The most immediate reason is the concentration of market leadership. The “Magnificent Seven” tech giants now account for more than 35% of the S&P 500, while the top ten companies make up nearly 40%. The gap between the S&P 500 and its equal-weighted equivalent is just shy of 10%, while the Magnificent Seven themselves have delivered a combined return of roughly 27.6% year-to-date. The comparison to the dot-com era is easy to make, but the fundamental difference is profitability: Apple, Google, Microsoft, Amazon, Meta and others continue to generate substantial earnings and hold enormous balance-sheet reserves. This profitability has helped anchor market confidence.

Figure 1 Growth of the Magnificent Seven as a part of the S&P 500

Another factor is the lag in how economic data reflects policy changes. Despite the risks tariffs pose, the full impact has not yet shown up in backward-looking data like GDP or employment reports. Investors expecting an immediate shock instead found resilient quarterly numbers, reinforcing confidence rather than shaking it.

Figure 2 Effective tariff rates over time, from the Yale Budget Lab

Figure 3 Widening wealth disparities between households and consumer spending

This combination — delayed data effects, high concentration of consumption, and sustained AI investment — has helped keep investor sentiment resilient, even as negative signals accumulate beneath the surface. It has also masked the risks of allowing speculative dynamics to develop largely unchecked.

Figure 4 Growth of Personal Consumption as a percentage of GDP

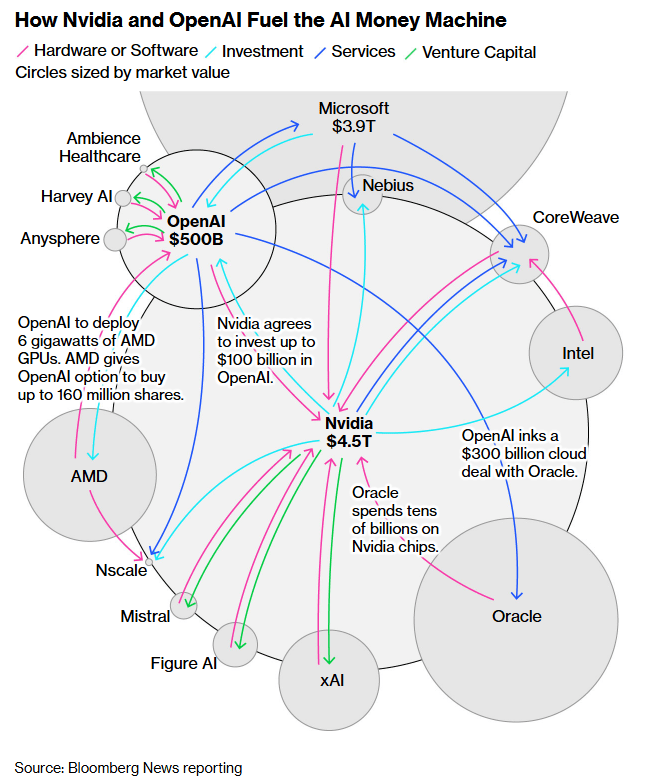

Concerns about an AI bubble are growing. Estimates of total AI investment now exceed $3 trillion when considering capital expenditures, valuations, and related infrastructure spending. Commercial use cases outside of a few sectors remain limited. Some firms have begun participating in “circular funding arrangements,” where they invest in each other’s AI initiatives to reinforce perceived valuations. Even industry leaders acknowledge the speculative environment: Sam Altman, the CEO of Open AI has said there is likely a bubble, while Jeff Bezos has called this a “good bubble” that will still produce transformative breakthroughs.

History suggests that speculative cycles are remarkably resistant to logic. They often convert skeptics into participants, including professional money managers who join in under client pressure. Market bubbles resemble the proverbial frog in a pot: the danger rises slowly enough to dull caution.

Yet they also resemble the “watched pot” that never seems to boil. As long as new capital continues to flow into AI-linked investments, momentum can persist. Predicting the end of a bubble is famously difficult — markets can remain irrational longer than investors can remain solvent.

So what should investors do? Awareness of rising risk is the starting point. We may not be able to time the end of the AI boom, but we can examine investor behavior for signs of speculative excess.

Consider Tesla. After the election, the stock surged nearly 98% in six weeks on enthusiasm linked to political alignment and narrative momentum. Since then, sales have weakened, profitability has declined, and competition has intensified — yet the stock remains 10% above its level on inauguration day and has more than doubled off its lows. Tesla’s valuation continues to reflect belief in future breakthroughs rather than current operational performance. It is a clear illustration of narrative overpowering fundamentals — a hallmark of speculative markets.

Figure 6 Tesla stock performance from November 4, 2024 to November 4, 2025

If this environment feels uncomfortable, it may be time to review portfolio risk exposure. Reducing equity risk comes with trade-offs — especially missing out on momentum-driven gains — but clarity on long-term goals can help prevent emotionally driven decision making.

Market manias are difficult to avoid and even harder to detach from when others are benefiting. The antidote is a disciplined investment plan that emphasizes long-term objectives over short-term excitement. In a world where the water may be warming around us, it is better to be a watcher than the frog.

These are just some of the headlines and subjects floating around the internet. Depending on who you are and where your political allegiances lay, the answers will be self-evident. Trump is either a an economic genius and unparalleled negotiator, or he is a clumsy and indifferent conman masquerading as successful businessman and politician.

For investors this presents a real challenge. These questions aren’t just thought experiments. Depending on the answers they may significantly impact where one chooses to invest, and the more polemical the question the farther we may get from a useful answer, regardless of politics. If our goal is to ask questions to reveal truth, we may find ourselves confused as to why markets have surged back from their lows (as of May 12th the major US indices have almost recovered from their tumble at the beginning of April) even while business reporting warns of a potential for a worsening economy.

One way to make better sense of what’s happening is to put ourselves in the shoes of Donald Trump’s administrative allies. Imagine what someone who believes in what Donald Trump is doing would say about his economic plans. Its not as though they haven’t heard economists and businesses express doubt and worry about the actions of his administration. So how would they defend them?

In my imagining I believe they would argue something like the following:

The United States is enormously rich but wastes money on cheap goods from China, and while some of these goods don’t need to be made here, America has lost enough manufacturing jobs that its worthwhile experimenting with tariffs to bring jobs back. Over the past 45 years we’ve seen countless evidence that playing by the rules of globalization reduces the ability of governments to help their most vulnerable citizens, and money has become too fluid and too willing to cross borders at the expense of their domestic homes. Regardless of what people fear, America remains the richest country in the world, with the largest consumer base, and that combined with the existing strength of the US economy will be enough to bring industry back to the US in some capacity while tariffs on junk from other countries will help pay for renewed and permanent tax cuts. Market volatility will be temporary while the economy realigns itself, but the combination of lower taxes and existing economic strength will ultimately help lift the markets even higher.

You don’t have to believe in such a claim, or even pretend this was what Donald Trump campaigned on. What I’m putting forth is a set of ideas (picked up through numerous interviews and speeches) that I believe his administration finds largely defensible and recognizable, and would be a better frame of reference for understanding their actions. Let’s start with the recent indication that GDP is contracting. In traditional economic terms, two quarters of back-to-back GDP contractions constitute a recession. We’ve had more than a few of those over the past decade, but few people would say that we’ve had recessions. The reason for this might be best expressed by Jason Furman; an American economist, professor at Harvard, and former deputy director of the US National Economic Council, in a recent editorial in the Financial Times. Outlining the importance of “Core GDP” vs “GDP”, he points out that Core GDP (actually known as Real Final Sales to Private Domestic Purchasers) better reflects consumer spending and private investment while the traditional GDP includes net exports, inventories, and government spending, all things in flux because of Trump’s new administration. So, while the GDP contracted in Q1 of this year, the Core GDP was up in the first three months.

What about rumours of empty ports and empty shelves? Reportedly Trump was shaken following meetings with the heads of three major retailers about shelves being empty if the tariff’s remain at 145% on China. Trump seems to have vacillated a number of times about the size and implementation of the tariffs, but as of today they remain intact. Asked about higher prices and fewer options Trump seemed dismissive of concerns over the Chinese trade war declaring “maybe the children will have two dolls instead of thirty dolls, and maybe those dolls will cost a couple of bucks more.”

Is Trump being dismissive? Yes, but he’s also not worried that shelves will be empty. Though shipping and imports are down as we head into May for cargo coming from China, far from alarmist rumours that docks are sitting empty there is still plenty of ocean-going traffic coming from China.

This discrepancy between a popular public impression and the on-the-ground economic reality gives room to Trump’s administration to continue ahead with ideas that remain controversial, as well as opening up investors to making mistakes in their allocations. For the time being, Trump does have a reservoir of economic and political strength to call on. He may be using that reserve up, but may also have guessed with some accuracy that the global economy will keep doing business with America regardless of whatever feathers he ruffles.

But markets may also not be calculating the longer-term direction correctly, mispricing assets and remaining too optimistic. Since Trump’s re-election markets have been shown to be placated by the promise of deferred tariffs, as though deferring them is really the prelude of getting rid of them. Trump doesn’t help this by going back and forth on their implementation, but listening to his words, and following his actions, I feel that it would be a mistake to assume that the tariffs will ultimately be rescinded.

This seems best exemplified by the announcement of the US-UK trade deal. Called “a starting point” by the British ambassador, the Trump administration has said the deal is “maxed out”, leaving in place a 10% tariff on British imports, with a reduced tariff on British cars, steel, and aluminum (the deal effectively lowers car and steel duties to the flat 10% rates, down from 27.5%).

Whether deals such as these are anything for the market to get excited about is a question that will be answered with time, like all the unanswered questions that have been introduced this year. What investors must work on is remaining clear eyed about what is happening, and resist submitting to their own partisan preferences. Trump may yet undermine the US economy, and trade deals may turn out to simply be acknowledgements of existing tariff rates, or perhaps the opposite may happen. But recognizing that reality is more mixed and that we do not yet have a clear picture about the future will promote more time tested strategies for sensible investing.

Aligned Capital Partners Inc. (“ACPI”) is a full-service investment dealer and a member of the Canadian Investor Protection Fund (“CIPF”) and the Canadian Investment Regulatory Organization (“CIRO”). Investment services are provided through Walker Wealth Management, an approved trade name of ACPI. Only investment-related products and services are offered through ACPI/Walker Wealth Management and covered by the CIPF. Financial planning services are provided through Walker Wealth Management. Walker Wealth Management is an independent company separate and distinct from ACPI/Walker Wealth Management.

This piece was meant to come out last week before the most recent tariff announcement. It was delayed, but the points it makes remain relevant.

Donald Trump’s actions since taking office have failed to deliver the kind of economic and market stimulation people had been imagining. For many professionals, business owners, and financial analysts, the assumption was that Trump would be good for markets and good for the economy. His other political views, like isolationism, tariffs, and sense of personal grievance weren’t great features, but he would fundamentally be bound by market and economic performance.

That faith eroded quickly as it seemed that Trump was intent on widespread and indiscriminate tariffs, targeting first America’s closest trading partners, and then reciprocal tariffs on the European Union, Great Britain, Australia, and Taiwan. Concerns that this might damage the American economy may have bought time on when those tariffs were to be implemented (as of writing Canadian and Mexican tariffs have been deferred twice, though Steel and Aluminium tariffs have gone ahead) but April 2nd remains “liberation day” according to Trump, a day when America stops getting “ripped off”.

Trump’s administration have pivoted away from the idea that Trump will be good for the immediate economy, and that a “period of transition” is on the way. During his speech to Congress (officially not a State of the Nation) Trump also said that farmers will sell more of their food to Americans, ostensibly a populist message but one more likely grounded in further declines of American agricultural export.

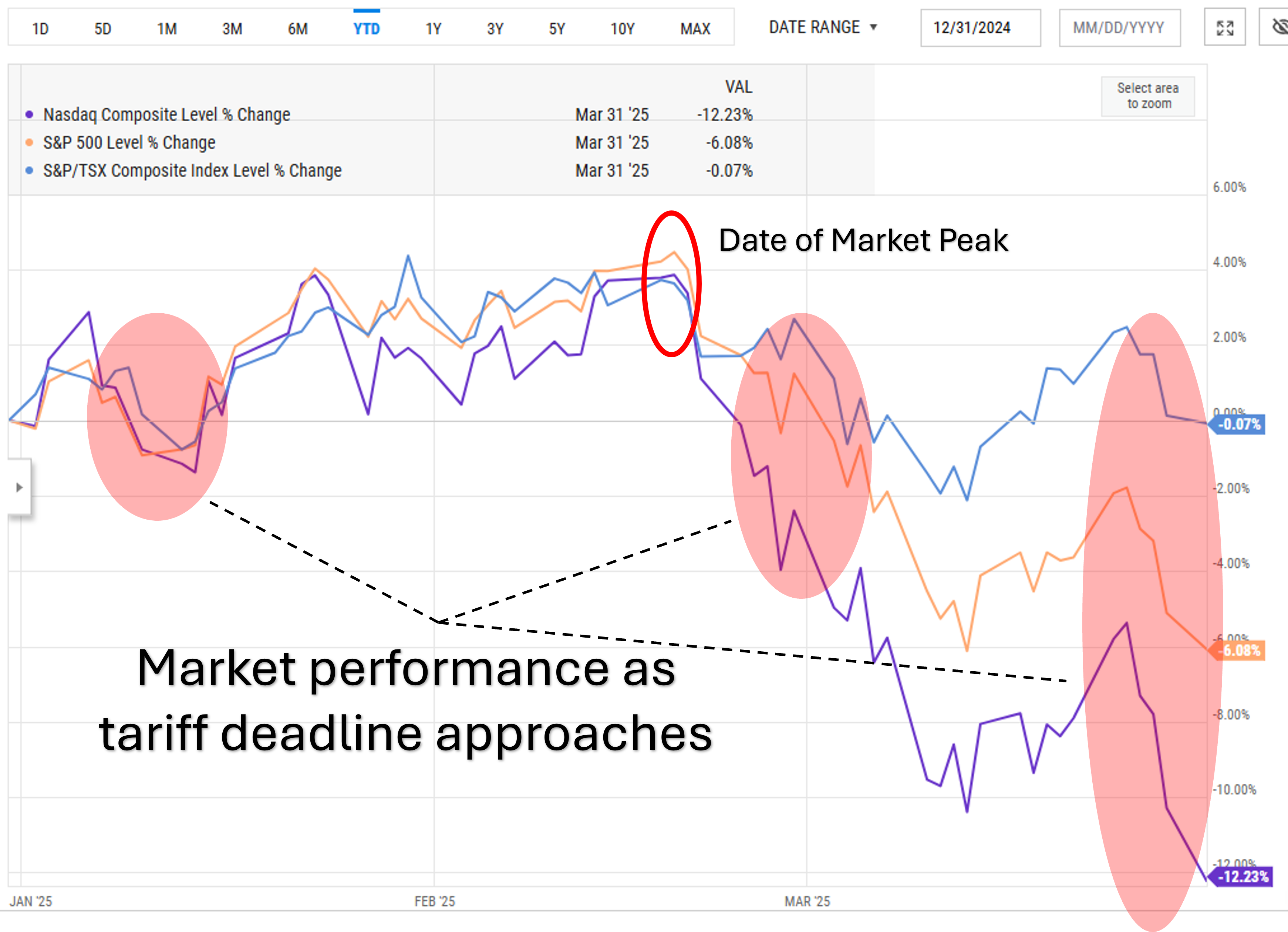

The markets peaked around February 19th, with the S&P 500 up 4.46% since January 1st. The Dow Jones had peaked a little earlier at 5.5%, and the Nasdaq Composite was up 3.86%, all respectable numbers for the first 45 days of a year, especially following a very strong 2024. Over the subsequent weeks markets began losing steam and saw a significant drop. From mid February to March 12th, a period of three weeks, the Nasdaq lost 13.05%, the S&P 500 9.31%, and the Dow 7.16%. Investors were worried, a recession seemed looming, and consumer confidence had plummeted.

Figure 1Market data provided by Y Charts. Data is until March 31, 2025

Yet only two weeks later markets seemed to have stabilised. Commentators were more confident and expected Trump’s tariffs to be more “focused”. Following some fairly significant government intervention, even Tesla’s shares regained some of their lost ground, and the bond market had retreated as investor enthusiasm seemingly returned. And then, at the end of last week the enthusiasm sputtered once again.

But these things have not yet fully come to pass. Trump’s way of engaging with government is dictatorial with a reality show slant. Rarely does he spell out what a policy will be and frequently defaults to the phrase “we’ll see what happens.” This level of uncertainty gives Trump room to maneuver, and allows the market to engage in its most common behavior; optimism. Trump may seem to be heading towards a recession, but there remains a chance he may change his mind. The market sell-off through February and March was not an indictment of Trump’s government. It was a reset on the risk for investors and an opportunity to reevaluate what might happen next. That leaves considerable latitude for Trump’s administration to back away from damaging policies, or double down on them.

Heading into 2025 it looked like the US economy was the strongest globally, and while the early days of the new administration seemed to have changed some of that math, what it means is that there is still lots of different ways that the year could still unfold. The United States may back away from its trade war, claiming victory with whatever concessions can be finagled. Elon Musk might be kicked out of the Trump inner circle, something that would certainly change the calculus about how the government would be run. Voters, which look considerably less impressed with Trump’s early policies, might be so angry that Republican members of the house find the nerve to push back on the administration. There are lots of potential futures.

For investors the challenge is to find a path that will allow them to navigate between the pessimism of Trump’s detractors and the optimism of his own administration. After so many positive years in the markets there is real wisdom in taking some of those profits off the table, and good investment policy hasn’t changed. Given the very strong performance out of the United States for the past five years, its likely that those investments have grown, especially relative to other equity positions. This is a good time to ensure that portfolios are well diversified and that assets are not too concentrated. Lastly, safety is something that should be given real thought to. Rob Carrick of the Globe and Mail wrote a piece arguing that if you need your money in the next five years, you should pull it out now. That advice should be tempered with a conversation with your actual financial advisor, but what all investors should be looking for is a blend of the following:

Enough equities to participate in good markets across the globe.

Enough safety that they won’t panic if markets do worse.

Enough cash to be able to take advantage of bad markets when they come up.

These three principles will look different for everyone, but should be balanced by the amount of risk you can absorb, and the ability to continue to meet your financial goals.

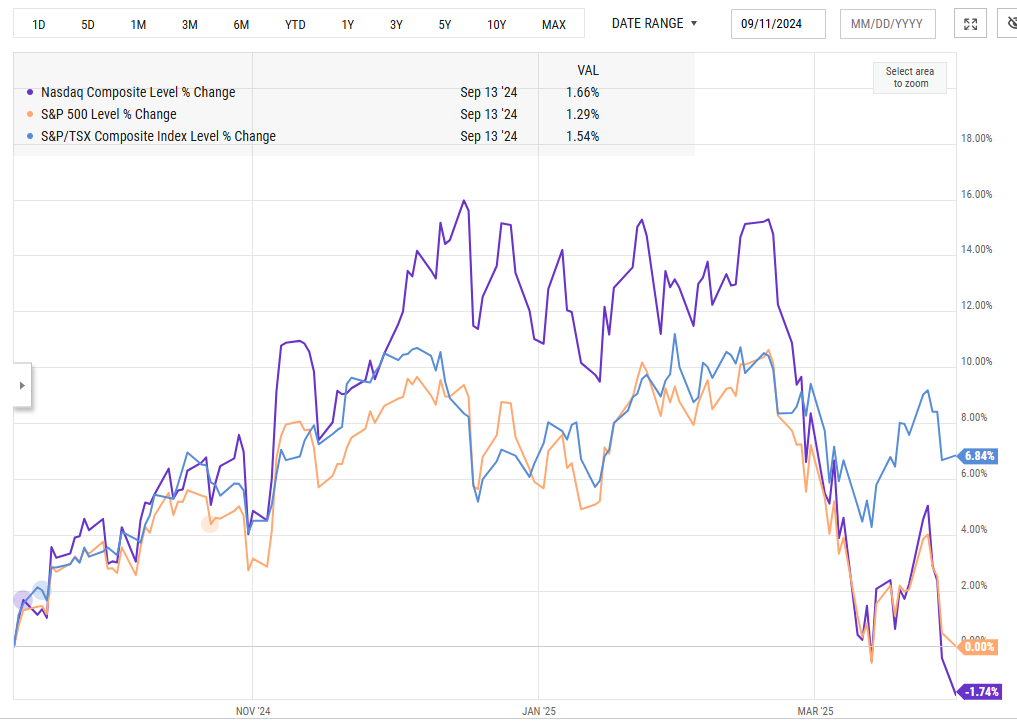

As we get closer to Trump’s “liberation day”, how much of Donald Trump’s policy agenda is well understood by investors is up for debate. According to Bloomberg, as well as some other news sources, retail investors followed a “buy the dip” mentality over March, while big institutional investors backed away. The market is not settled on what is going to happen, and while its tempting to say that little investors might take the biggest losses, there have been many instances of mistakes by large institutional investors. At the same time, there are many reasons to be cautious now. Though markets are off their all-time highs, they remain still at historic levels, and while the news has been quick to discuss “market panics” and “market crashes”, in truth we’ve only gone back to where we were in September. Investors should be on guard that markets can still go in either direction.

This leads to my final point. Investors will need to show patience in the face of the uncertainty. Followed to their natural ends, as I’ve outlined, many of his most aggressive policies don’t bode well for the future. But many of these policies may simply not come to pass. Markets may surprise people expecting the worst, and our own personal feelings about Trump and his administration’s actions may cloud our judgement about reality. What investors need to be is patient, and prepared.

Aligned Capital Partners Inc. (“ACPI”) is a full-service investment dealer and a member of the Canadian Investor Protection Fund (“CIPF”) and the Canadian Investment Regulatory Organization (“CIRO”). Investment services are provided through Walker Wealth Management, an approved trade name of ACPI. Only investment-related products and services are offered through ACPI/Walker Wealth Management and covered by the CIPF. Financial planning services are provided through Walker Wealth Management. Walker Wealth Management is an independent company separate and distinct from ACPI/Walker Wealth Management.

In 2016, Donald Trump supporters said that you should take him seriously, but not literally. His first press secretary, Anthony Scaramucci said “don’t take him literally, take him symbolically.” This defense of Trump was meant to highlight that while he may have said incredibly controversial things, much of that was just talk, and it was his message behind the words that you should really pay attention to.

But Trump himself has contradicted this view more than once, frequently saying “I don’t kid” when challenged on policy (the exact comment came about in 2020 over coronavirus testing). In other words, Trump has let people know that you shouldn’t be surprised when he does do things that seemed initially outrageous. For the wider world this has meant that you should take Trump at his word, and that even if some of his rhetoric is just that, rhetoric, you would be foolish to ignore the substance of his messages.

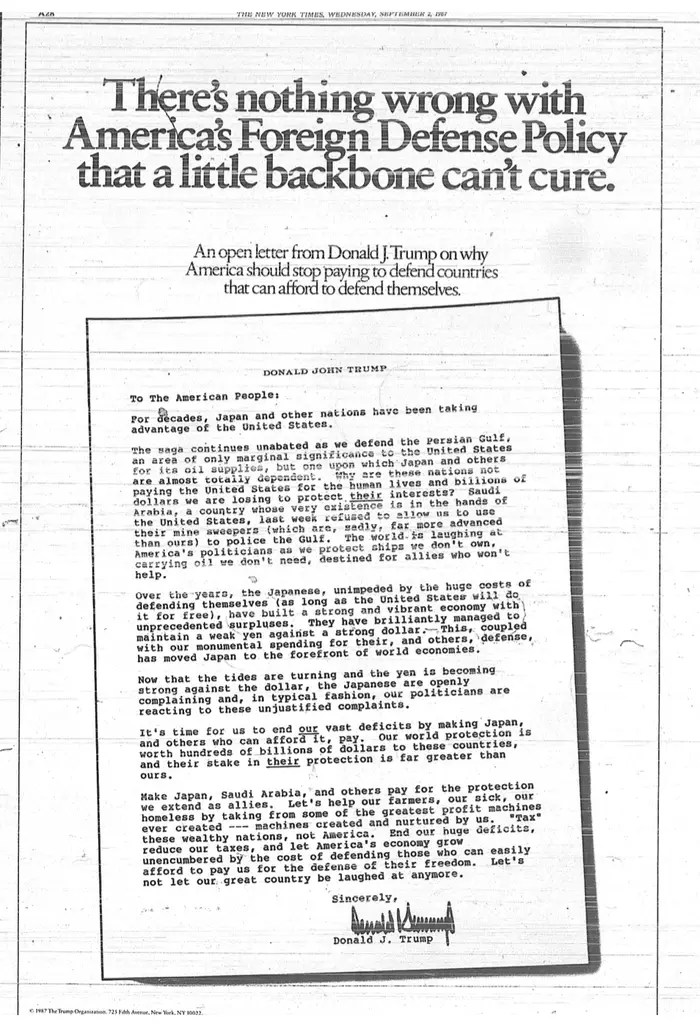

Since his re-election Trump’s focus has been squarely on tariffs, promising them on China (a further 10%), on BRIC nations (100%) and Canada and Mexico (25% each). He’s suggested that some of the tariffs can be avoided for Canada and Mexico over better border controls on drugs and illegal immigrants, but whether this is true is unknown. Political commentators like David Frum have pointed out that Trump’s views on trade have been consistent since his first considered run for the presidency in 1987, that he is hostile to trade and sees it as a zero-sum game.

In 2025 world leaders and policy shapers believe Trump should be taken both seriously and literally. While the current political situation in Canada has been turbulent, the view of the government and provinces is almost unanimous (Quebec and Alberta remain the perennial opponents to joining the band wagon). Doug Ford took the initiative to announce that Ontario could stop energy exports to the US in the event of a trade fight, a position seconded by BC’s premier David Eby.

But in the United States the threat of aggressive and expanding tariffs have also been taken literally, notably by Jerome Powell of the Federal Reserve. On December 18th, in a move that shook markets, Jerome Powell did announce a final rate cut for 2024, but stressed that future cuts were heavily dependent on inflation, which will likely rise if Trump enacts his regime of trading tariffs. Markets were quick to react, and though 2024 will be remembered as a pretty good year for investors, the speed and size of the market sell-off was newsworthy, being the largest since August.

The next morning and markets began on a relatively positive note, continuing a trend of brief panics followed by long yawns as markets simply resume their upward momentum. Little seems to have dissuaded the bull market since 2022 and with the US economy still showing itself to be very strong there’s every chance that the brief panic on December 18th was just that, a moment of panic at the end of 2024. But Trump, like the rest of us, doesn’t live in longer and slower news cycles. Instead market panics live on in social media, and run the risk of coalescing into counter narratives that Trump might hurt the economy more than help it (its notable that the economy has been very strong under Biden, but that didn’t change the perception that Trump had been the better economic steward).

In 2018 Jerome Powell began raising rates to blunt the sharper edges of a hot economy and return interest rates to somewhere near a historic norm. Since 2008 rates had remained at emergency low levels, and there was a genuine concern that markets were becoming addicted to cheap cash. In October of that year Jerome Powell made clear that rate hikes would continue until the Fed felt they’d reached a neutral rate, news not well received by the stock market. From October to the end of the year the S&P 500 lost 18% by December 24th, before rebounding slightly by the New Year. Markets had posted decent returns to the end of September, but wiped out those gains and finished the year -6.24% . During the last months of the year Trump made repeated efforts to pressure Powell to halt or cut rates, often publicly over Twitter.

My opinion is that Trump likes the ambiguity surrounding his pronouncements. Whether he actually intends to implement all the tariffs he’s discussed, whether they are bargaining positions, or whether he can be talked out of them is a grey area that offers him a position of strength. Politicians may be particularly vulnerable to his vagaries since they often wish to protect the status quo while Trump feels free to be a disruptor. But that grey area only works as a negotiating tactic so long as people believe that deals can be reached. If nations come to believe that Trump is serious and literal about tariffs and don’t believe they can be avoided, you are only left with a trade war. Similarly if you are in charge of the Federal Reserve and believe that Trump will do what he says, then you have every reason to pursue positions that curb inflation.

Following Trump’s election Jerome Powell was asked whether he would resign as the Federal Reserve chair, and was clear in his response; he will not, he is not required to leave, and cannot be compelled to. Trump already has a difficult and publicly hostile history with Powell, and its easy to imagine that if Powell is taking Trump seriously, he will move into direct conflict with Trump because of his policies, not in spite of them. Similarly conflict may be around the corner on diplomatic issues for the exact same reason. If Mexico feels it can’t avoid a trade fight with the US, you can assume that Mexico might be less interested in working to curb migrants at the US border. In Canada the same might be true, negotiating with someone who has no intent to make a deal (or honor the one already made) is not likely to build support for concessions.

Today Trump will take office following his inauguration, and he’s expected to sign a number of executive orders kicking off his next term. He has posed as a disruptor, and has nominated a number of other unusual thinkers and people opposed to the status quo to make up his cabinet. Whether they all take those roles and can do what they say they plan too is yet to be seen, but on December 18th we may have gotten some insight into what that future might look like, a future where Donald Trump is taken at his word, both seriously and literally.

Aligned Capital Partners Inc. (“ACPI”) is a full-service investment dealer and a member of the Canadian Investor Protection Fund (“CIPF”) and the Canadian Investment Regulatory Organization (“CIRO”). Investment services are provided through Walker Welath Management, an approved trade name of ACPI. Only investment-related products and services are offered through ACPI/Walker Wealth Management and covered by the CIPF. Financial planning services are provided through Walker Wealth Management. Walker Wealth Management is an independent company seperate and distinct from ACPI/Walker Wealth Management.

April was a turbulent month for markets. Having begun 2024 with an abundance of enthusiasm about the prospect of (very near) interest rate cuts from central banks, an improving economy both domestically and abroad, and resilient employment, 2024 promised the fulfillment of a long-held dream; for the central banks of Canada and the United States to tackle inflation without causing a recession.

Though recessions seem to not be lurking in the immediate vicinity, the best-case scenario for the year is now fully off the table. Several months of higher-than-expected inflation numbers have caused markets to reconsider their earlier optimism and contemplate some of the more pessimistic predictions for economies.

In turn, US markets shed several percentage points through the first two weeks of April, not wiping out the year’s gains but reducing them by about half. Bond markets, having placed bets on rate cuts and longer duration bonds have retreated as well, wiping out gains for the year and forcing bond traders to retrench into safer, shorter duration positions.

Markets have steadied since then, and have been encouraged by Jerome Powell’s statements that the Fed still intends to cut rates, but the earlier optimism about many cuts totalling more than 1% for the year seem unlikely, and even now we will need more data in the coming months to trigger the first cut that had been anticipated for the early year.

Why is this, and why have markets been so easily convinced that rates were bound to fall so quickly?

There’s no obvious single answer. Like many issues surrounding complicated problems a multitude of events, including human bias and the best of intentions have formed the foundations for a great deal of misunderstanding. For the Fed’s part, it has remained committed that data will drive all interest rate decisions, a sensible argument but one that has tied their hands. Investors and analysts have shown a natural bias of optimism, and have assumed that with the bulk of inflation easily defeated through 2022 and 2023 that the final pieces would fall easily into place. This optimism has not learned from the recent past, as 2023 began in much a similar way, with anticipation of rate cuts happening in the second and third quarter of the year only to have rates start increasing in May.

But after these more human problems, what remains are a series of headwinds that will likely be with us for the foreseeable future. While prices of many commodities have fallen from their peaks, and “supply chain constraints” are no longer choking the global trade network, the world is fundamentally different than its was before 2020. China’s relationship with the West is now more openly antagonistic, and a combination of “reshoring” or “friend shoring” is ensuring that costs will be higher than they were in the past. Food prices have continued to rise, with sometimes opaque reasons. In some instances there are clear justifications for higher costs, like bird flu affecting American egg prices or higher gas charges pushing up the cost of shipping. But other times it seems that prices have risen because grocery stores simply can. Finally, commodity prices, while lower than they were in 2021/2022, remain above pre-covid levels. This applies especially to the price of energy, which seems set to stay elevated for the near term.

Performance of the 1 year WTI contract – Source: Bloomberg

Underlying this remains some larger issues about inflation’s presence in our lives before 2020. As I’ve previously written, many parts of our society were experiencing inflation long before CPI began to worry economists and other experts. Prices of physical goods had been falling for decades, but price of homes, child care, education, and food had all been climbing over that same period. The price of housing might be better if governments took a more active role in getting the cost of development down, but permits and other government fees now account for anywhere between 20% (CMHC estimates) to 60% when all taxes, red tape, permit costs and development charges are accounted for, a lucrative source of funds for municipal budgets.

Additionally, since 2008 interest rates had been at “emergency levels”, the lowest borrowing costs of any time in history. Those near zero rates, which were intended to help remove slack from the economy and encourage large capital expenditure instead stimulated enormous share buybacks among major corporations. Instead of new jobs and a hotter economy we got increasing share prices and more corporate debt.

Problems that take a long time to form do not get fixed quickly. Repeatedly markets have shown an impatience for corrections and are quick to assume that pauses in inflation must mean that the trend of higher prices has both been beaten and that interest rates can fall back to previous emergency levels. Even if interest rates are at sufficient levels to regain control over the direction of inflation, it still doesn’t mean that rates can fall quickly, and the longer rates stay elevated above the emergency levels of the past, the deeper and more costly current interest rates become to the economy.

In Canada low interest rates helped stimulate an enormous increase in property values through the 2010s and into the pandemic. Higher interest rates threaten those gains and as we go through 2024, almost 60% of mortgages will have renewed into more expensive loans since rates began climbing. Even if interest rates begin to fall, homeowners can expect that the cost of borrowing will be much higher than they’ve been for many years. Between the desire of home owners to keep house values high, municipalities to keep their tax bases stable, and banks to ensure that the value of properties they’ve underwritten don’t move too much, the pressure to get inflation down runs squarely into our own self interest.

The urgency and desire for lower interest rates are real, but so are the headwinds that keeps inflation pressure high.

Walker Wealth Management is a trade name of Aligned Capital Partners Inc. (ACPI)* – if applicable ACPI is regulated by the Investment Industry Regulatory Organization of Canada (http://www.iiroc.ca) and a Member of the Canadian Investor Protection Fund (http://www.cipf.ca). (Advisor Name) is registered to advise in (securities and/or mutual funds) to clients residing in (List Provinces).

This publication is for informational purposes only and shall not be construed to constitute any form of investment advice. The views expressed are those of the author and may not necessarily be those of ACPI. Opinions expressed are as of the date of this publication and are subject to change without notice and information has been compiled from sources believed to be reliable. This publication has been prepared for general circulation and without regard to the individual financial circumstances and objectives of persons who receive it. You should not act or rely on the information without seeking the advice of the appropriate professional.

Investment products are provided by ACPI and include, but are not limited to, mutual funds, stocks, and

bonds. Non-securities related business includes, without limitation, fee-based financial planning services; estate and tax planning; tax return preparation services; advising in or selling any type of insurance product; any type of mortgage service. Accordingly, ACPI is not providing and does not supervise any of the above noted activities and you should not rely on ACPI for any review of any non-securities services provided by Adrian Walker.

Any investment products and services referred to herein are only available to investors in certain jurisdictions where they may be legally offered and to certain investors who are qualified according to the laws of the applicable jurisdiction. The information contained does not constitute an offer or solicitation to buy or sell any product or service.

Since late February the bulk of global attention has been focused on the Russian invasion of Ukraine. The invasion remains ongoing, and will likely last for months, potentially even years, and represents the most dangerous geopolitical situation we are likely to face until China tries to enforce control over the South China Seas or invades Taiwan.

But while our attention has been narrowly focused, interest is growing about how the world’s second largest economy is choosing to mange the late stages of the pandemic, a series of choices that have ramifications for much of the world.

China has had mixed luck with Covid. By the end of 2020 it looked as though China might be the only winner economically from the pandemic, but 2021 turned out to be a year for the West. First, Western vaccines, particularly the mRNA vaccines were highly effective, while the Chinese vaccine produced domestically had only a 50% success rate. The Chinese government also was hyper critical of the more effective Moderna and Pfizer vaccines, essentially precluding them from Chinese use. This has left the country in a difficult spot. Chinese mandated lockdowns have been brutal but effective, leading to uneven vaccine use. The low infection rates that the “Covid Zero” policy has delivered has also robbed the country of natural immunity. Today China, already struggling economically, is still locking down whole cities in the hopes of containing outbreaks.

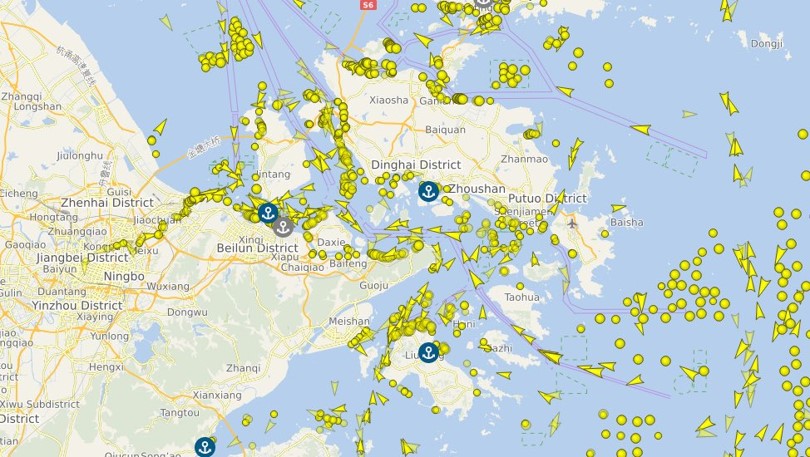

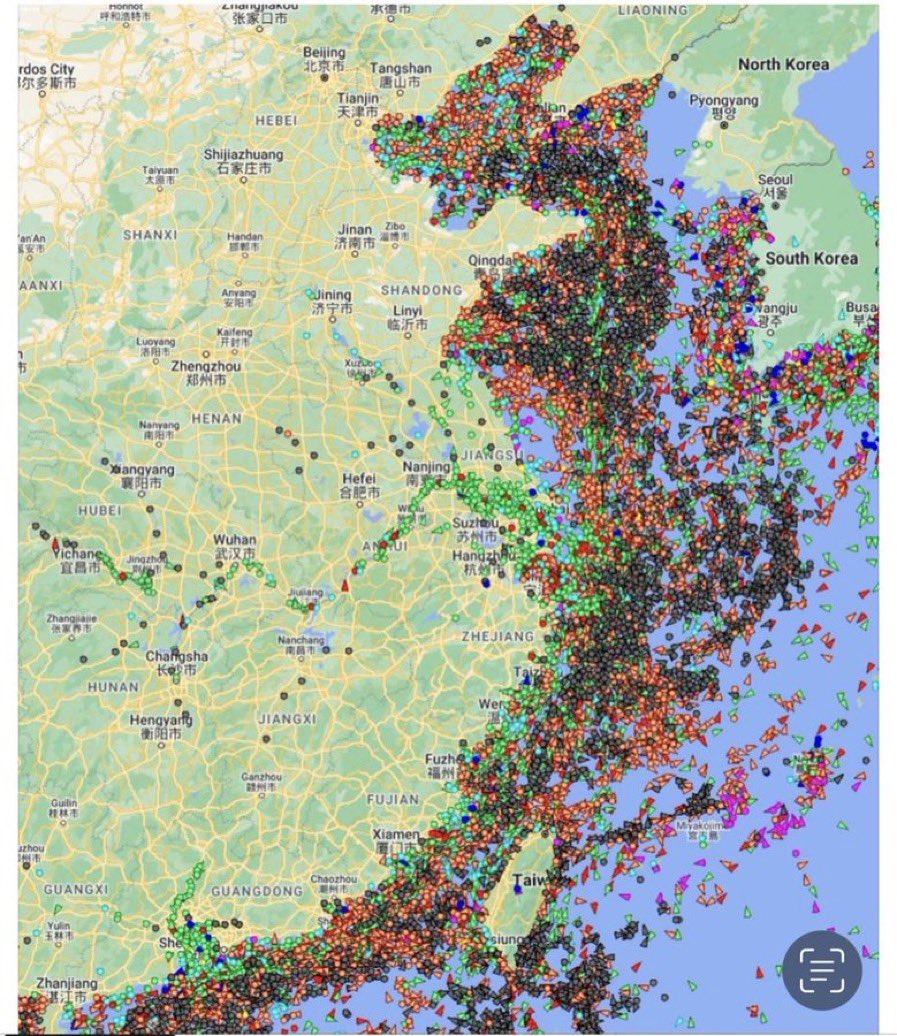

Chinese lockdowns are also worsening global inflation. The supply chain disruptions caused by the most recent lockdowns in Shanghai are dramatic to say the least. In the above picture each yellow dot represents one cargo ship waiting to be docked and unloaded. Supply chains were already deeply stressed when Shanghai went into lockdown last month, and the global impact of further supply disruptions is something we’re very likely to notice.

This image came from early May

Lastly, some months ago (October 2020) I had detailed how China’s foreign policy, which was heavy handed and often petulant, was angering nations all across the globe. China may not view the world the way its geopolitical rivals do, but its inability to grasp at least what might be considered fair or just by other nations is damaging its own ability to wield soft power, an essential part of being a global hegemon. China’s decision to back Russia in its invasion of Ukraine likely reflected China’s near-term goals of retaking Taiwan and its general contempt for the current world order. However, the global resistance to the Russian invasion, the support shown Ukraine and the barrage of negative publicity (as well as realizing that an untested military in countries with lots of corruption may not be able to score quick military victories) must serve as a wake-up call to China’s ruling class. As of 2022 China seems to have squandered much of its international good will and is unlikely to find many willing allies for its global ambitions.

China seems to be suffering on all fronts. 2021 was a bad year for China’s economy, cumulating in the public meltdown of one of its biggest developers in November. But everything, from its politics to its public health policies are working against it. The world’s second largest economy, one that is the largest trading partner to 130 countries, can’t seem get out of its own way, and as it falters it can’t help but impact us.

Walker Wealth Management is a trade name of Aligned Capital Partners Inc. (ACPI)*

ACPI is regulated by the Investment Industry Regulatory Organization of Canada (www.iiroc.ca) and a Member of the Canadian Investor Protection Fund (www.cipf.ca). (Advisor Name) is registered to advise in (securities and/or mutual funds) to clients residing in (List Provinces).

This publication is for informational purposes only and shall not be construed to constitute any form of investment advice. The views expressed are those of the author and may not necessarily be those of ACPI. Opinions expressed are as of the date of this publication and are subject to change without notice and information has been compiled from sources believed to be reliable. This publication has been prepared for general circulation and without regard to the individual financial circumstances and objectives of persons who receive it. You should not act or rely on the information without seeking the advice of the appropriate professional.

Investment products are provided by ACPI and include, but are not limited to, mutual funds, stocks, and bonds. Non-securities related business includes, without limitation, fee-based financial planning services; estate and tax planning; tax return preparation services; advising in or selling any type of insurance product; any type of mortgage service. Accordingly, ACPI is not providing and does not supervise any of the above noted activities and you should not rely on ACPI for any review of any non-securities services provided by Adrian Walker.

Any investment products and services referred to herein are only available to investors in certain jurisdictions where they may be legally offered and to certain investors who are qualified according to the laws of the applicable jurisdiction. The information contained does not constitute an offer or solicitation to buy or sell any product or service. 16 Past performance is not indicative of future performance, future returns are not guaranteed, and a loss of principal may occur. Content may not be reproduced or copied by any means without the prior consent of the author and ACPI.

Markets have been falling through the year, and despite some encouraging rallies the trend so far has been decidedly negative. The NASDAQ Composite, one of the three big indexes heavily tilted towards technology companies had a -23.86% YTD return as of Monday, May 16th, a minor recovery after it had reached a low of -27% on Thursday of the previous week. The Dow Jones and the S&P 500 have YTD returns of -10.31% and -14.82% respectively. The question for investors is “what to do?” in such markets, especially after some of the best years despite the pandemic.

A closer inspection of the markets however shows that while there have been some steep sell offs reflected in the broad market, the real market declines have been far more concentrated. And while there are many different market headwinds to choose from when it comes to reasons for the recent selling action; inflation, interest rates, geopolitical strife, COVID-19, maybe even Elon Musk, the sector that has been sending markets lower has been the tech sector.

Over the past couple of years the companies posting the biggest gains in the markets have been tech companies. Apple stock (AAPL) was up 88.97% in 2019, 82.31% in 2020, 34.65% in 2021, and is down -11.6% so far in 2022. Amazon (AMZN) was up 76.26% in 2020, and has fallen -30.18% this year. Facebook, now META Platforms (FB) gained 56.57% in 2019, 33.09% in 2020, 23.13% in 2021 and has lost -38.08% in 2022. Netflix was up 67.11% in 2020, and a further 11.41% in 2021 but is down -68.74% this year. Tesla, which had an astounding 743.4% gain in 2020 and another 49.76% return in 2021 is so far down -17.36% in 2022, how long can it resist gravity? (All prices and YTD performance were collected from ycharts.com on May 6th, 2022).

I predict that we may never fully understand how the pandemic changed thinking and why stock prices climbed so much, but the reality was that many tech companies benefited from people staying home, going online and the changing priorities that coincided with not having to be in offices and commuting. Tech companies that became huge like Shopify (SHOP), which allowed traditional retailers to become online retailers, benefitted immeasurably from the lockdowns. But it too has seen its stock decline this year by -69.59%, pushing the price back to where it was in December 2019.

Markets are facing other risks too. Inflation, which seems to be running at about 8%, can threaten economies as people buy fewer items due to cost increases. Interest rate hikes, which are meant to ultimately curb inflation by restricting monetary supply and reduce lending/economic activity have hit bond markets particularly hard. Higher interest rates mean higher borrowing costs, and its here we might hypothesize about some of the unintended consequences of the incredibly accommodative monetary policy that the pandemic introduced. That might be that investors were able to borrow to invest, and the threat of both rising interest rates and stumbling returns will only hasten the exit of money from the market by some investors. Higher borrowing costs will also have another impact on markets, as a sizeable amount of stock market returns over the past decade have come from share buy backs, funded in part by low-cost borrowing.

Having said all that, economies are still looking very strong in the present. Earnings have remained high, jobless claims continue to fall, and while we’ve seen a spike in costs the ability to address those inflationary pressures may not be something that can be easily done through monetary restricting.

There are many different sources of inflation, but two significant issues are not connected to “cheap money”. Instead we have issues that are primarily structural and represent the failure of political foresight. The first among these has to do with oil. Since the price of oil fell in 2014, infrastructure development has stalled, heavily indebted producers have retreated, and now Russia has been closed off from much of the global market. This confluence of events has unfortunately arrived as economies are reopening, global use nears pre-pandemic levels, and global refined supply is at historic lows. There is no simple solution for this, as the only remedy is time (and development). In theory, Canadian and US oil could make up much of the global need, but for a multitude of reasons neither country is in a position to rapidly increase production.

Similarly, supply chain disruption and the heavy reliance on offshore manufacturing have meant that there is no simple solution to production problems occurring in other nations. China is the key issue here, with an enormous grip on much of global supply on many items and their current insistence on a “Covid Zero Policy” China is effectively shut to global business. This means ships can’t get into port, and with-it products cannot make it to market.

Higher borrowing costs seem unlikely to handle this problem. High gas prices and lack of supply may be inflationary, but high borrowing costs can’t target those issues. Instead, higher interest rates and the threat of more in the future are hitting the parts of the market that have been pushed higher by cheap credit. The stock market and the housing market.

If markets seem to be moving independently of economies, its possible that won’t stay that way for long. As previously mentioned, higher energy prices are not controllable by higher lending rates. But higher energy prices can introduce demand destruction, a fancy way of saying that economies shrink because prices get out of control. Oil is still in high use and its needs go far beyond powering cars. In fact internal combustion engines only account for 26% of global oil need, meaning those higher prices for crude, if they get too high, can have wide inflationary impacts to the entire economy.

Higher lending rates may also lead to a substantial economic reset, especially for Canadians who have much of their net worth tied up in their homes. With almost 50% of new mortgages in Canada variable rate mortgages, home prices having skyrocketed in the past few years and with most Canadian debt connected to homes, the risk to home owners is very real. Can the Bank of Canada tame inflation, orchestrate a soft landing for the housing market and keep the economy chugging along? Such a question invites highwire act comparisons.

So what’s happening with markets? Perhaps we are simply correcting a narrow subset of the market that got too hot through 2020-2021. Perhaps we are seeing the dangers of printing too much money. Perhaps we are seeing the realities of people buying too many index ETFs. Perhaps we are witnessing people being too fearful about the future. Perhaps we are too fearful of inflation or interest rates. Perhaps we are on the brink of a recession.

Perhaps, perhaps, perhaps.

But let me offer a slightly different take. Investing is frequently about connecting your needs as an investor with the realities of the world. As Warren Buffet famously said, in the short term the stock market is a voting machine, in the long term a weighing machine. If you can afford risk, you can be risky, and with that comes the potential for significant market swings. If you can not afford risk, then your portfolio should reflect that need. If you cannot stomach bad days, potentially weeks or even months of bad news, then you need to find a way to keep your investment goals aligned with your risk tolerance.

When I started this essay we had just completed one of the worst weeks of the year, which bled into the second week of May. As I finish this piece markets are in the process of rallying for a third day, posting modest gains against the backdrop of significant losses. It would be nice if I could end this with some confidence that we’ve turned a corner, that markets had bottomed and that the pessimism that has led to so much selling is evaporating as people come to recognize that stocks have been oversold. Yet such prognosticating is the exact wrong tack to take in these markets. Instead, this is a good time to review portfolios, ensuring that you are comfortable with your risk, that your financial goals remain in sight and that the portfolio remains positioned both for bad markets, and for good ones too.

If you have any concerns about how your portfolio is positioned and need to review, please don’t hesitate to contact us today.

Walker Wealth Management is a trade name of Aligned Capital Partners Inc. (ACPI)*

ACPI is regulated by the Investment Industry Regulatory Organization of Canada (www.iiroc.ca) and a Member of the Canadian Investor Protection Fund (www.cipf.ca). (Advisor Name) is registered to advise in (securities and/or mutual funds) to clients residing in (List Provinces).

This publication is for informational purposes only and shall not be construed to constitute any form of investment advice. The views expressed are those of the author and may not necessarily be those of ACPI. Opinions expressed are as of the date of this publication and are subject to change without notice and information has been compiled from sources believed to be reliable. This publication has been prepared for general circulation and without regard to the individual financial circumstances and objectives of persons who receive it. You should not act or rely on the information without seeking the advice of the appropriate professional.

Investment products are provided by ACPI and include, but are not limited to, mutual funds, stocks, and bonds. Non-securities related business includes, without limitation, fee-based financial planning services; estate and tax planning; tax return preparation services; advising in or selling any type of insurance product; any type of mortgage service. Accordingly, ACPI is not providing and does not supervise any of the above noted activities and you should not rely on ACPI for any review of any non-securities services provided by Adrian Walker.

Any investment products and services referred to herein are only available to investors in certain jurisdictions where they may be legally offered and to certain investors who are qualified according to the laws of the applicable jurisdiction. The information contained does not constitute an offer or solicitation to buy or sell any product or service. 16 Past performance is not indicative of future performance, future returns are not guaranteed, and a loss of principal may occur. Content may not be reproduced or copied by any means without the prior consent of the author and ACPI.

Its traditional that the end of a year should stimulate some reflection on the past and the future, and so in the spirit of tradition I thought I’d take some time to look over some of the stranger and more surprising aspects of 2021.

China

While 2021 brought the pandemic *closer* to an end through the distribution of vaccines, markets underwent some fairly dramatic reversals over the course of the year. For instance China looked to be the principal economy in January. Following its own strict enforcement of Covid restrictions and solid economic performance, China seemed to be an earlier winner by the beginning of 2021, and set to enjoy robust growth through the year.

By March the tide was shifting however. China’s leader, Xi Jinping, proved to be every bit committed to his past comments about protecting and strengthening the CCP over free market concerns. Several billionaires, notably Jack Ma the founder of Alibaba, disappeared for long periods before reemerging only to publicly announce that they would be stepping down from their roles.

The finer points of China’s housing market are too nuanced to get into here, but it’s enough to know that the property bubble in China is large, built on sizeable debt and could take some time to deflate (if it does) and no one is sure what the fallout might be. Combined with China’s ongoing policy of “Covid Zero” – an attempt to eradicate the virus as opposed to learning to live with and manage it, we head into 2022 with China now a major outlier in the Asian region.

Inflation

Inflation was probably the other most discussed and worrying trend of 2021. Initially inflation sceptics seemed to win the argument, as central banks rebuffed worries over rising prices and described inflation as transitory. That argument seemed to wane as we entered late Q3 and prices were indeed a great deal higher and didn’t seem to be that “transitory” anymore. Inflation hawks took a victory lap while news sites began to fill up with worrying stories about rising prices on household goods.

The inflation story remains probably the worst understood. Inflation in Canada, as in other Western nations has been going on for sometime, and its effects have been under reported due to the unique nature of the CPI. But some of the concern has also been overwrought. Much of the immediate inflation is tied to supply chains, the result of “Just-in-time” infrastructure that has left little fat for manufacturers in exchange for lower production costs. Bottlenecks in the system will not last forever and as those supply chains normalize that pressure will recede.

The other big pressure for inflation is in energy costs, but that too is likely to recede. Oil production isn’t constrained and prices, while higher than they were at the beginning of the pandemic are lower than they were in 2019. In short, many of the worries with inflation will not be indefinite, while the issues most worrying about inflation, specifically what it costs to go to the grocery store, were important but underreported issues before the pandemic. Whether they prove newsworthy into the future is yet to be seen.

*Update – at the time of writing this we were still waiting on more inflation news, and as of this morning the official inflation rate for the US over the past year was 7%. Much of this is still being chalked up to supply chains squeezed by consumer demand. An unanswered question which will have a big impact on the permanence of inflation is whether this spills into wages.

This political advertisement from the Conservatives ruffled many feathers in late November

Housing and Stocks – Two things that only go up!

If loose monetary policy didn’t make your groceries more expensive, does that mean that central bankers were right not to worry about inflation distorting the market? The answer is a categorical “No”. As we have all heard (endlessly and tediously) housing prices have skyrocketed across the country, particularly in big cities like Toronto and Vancouver, but also in other countries. The source of this rapid escalation in prices has undoubtedly been the historically low interest rates which has allowed people to borrow more and bid up prices.

In conjunction with housing, we’ve also seen a massive spike in stock prices, with even notable dips lasting only a few days to a couple of weeks. The explosion of new investors, low-cost trading apps, meme-stocks, crypto-currencies, and now NFTs has shown that when trapped at home for extended periods of time with the occasional stimulus cheque, many people once fearful of the market have become quasi “professional” day traders.

Suspicious Investment Practices In addition to a stock market that seems bulletproof, houses so expensive entire generations worry they’ve been permanently priced out of the market, the rapid and explosive growth of more dubious financial vehicles has been a real cause for concern and will likely prompt governments to begin intervening in these still unregulated markets.

Crypto currencies remain the standout in this space. Even as Bitcoin and Etherium continue to edge their way towards being mainstream, new crypto currencies trading at fractions of the price, have gotten attention. Some have turned out to be jokes of jokes that inadvertently blew up. Others have been straight-up scams. But all have found a dedicated group of investors willing to risk substantial sums of money in the hope of striking it rich.

NFTs, or non-fungible tokens have also crept up in this space, making use of the blockchain, but instead of something interchangeable (like a bitcoin for a bitcoin, i.e. fungible) these tokens are unique and have captured tens of thousands, sometimes hundreds of thousands of dollars for unique bits of digital art. Like cryptocurrencies, much of the value is the assumed future value and high demand for a scarce resource. However, history would show that this typically ends poorly, whether its housing, baseball cards or beanie babies.

Lastly, there has been a number of new investment vehicles, the most unusual of which is “fractional ownership”. The online broker Wealth Simple was the first to offer this in Canada and it has been targeted to younger investors. The opportunity is that if your preferred stock is too expensive, you can own fractions of it. So if you wanted to invest in Amazon or Tesla, two stocks that are trading at (roughly) $3330 and $1156 respectively at the time of writing, those stocks might be out of reach if you’re just getting started.

This is a marketing idea, not a smart idea. The danger of having all your assets tied up in one investment is uncontroversial and well understood. The premise behind mutual funds and exchange traded funds was to give people a well-diversified investment solution without the necessity of large financial position. The introduction of fractional ownership ties back to the market fragility I mentioned above, with younger investors needlessly concentrating their risk in favour of trying to capture historic returns.

The End

For most investors this year was largely a positive one, though markets went through many phases. But while the pandemic has remained the central news story, the low market volatility and decent returns has kept much of us either distracted or comfortable with the state of things. And yet I can’t help but wonder whether the risks are all the greater as a result. Many of these events, the large returns in an ever tightening group of stocks, the growth of investors chasing gains, the sudden appearance of new asset bubbles and the continued strain on the housing market and household goods add up to a worrying mix as we look ahead.

Or maybe not. Market pessimists, housing bears, and bitcoin doubters have garnered a lot of attention but have a bad track record (I should know!) Many of the most pressing issues feel as though they should come to a head soon, but history also teaches us that real problems; big problems that take years to sort out and lead to substantial changes are often much longer in the making than the patience of their critics. The test for investors is whether they can stand by their convictions and miss out on potential windfalls, or will they become converts right as the market gives way?

Next week, we’ll examine some of the potential trends of 2022.

For the past few weeks I’ve been struggling to capture what’s been happening in markets since late January. There has simply been so much that it is hard to succinctly cover it all in a single blog post.

So instead, toady I hope to touch on one thing that should stand out to us, the potential end of an investing strategy that is so standard it is reflected in almost every corner of the financial services world, from mutual fund companies to robo-advisors to banks.

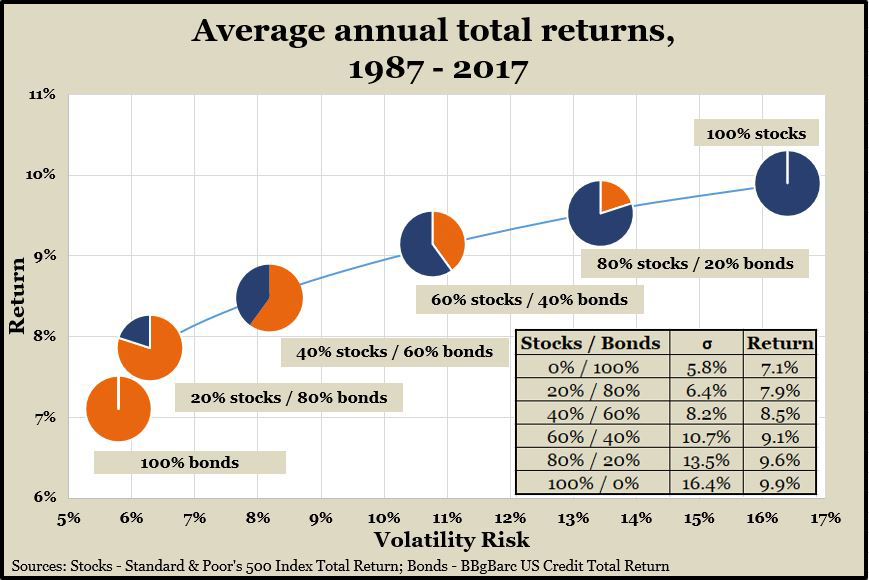

The 60/40 split, or balanced portfolio, is the general go to solution for steady returns. The principle is simple: 60% of a portfolio is weighted towards equities, that is stocks in companies, mutual funds or ETFs, and the remaining 40% goes towards fixed income; a collection of bonds or other “safe” investments that pay some income in the form of mutual funds or ETFs.

This is a wide space to play in. Within the stock or equity portion, a portfolio may have exposure to any number of companies, sectors, or geographies. Similarly, the fixed income component can have government debt, corporate bonds, T-bills, mortgage securities, either domestic or foreign, in short or longer durations. The individual positions may have short term impacts on performance, as some investments will outperform for limited stretches, but the general architecture of the portfolio should see relatively stable and consistent returns over time with an acceptable level of risk for the majority of investors.

This wasn’t just speculation. It had some math behind it, explained in the form of the “Efficient Frontier”, a curve that showed the relation of risk to return and aimed to help identify an optimum portfolio based on these two metrics. The goal was to maximize the amount of return for the risk undertaken. Its easy to get lost in the weeds here, but if you’re ever interested you can read up on Modern Portfolio Theory or Harry Markowitz. Put simply, the lesson the industry took was that a diversified portfolio of investments, with rough weightings of 40% in fixed income and 60% in equities would largely suit most people.

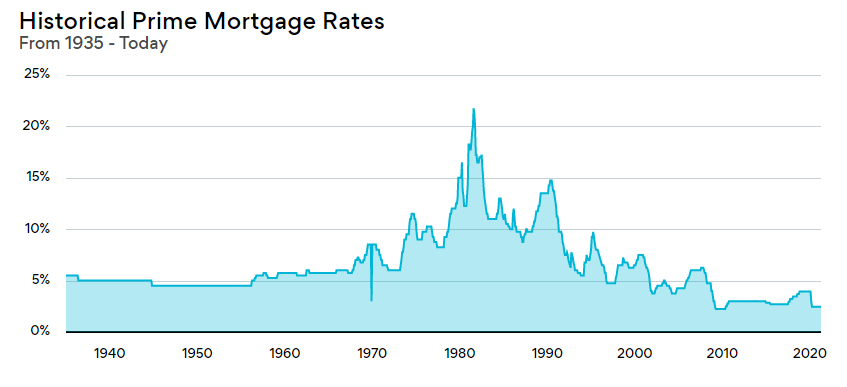

It’s worth asking why this is. And the answer has a lot to do with buying a house in the late 1970s and early 1980s.

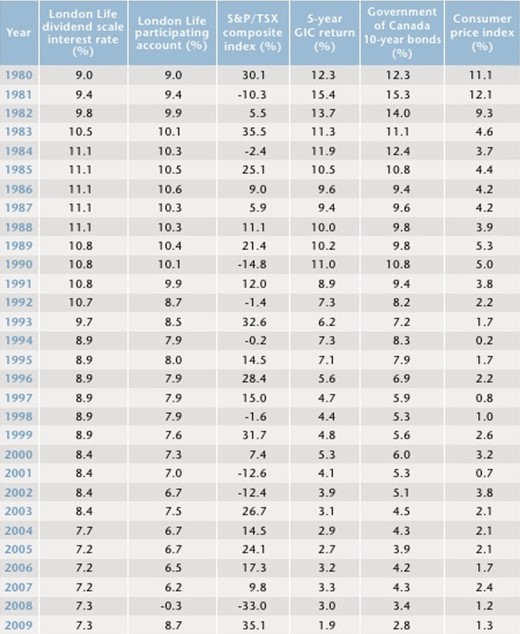

As anyone who remembers 8-tracks will tell you, buying a house in the early part of the 80s was expensive. 5-year fixed rates were 20%, or more. According to the website ratehub.ca, the prime lending rate in Canada peaked at around 21.75% in August of 1981. By comparison, my current 5-year mortgage is a whopping 1.8%. In 1981, you could buy a Government of Canada 10-year bond with a coupon rate of 15.3%, and a 5-year GIC with a rate of 15.4%. Today a 10-year government of Canada bond has a yield of 1.51% and the most generous GIC I can sell is 1.96% from Haventree Bank with a minimum deposit of $50,000.

Figure 1 From London Life – Looking Back at Historical Returns

Okay, so what’s the connection?

The issue here is not just that buying a house cost more when it came to lending in the 1980s, but that the cost of lending itself has been falling for the last 40 years. We tend to think of bonds as an investment you buy, when in reality they are a loan you are making that can be traded on an open market. So imagine you were building a bond portfolio in the early 1980s, and the average yield of that portfolio (the interest you will receive based on what you paid) is 15%. It’s very safe, made entirely of Canadian 10-year bonds. Now, three years pass and a new 10-year bond from the GoC has a rate of 12.3%, what’s the effect on your bond portfolio?

It’s good news! It’s worth more, because for the next 7 years your bonds will pay 3% more than any new bond issuance. By 1986 a 10-year bond was paying 6% less per year than your portfolio. For the last 40 years the cost of borrowing has continued to decline, and the result has been to make bonds issued in previous years more valuable. And so, while there may have been fluctuations in returns over short periods of time, by and large a portfolio of bonds returned not just income, but also capital gains as older bonds were worth more with each decline in the cost of lending.

Today the cost of lending is low. Very low. Central bank lending rates for Canada, the United States, and the ECB are 0.25%, 0.25% and 0% respectively. A 30-year government of Canada bond has a current yield of 1.948%. In other words, were you to buy that bond today, the most you would earn is 1.948% on whatever you paid for the next 30 years.

But remember, bonds are traded on an open market. This means that the value of a bond fluctuates with its demand, and with it the return the bond gives. So, if you think that 1.948% is not enough interest to warrant buying the bond and the broad market agrees with you, the price of the bond should fall enough to push up the yield (for reference, the yield is the interest paid by the bond, divided by its price) until it pays enough interest to warrant investing. And that is what has been happening this year. Government bonds in the United States have been dumped as investors expect stock markets to do well and bond yields are considered too low. And as the bond price falls, the yield the bond pays goes up in relation to the decline of the price, and with it sets a borrowing rate investors are more comfortable with.

What this means for portfolios is that the 40% allocated to bonds is now very vulnerable to both investor sentiment and future rate hikes by central banks. With borrowing rates already at rock bottom both of these risks seem likely, and it’s left the traditional “balanced portfolio” exposed when it comes to reducing risk through different asset classes.

You might assume that this is a new problem, but it isn’t. Risk has been growing and portfolios have been evolving in complexity to meet the needs of investors for the last few decades. Much of this has happened on the equity side of portfolios, with investors demanding, and ultimately gaining access to a much wider range of investable products since the 90s. The period where you could have a portfolio made up of just Canadian dividend paying stocks ended long ago, and in its place, portfolios now hold a variety of investment products with access to large cap, small cap, US, North American, global, international, Emerging Markets, Frontier Markets, sector specific investing, thematic investing, commodities, dividends, value, growth, and growth at a reasonable price. Bonds have undergone a similar transformation, with investors moving from government bonds, to corporate bonds, to junk bonds (bonds with lower quality ratings and potentially higher default rates) both domestically and globally.

Today, to achieve a return of about 6.5%, the average investor is taking on risk at a much higher rate than they would 20 years ago. In 2000 a 6.5% return could be achieved with a portfolio of exclusively bonds. 20 years later a 6.5% return would require a much larger range of positions, including US stocks (large and small cap), real estate, private equity and would have a relative level of risk of more than double (almost three times!) the 2000 level. The above changes to the bond market will only mean more risk and more volatility for investors.

I’m reluctant to ever declare something “dead” or “over”. That language betrays too much confidence about tomorrow, but financial history is much longer than most people appreciate and is filled with disruptions and the ending of economic certainties followed by the arrival of new paradigms. Whether it is the bankrupting of the Medicis, or the popping of a tulip bubble, economic realities can change. The “balanced portfolio” with its 60/40 mix, has been a cornerstone of simplified investing, a “go-to” solution that has made mass investing using discount platforms affordable and easy.

Figure 3 From Wealth Simple’s web page, simply choose your risk comfort and get a portfolio with more or less bonds. No need to think, no need to worry.

In an ideal world we might wish that investing was more “set it and forget it” than not, but long-term data and averages obscure the reality for many people. In the last ten years we’ve seen two serious “once in a lifetime” events that have shaken markets and governments. Investors, no matter what their stripe, whether they prefer robo-advisors, bank products or a personal financial advisor like myself, should be cautious that the rules to successful portfolio building are immutable.

Last week may go down as one of the weirdest weeks in investing history.

By now you have been made aware of the company Game Stop (GME:N). You’ve undoubtably been forced to look up what a short position and a “short squeeze” are and have collided head first into the meme fuelled online community of Wall Street Bets, the subreddit that lives for dangerous investments and may go down in history for the first market based populist uprising.

My first twig that something was going on came the week before last. I had investments in Blackberry (BB:TSX), a company that I had felt was undervalued and believed had made a successful transition into cyber security, a market sector I believe poised for long term growth. The ride had had not been fun. And then, all of a sudden the stock began going up. At first it seemed to be in response to a series of positive news stories; a settled IP legal case with Facebook, a new deal with Amazon for cloud services, and the sale of some 90 patents to Huawei. And then the stock took off. Within days a stock that had been languishing around $8 – $9 had suddenly doubled and was now looking to triple.

I was elated, until I read about Wall Street Bets (WSB), Game Stop, a hedge fund and how a number of stocks, including Blackberry, were being driven higher in an attempt to hurt a hedge fund. The story was fascinating but also terrifying. On Tuesday morning I exited Blackberry and began trying to understand what was going on.

The internet is a weird place, and far from creating a new universal society, it has instead hastened the growth of more insular and specialized communities. From the outside these groups can feel pretty alien. They have their own language, jokes and hierarchies and the subreddit Wall Street Bets is no different. But once you had pushed past the memes and lingo, it became clear the WSB, which is filled with amateur traders, had caught on to a risky move by a hedge fund called Melvin Capital. Melvin Capital had taken out large short positions on Game Stop, a legacy business that sold physical game cartridges in malls that was obviously struggling. The price of the stock had recently gone up following a new board member and announced plans for further restructuring. The traders at Melvin Capital believed the price of the stock over valued and had opted to short the stock (a method of betting on a future price decline by “borrowing” stock, selling it and buying it back within a set period of time). What the investors over at WSB understood was that the size of the short was too big, and that if they were to buy up all the available stock and hold it they could create a “short squeeze” in which the price of the stock climbs and the available supply of the stock falls, forcing potentially unlimited losses on those holding the shorts.

From here everything becomes extremely weird. It turned out the Wall Street Bets crowd wasn’t interested in making money as much as they were interested in crippling Melvin Capital. The trading platform that facilitated all of this, Robinhood, which prided itself on “democratizing trading” and offered no fees for doing trades, suddenly seemed to fold under the most minor of pressure to the request of another hedge fund to restrict retail trading on Game Stop, allowing only selling and no buying on Thursday. Suddenly members of Congress from across the political spectrum were tweeting and complaining about the restriction of trading regarding Game Stop and threatening to hold hearings into Robinhood’s practices.

On Friday limited purchases of Game Stop reopened, and much to the surprise of many, the commitment to “hold” did hold. While the price of Game Stop stock had fallen Thursday during the period only selling was allowed, the price decline reflected minimal volumes. On Friday morning the stock opened again above $300, and despite considerable volatility closed the week at $325 a share.

You’d be forgiven if you’re having a hard time following all the facets of this story, but from my vantage I’d like to share the 4 major issues this convoluted chain of events has created.

1.Populism and Democracy – Twitter and Reddit have been alive with excitement over screwing with a hedge fund, and its apparent that those engaging in the initial rally for GME are committed to undermining Melvin Capital, but the sharp response from Wall Street institutions that this represented some kind of illegitimate assault on the markets highlights the lack of interest in a “democratized” market. Like a lot of internet buzz about “making things more accessible” or “democratic”, when put into practice established institutions don’t seem to like the rabble actually having all that much power. Whether it’s a crowd sourced populist group of traders playing the other side of an over leveraged short position, or simply an online vote that wishes to name a scientific vessel “Boaty McBoatface”, efforts to open, engage and democratize previously closed off institutions seem to fail when it turns out the masses don’t share the goals or reverence of those institutions.

2. Hedge funds often describe themselves in terms of significant reverence and are self-styled “Titans of Wall Street”, but as a group hedge fund performance frequently falls flat. What hedge funds have been good at is risking other people’s money. The brashness and over confidence displayed by hedge fund traders is precisely how you end up with a short position worth 130% of the available stock of a company and squandering $5 billion in a week. Some may find “shorting” a controversial practice, but in reality it is a common and well understood strategy. But in the hands of hedge funds it can become predatory as efforts are made to sometimes game the system and force stock prices down unnecessarily.

3. The Robinhood trading app, which has become all the rage with DIY investors seemed to have its brand implode in the week, and it perhaps revealed far more about this business than anyone had wanted. Like Google or Facebook, where the service is “free”, people using the Robinhood trading platform were the product. Robinhood, legally but controversially, makes its money by “payment for order flow”, or by directing the orders to different parties for trade execution. This all gets pretty complex, but at its core those using the Robinhood app may have been paying fractionally too much for their trades, but when in the context of billions of trades it adds up to a substantial amount of money. The benefit of buying overflow is that high frequency trading algorithms can potentially front run those trades, which was the subject of the controversial Flash Boys book by Michael Lewis. Perhaps more nefarious was who was Robinhood’s primary purchaser of order flow; Citadel Execution Services, which is owned by Citadel LLC, which just bailed out Melvin Capital.

4.Much of this will end up bypassing the bulk of the population. The story is too weird, to convoluted and too specialized. It involves a cynical and anarchistic online community whose rallying cry is “WE CAN REMAIN RETARDED LONGER THAN THEY CAN STAY SOLVENT”, something that many will find repellent and will keep people from looking closer. What might make people pay attention is the money.

The apocryphal story of the famous investor receiving investment advice from the shoe shine boy right before the great crash has some modern parallels. Prices for stocks, some at all time highs, keep going up despite worrying fundamentals. Companies like Tesla, which have devout adherents, have bid up that stock so that the total company is worth more than all the other major car companies combined! This reeks of the beginnings of a mania, one that can only be made worse by a prolonged lockdown, low interest rates, and the use of social media to hype up a stock. The allure of easy money, embodied by the events surrounding Game Stop will only attract more investors that believe that they too can beat the market.

At the end of last week the number one app in Canada was the Wealthsimple Trade App, a similar low cost trading platform to Robinhood, while the Robinhood App itself remains highly popular south of the border.

The wind has been let out of the sails somewhat this week. Game Stop closed under $100 on Tuesday, and early hype that silver was going to be the next big WSB play seem to have fizzled also. Markets seem to have responded to this cooling of temperatures by resuming their positive direction, but the spectre of market mania looms over returns. Where we go next, I don’t know. But I do know that sensible investors should be watching this with concern. Whatever the merits of hunting hedge funds through crowd sourced market initiatives, the larger story remains one of deep concern, involving all the worst aspects of investing.

“Information in this commentary is for informational purposes only and not meant to be personalized investment advice. The content has been prepared by Adrian Walker from sources believed to be accurate. The opinions expressed are of the author and do not necessarily represent those of ACPI”.