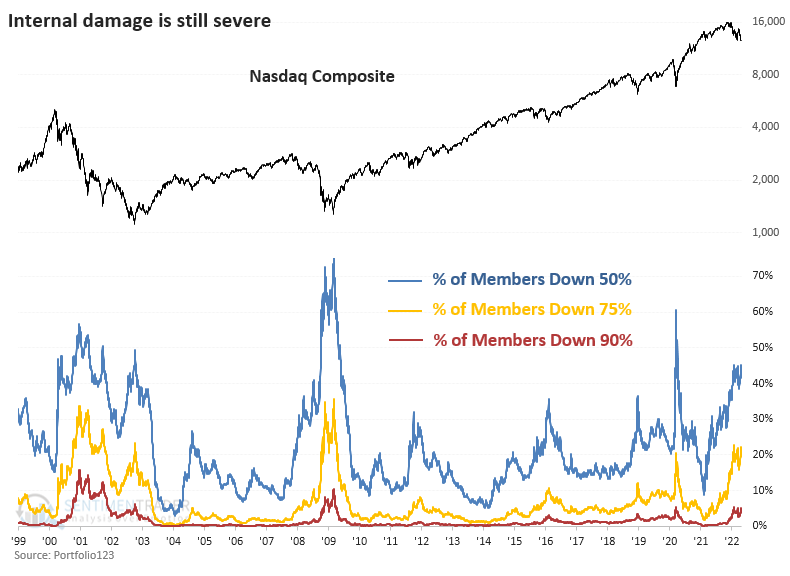

Markets have been falling through the year, and despite some encouraging rallies the trend so far has been decidedly negative. The NASDAQ Composite, one of the three big indexes heavily tilted towards technology companies had a -23.86% YTD return as of Monday, May 16th, a minor recovery after it had reached a low of -27% on Thursday of the previous week. The Dow Jones and the S&P 500 have YTD returns of -10.31% and -14.82% respectively. The question for investors is “what to do?” in such markets, especially after some of the best years despite the pandemic.

A closer inspection of the markets however shows that while there have been some steep sell offs reflected in the broad market, the real market declines have been far more concentrated. And while there are many different market headwinds to choose from when it comes to reasons for the recent selling action; inflation, interest rates, geopolitical strife, COVID-19, maybe even Elon Musk, the sector that has been sending markets lower has been the tech sector.

Over the past couple of years the companies posting the biggest gains in the markets have been tech companies. Apple stock (AAPL) was up 88.97% in 2019, 82.31% in 2020, 34.65% in 2021, and is down -11.6% so far in 2022. Amazon (AMZN) was up 76.26% in 2020, and has fallen -30.18% this year. Facebook, now META Platforms (FB) gained 56.57% in 2019, 33.09% in 2020, 23.13% in 2021 and has lost -38.08% in 2022. Netflix was up 67.11% in 2020, and a further 11.41% in 2021 but is down -68.74% this year. Tesla, which had an astounding 743.4% gain in 2020 and another 49.76% return in 2021 is so far down -17.36% in 2022, how long can it resist gravity? (All prices and YTD performance were collected from ycharts.com on May 6th, 2022).

I predict that we may never fully understand how the pandemic changed thinking and why stock prices climbed so much, but the reality was that many tech companies benefited from people staying home, going online and the changing priorities that coincided with not having to be in offices and commuting. Tech companies that became huge like Shopify (SHOP), which allowed traditional retailers to become online retailers, benefitted immeasurably from the lockdowns. But it too has seen its stock decline this year by -69.59%, pushing the price back to where it was in December 2019.

Because the tech sector has become so large, particularly in the NASDAQ, the retreat of these companies carries big implications for indexes and by extension the wider market as well. As markets fall, it encourages investors to panic sell, aided and abetted by the army of computers that help multiply the effects of momentum selling. This is especially true as investors have migrated to low-cost passive index ETFs, a trend so noticeable that experts worry it might be warping the market as investors worry less about the value of individual companies and instead pile money into broad indexes with no quality filters.

Markets are facing other risks too. Inflation, which seems to be running at about 8%, can threaten economies as people buy fewer items due to cost increases. Interest rate hikes, which are meant to ultimately curb inflation by restricting monetary supply and reduce lending/economic activity have hit bond markets particularly hard. Higher interest rates mean higher borrowing costs, and its here we might hypothesize about some of the unintended consequences of the incredibly accommodative monetary policy that the pandemic introduced. That might be that investors were able to borrow to invest, and the threat of both rising interest rates and stumbling returns will only hasten the exit of money from the market by some investors. Higher borrowing costs will also have another impact on markets, as a sizeable amount of stock market returns over the past decade have come from share buy backs, funded in part by low-cost borrowing.

Having said all that, economies are still looking very strong in the present. Earnings have remained high, jobless claims continue to fall, and while we’ve seen a spike in costs the ability to address those inflationary pressures may not be something that can be easily done through monetary restricting.

There are many different sources of inflation, but two significant issues are not connected to “cheap money”. Instead we have issues that are primarily structural and represent the failure of political foresight. The first among these has to do with oil. Since the price of oil fell in 2014, infrastructure development has stalled, heavily indebted producers have retreated, and now Russia has been closed off from much of the global market. This confluence of events has unfortunately arrived as economies are reopening, global use nears pre-pandemic levels, and global refined supply is at historic lows. There is no simple solution for this, as the only remedy is time (and development). In theory, Canadian and US oil could make up much of the global need, but for a multitude of reasons neither country is in a position to rapidly increase production.

Similarly, supply chain disruption and the heavy reliance on offshore manufacturing have meant that there is no simple solution to production problems occurring in other nations. China is the key issue here, with an enormous grip on much of global supply on many items and their current insistence on a “Covid Zero Policy” China is effectively shut to global business. This means ships can’t get into port, and with-it products cannot make it to market.

Higher borrowing costs seem unlikely to handle this problem. High gas prices and lack of supply may be inflationary, but high borrowing costs can’t target those issues. Instead, higher interest rates and the threat of more in the future are hitting the parts of the market that have been pushed higher by cheap credit. The stock market and the housing market.

If markets seem to be moving independently of economies, its possible that won’t stay that way for long. As previously mentioned, higher energy prices are not controllable by higher lending rates. But higher energy prices can introduce demand destruction, a fancy way of saying that economies shrink because prices get out of control. Oil is still in high use and its needs go far beyond powering cars. In fact internal combustion engines only account for 26% of global oil need, meaning those higher prices for crude, if they get too high, can have wide inflationary impacts to the entire economy.

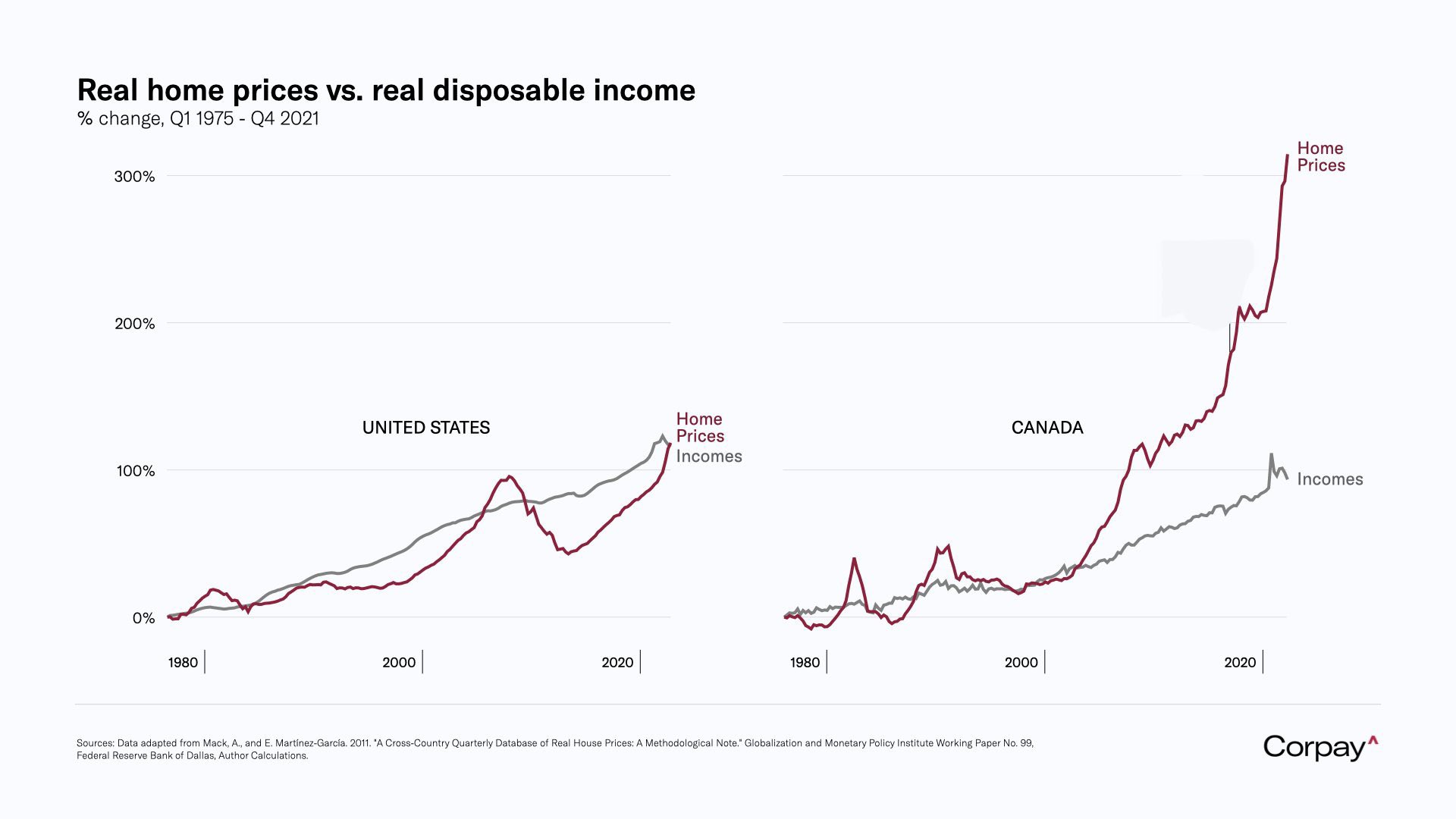

Higher lending rates may also lead to a substantial economic reset, especially for Canadians who have much of their net worth tied up in their homes. With almost 50% of new mortgages in Canada variable rate mortgages, home prices having skyrocketed in the past few years and with most Canadian debt connected to homes, the risk to home owners is very real. Can the Bank of Canada tame inflation, orchestrate a soft landing for the housing market and keep the economy chugging along? Such a question invites highwire act comparisons.

So what’s happening with markets? Perhaps we are simply correcting a narrow subset of the market that got too hot through 2020-2021. Perhaps we are seeing the dangers of printing too much money. Perhaps we are seeing the realities of people buying too many index ETFs. Perhaps we are witnessing people being too fearful about the future. Perhaps we are too fearful of inflation or interest rates. Perhaps we are on the brink of a recession.

Perhaps, perhaps, perhaps.

But let me offer a slightly different take. Investing is frequently about connecting your needs as an investor with the realities of the world. As Warren Buffet famously said, in the short term the stock market is a voting machine, in the long term a weighing machine. If you can afford risk, you can be risky, and with that comes the potential for significant market swings. If you can not afford risk, then your portfolio should reflect that need. If you cannot stomach bad days, potentially weeks or even months of bad news, then you need to find a way to keep your investment goals aligned with your risk tolerance.

When I started this essay we had just completed one of the worst weeks of the year, which bled into the second week of May. As I finish this piece markets are in the process of rallying for a third day, posting modest gains against the backdrop of significant losses. It would be nice if I could end this with some confidence that we’ve turned a corner, that markets had bottomed and that the pessimism that has led to so much selling is evaporating as people come to recognize that stocks have been oversold. Yet such prognosticating is the exact wrong tack to take in these markets. Instead, this is a good time to review portfolios, ensuring that you are comfortable with your risk, that your financial goals remain in sight and that the portfolio remains positioned both for bad markets, and for good ones too.

If you have any concerns about how your portfolio is positioned and need to review, please don’t hesitate to contact us today.

Walker Wealth Management is a trade name of Aligned Capital Partners Inc. (ACPI)*

ACPI is regulated by the Investment Industry Regulatory Organization of Canada (www.iiroc.ca) and a Member of the Canadian Investor Protection Fund (www.cipf.ca). (Advisor Name) is registered to advise in (securities and/or mutual funds) to clients residing in (List Provinces).

This publication is for informational purposes only and shall not be construed to constitute any form of investment advice. The views expressed are those of the author and may not necessarily be those of ACPI. Opinions expressed are as of the date of this publication and are subject to change without notice and information has been compiled from sources believed to be reliable. This publication has been prepared for general circulation and without regard to the individual financial circumstances and objectives of persons who receive it. You should not act or rely on the information without seeking the advice of the appropriate professional.

Investment products are provided by ACPI and include, but are not limited to, mutual funds, stocks, and bonds. Non-securities related business includes, without limitation, fee-based financial planning services; estate and tax planning; tax return preparation services; advising in or selling any type of insurance product; any type of mortgage service. Accordingly, ACPI is not providing and does not supervise any of the above noted activities and you should not rely on ACPI for any review of any non-securities services provided by Adrian Walker.

Any investment products and services referred to herein are only available to investors in certain jurisdictions where they may be legally offered and to certain investors who are qualified according to the laws of the applicable jurisdiction. The information contained does not constitute an offer or solicitation to buy or sell any product or service. 16 Past performance is not indicative of future performance, future returns are not guaranteed, and a loss of principal may occur. Content may not be reproduced or copied by any means without the prior consent of the author and ACPI.

Nice job!