Greece has proven to be a needless problem for much of Europe, but one that has highlighted many of Europe’s fundamental weaknesses. Greece may have navigated itself into this mess, but it isn’t unreasonable to expect that solutions to Greece’s problems eventually look like, well, solutions. In short Greece needs one of three things. Either to be treated like a fundamentally poor state requiring transfer payments from the rest of Europe (unacceptable to Germany), relief in the form of debt forgiveness (unacceptable to the ECB, Germany and the IMF), or to exit the euro and revert to the drachma (unacceptable to Greece).

Notably none of these options has been pursued. Instead the status quo has been maintained to nobody’s satisfaction. The Greek government is outraged that the deal is effectively worse than the one they rejected. Most of Europe is upset at how poorly the negotiations were handled by both sides, and the brash and ultimately useless Alex Tsipras has ultimately failed in getting any of the concessions he thought he might secure through his brinkmanship.

There is some light at the end of the tunnel however. There is now some hope for debt forgiveness in the future. And if Greece hits its austerity and reform targets there may be continued relief on both interest rates for existing debt and the opportunity to push the payment dates farther out into the future. While this may signal some progress, the problems that underlie the Greek crisis still exist across Europe.

Those problems have everything to do with Europe’s loose federation and shared currency. I recommend the above video to quickly explain the inherent problems within the euro. But for now it looks as though the only winner in all this is the integrated EU zone. Once again it seems that the decisions made were about protecting the European experiment, even as that experiment makes matters worse for Europeans. That raises questions again about what the point of the EU is if not to improve people’s lives.

This week three big issues are defining the financial landscape

Greece Isn’t Done Yet!

Despite a no vote in Greece over the weekend, the EU still believes it is within the collected interest within the Eurozone to stop Greece from imploding. Strong resistence seems to be coming from Greece on this issue as the Greek Prime Minister, Alexis Tsipras, swanned into Brussels with Cheshire cat grin and nothing in hand to negotiate with. Greece has five days to work out a plan with its creditors before being declared in default. While the Greek situation seems to be playing out at a glacial pace, the fact is that these tactics can only go on for so long, and eventually (presumably by the end of the week) a point of no return will be passed and negotiations will be moot. The stakes are high as a Greek default, while not insurmountable by European leaders, risks creating problems in other member states. That contagion is at the heart of German reluctance to cut Greece any slack and it is the real concern that is adding volatility to the market. Markets would like to see a sensible conclusion to the Greek problem since it will reassure everyone that the larger plan for Europe is still in place. A chaotic Greek exit from the euro could simply make matters worse.

China: Start Panicking and Throw Things!

For years people have scratched their heads at the curious case of China. China’s economy is huge and somewhat a mystery. Like most big economies, the government makes predictions about the future of economic growth. Unlike most big economies those predictions are always right and never need any revision. In addition to China’s always correct economic growth numbers, China has embarked on massive infrastructure projects. So massive that they’ve built entire cities where no one lives. This combination of big spending and highly suspect numbers has made many people wonder whether there is a looming problem within China that has yet to rear its head.

That problem may have arrived this month. The Chinese stock market has lost close to 40% over the last month and the government has had to step in to try and stop the collapse. So far that hasn’t worked. Prices in China have surged over the last few years as many smaller investors have not just placed money in the market, but borrowed to do it as well. While there were rules to stop “leveraged market mania” within the Chinese market, like all rules they were both weakened over time and people have found ways around them (you can read more about that in this May report: Credit Suisse Report on Chinese Leverage).

China has a market bubble and it’s in the process of deflating. Just this spring 20 million people opened stock accounts, while whole towns have given up farming so that they can play the markets. The Chinese government isn’t oblivious to this problem, and has taken extreme action to try an prop up the market, but whether that will work has yet to be seen. Meanwhile concerns that the market is collapsing is driving many investors to sell, exacerbating the situation.

Canada in Recession? What’s a Recession?

Canada’s economic situation is…unclear. At least, that’s the best case scenario. The regular reports from the Bank of Canada, The Financial Systems Review, which details risks within the Canadian market and has regularly highlighted that the indebtedness of Canadians poses the single greatest risk to the economy. If the economy were to change in any way that made servicing those debts impossible the effect would be serious. Since the December report, the Bank of Canada had made an unexpected rate cut to help prop up the economy which was being affected by the falling price of oil. The June FSR (which you can read HERE) stated the same thing, but hoped that an improving American economy would also float Canada’s economic boat. But shortly after publishing several things went wrong. It was revealed that the Canadian economy had contracted four months in a row, with the last month coming as a complete surprise to the BoC. Today, news got worse that Canada has had a record trade deficit, and combined with other bad news gives weight to the likelihood that Canada is already in recession. While this will add pressure for a rate cut, the real message here is that the Canadian market is far more dangerous and volatile than many investors think. That’s something that Canadians reviewing their portfolios should be highly aware of as they consider their retirement nest eggs.

(in Greek tragedy) excessive pride toward or defiance of the gods, leading to nemesis

Who doesn’t want to love this place? AMIRITE?

I love Europe. I love it’s culture, its cities and architecture and the pace of life. I think in many ways Europe seems more usefully progressive, with things like public transportation and even energy. But god I am tired of hearing about Europe. Since the beginning of the financial crisis Europe has become the wounded, but never dying, member of some ill fated expedition. Every time the expedition seems likely to escape their fate, Europe goes and breaks an ankle…or something.

From an investment standpoint Europe makes a lot of sense. It’s the largest economy on the planet. It’s highly industrialized and very productive. It has created one of the largest economies by knocking down trade and exchange barriers between nations. It has many multi-national firms, advanced R&D, and exports much to the rest of the world. And yet it constantly represents a problem for investors.

I believe the source of that problem may be hubris. There’s not a lot of science around that statement, there is no Hubris Index to track (although that would be neat!), nor is there some ratio to calculate. But there is a pattern of behavior that seems to lend itself to such an analysis.

We should be clear though, you need hubris to do great things. Name a nation that has attempted to reach beyond it’s grasp and risen to great military and economic might and you will uncover a great deal of pride and arrogance. But something must temper that pride or what could have been great becomes the next Greek crisis.

Europe’s problem is that it seems to have little regard for the inner voice that advises caution. The Euro Zone, initially an economic endeavour to improve financial and diplomatic ties (the belief is that trading partners don’t go to war with each other) has spilled out into a messy, difficult and byzantine organization that has had a difficult time following it’s own rules. It has rapidly expanded into new markets, making it’s non-EU neighbors (like Russia) nervous about it’s intentions. It has turned countries with no business being part of the EU into powder-kegs ready to disrupt the whole experiment.

Ya, this isn’t a joke. This is a real law that real people spent real time making.

Europe has lots of problems, but almost all of them are their own making. Greece may have borrowed the money that exploded their debt, but French and German banks lent them that money. Concerns that a Greek exit from the Euro could trigger a domino effect as deeply indebted nations choose default over austerity is also the result of hubristic action. Countries like Spain and Ireland were hit with austerity because the government bailed out the banks, not because the government had mismanaged their finances.

All of this reeks of arrogance and overreach. But Europe has done this to itself, and the more we continue to hit regular road bumps on the road to financial well being, the more it looks like Europe is undoing it’s own purpose. It’s no surprise then that the economy that has recovered the quickest from 2008 has been the one supposedly worse hit. The United States has remained the foremost place for investors, safer, faster growing and more profitable than Europe. Europe, who is still dealing with the same problems of five years ago.

If this is meant to terrify Greece’s creditors, they seem ready to call the bluff. The deadline for Greece’s current payment to the IMF (€1.5 billion) is June 30th, the proposed referendum is to be on July 5th. This means that Greece will default before it’s had a chance to decide on whether they should default. If this seems like a grim picture for Greece, you have no idea how bad it is about to get.

Since 2008 Greece has limped along, periodically looking as though it is going to default on its massive and unmanageable debt. In 2010, when it seemed like a default was inevitable a bailout was organized that mandated strict and painful austerity in exchange for the financial aid needed to keep Greece within the EU. That austerity has left the Greek economy in shambles. Unemployment sits at around 25%, while pensions have withered, as have government jobs and a shrinking healthcare budget. Greece lost nearly 25% of its GDP from the pre-crash high, a rate unmatched by any other heavily indebted Euro country facing similar austerity measures.

Greece’s history with finances is checkered, if we are being generous. Greece has defaulted on its sovereign debt obligations five times since independence, and has been in default for nearly 50% of its time since gaining independence. Greece’s financial problems are also largely of their own making, having borrowed extravagantly at low interest rates and greatly expanded its government services while ignoring taxes has not earned it many sympathetic allies within the Eurozone.

This guy is Alexis Tsipras and he is the PM of Greece. He is not going to be remembered the way I think he wanted to be remembered.

But Greece’s situation is now quite dire. Greece produces little, has only a modest economy and owes far more money than it can ever reasonably expect to pay. Its economic prospects are slim and to retain any economic stability means adhering to austerity measures that gut and change pension obligations, raise taxes, reduce government sizes and heavily restrict benefits. That may be necessary tough love but it is also deepens Greece’s depression and throws into chaos the future of many Greeks, who only a few years ago thought they knew when they could retire and with how much money.

Choosing austerity within the euro would at least mean keeping some of the economics on track, and would allow the government to access in excess of €15 billion in continued bailout funding. But the path now set by Tsipras, seeking a referendum five days after the deadline seems to have set in motion an even worse set of events.

From The Economist. Greece remains an outlier within Europe, even amongst other heavily indebted nations.

The continued uncertainty in the negotiations through June has been putting considerable strain on an already taxed banking system. As negotiations have dragged on, Greek citizenry have been making significant withdrawals and transfers at their banks. To avoid a run the banking system it has been propped up by the ECB with Emergency Liquidity Assistance. But after yesterday’s referendum announcement the pressure on banks reached a breaking point. Thousands lined up at ATMs to get their hands on as many Euros as possible. In response the government has suspended banking for the next week and promised new capital controls to restrict transfers and withdrawals. That’s only the beginning of Greece’s banking woes.

Rick McKee / Augusta Chronicle

The ECB has said that if Greece defaults the emergency liquidity assistance will end, which means also a collapse of the Greek banking system. And while there is no official requirement for this ECB position, the unofficial reasons are obvious. Default cannot seem like a viable path for the austerity stricken countries, and financial markets need to be reassured that EU members won’t willingly walk away from their financial obligations to satisfy voters.

This means that a Greek exit will be worse than accepting continued austerity. It will mean more unemployment, poverty, government cutbacks and shrinking services. There is still time for a deal. The government can accept the creditor demands, institute further austerity, avoid a banking collapse and continue to use the Euro. But that may only postpone a fate we all know is coming. Greece’s debt is still too large, its economy too small, its creditors too stubborn and its options too limited to change the course it is on. Greece was always destined to fail, and sometimes we must come to learn that not all problems have solutions, only outcomes.

Liquidity is a sacred cow among the investing professional class and the importance of being able to sell and redeem an investment at a moment’s notice is a cornerstone of presumed investor safety and a hallmark of modern investing. In fact, improving liquidity has been a goal of markets and it’s a major achievement that there isn’t a commonly held mutual fund, ETF or stock that can’t be sold at the drop of a hat.

But in the same way that we can overemphasize the benefits of some health trends to the point of excluding other good for you foods, (I’m looking at you gluten free diet) the assumed exclusive positive benefits of liquidity can crowd out some very reasonable reasons to seek investments with low or limited liquidity.

Why would you choose an investment that can’t be sold easily? It’s worth pointing out all the ways that liquidity make investing worse. Volatility is increased by liquidity. High frequency trading, ETFs and trading platforms that let novice investors monitor the ups and downs of the market provide liquidity while magnifying risk. Sudden events best ignored become focal points for sell-offs. Liquidity is almost always the enemy of cooler heads.

Liquidity also costs money. For investments that are traditionally illiquid, like some bonds and GICs, redeemable options often trade at a discount. According to RBC’s own website the difference between a redeemable and non-redeemable GIC is 25 bps ( a quarter of 1%), which doesn’t sound like much, but when rates are as low as 1.5% for a five year GIC that is a 16% reduction in return.

Picture of the early Dutch stock market

The principle of investing has been that buying and holding something over a period of time would result in returns in greater excess than the rate of inflation. That rate of return is based on the associated risk of the enterprise and how long the investment should be held for. But into this mix we have also come to value (greatly) the ease with which we can walk away from an investment. It is the underpinning of a stock market that your commitment to a corporate venture need not be you, but that your financial role can be assumed by someone else for a price (your share).But that feature has come to dominate much of what we both value and hate about investing. Canadians are relieved to know that can sell their investments on short notice, protecting them from bad markets or freeing up cash for personal needs. But by extension things like High Frequency Trading use that same liquidity to undermine fair dealings within markets.

Are there reasons to not choose a liquid investment (aside from your house)? I think the answer is yes. For one thing we may put an unnatural value on liquidity. We pay for its privilege but we rarely use it wisely. The moment we are tempted to use liquidity to our advantage we usually make the wrong choice. Selling low and buying high are the enemy of smart investing, but all too often that is exactly what happens. Every year DALBAR, a research firm, publishes a report detailing investor behavior and its results are sobering to say the least.

Poor investor decisions have led to chronic underperformance by “average investors”. The inability to separate emotions from investing, and the ease with which changes can be made have led to meager returns. In the 2014 study showed that the “average investor” 10 year return was a paltry 2.6%, nothing compared to the return of most indices. That return got surprisingly worse over time, with a 2.5% annualized return over 20yrs and 1.9% over 30. Reduced liquidity could inadvertently improve returns for investors by simply removing the temptation to sell in poor markets; in those moments when our doubt and emotions tell us to “run”.

This is from the 2014 DALBAR QIAB, or Quantitative Analysis of Investor Behavior.

So what types of investments are typically “illiquid”? Such products are normally reserved for “accredited investors”, or investors that have higher earnings or larger net savings. These deals are traditionally considered riskier and would be unsuitable for a novice investor (unfamiliar with the risks) or ill-suited to someone who might need to depend on their savings on short notice. That makes a lot of sense and any manager worth their salt would tell you that you shouldn’t tie up your savings if you might need them. But it is worth considering whether we have let our obsession with the convenience of liquidity undermine our goals as investors. Something to consider next time the urge to sell in bad markets comes upon you.

I can not find a better metaphor for Canada’s housing market than this image from the movie UP! (Which is a film I highly recommend)

If you’re looking for some good reading Google “Canadian Housing Bubble” and you could fill a library with the amount of material available. There isn’t a week that goes by without some new article somewhere screaming with alarm about Canada’s precarious and overvalued housing market. I’ve written many myself, but in conversation almost everyone admits that regardless of the danger nothing seems to abate the growth in home values.

The history of the average five year mortgage in Canada going back to the mid 1960s. It’s hard to believe that Canadians once paid interest rates in excess of 20% to buy a home. Today rates are at an all time low and unlikely to rise anytime soon. From the Globe and Mail, published May 13, 2015

This defying of financial gravity gives ammunition to those that doubt there is any real risk at all. The combination of low interest rates, willing banks, rising prices and an aggressive housing market has given a veneer of stability to an otherwise risky situation. Combined with the “sky is falling” talk about the house prices and it is easy to understand why many simply accept, or outright dismiss, the growing chorus of concerns about house prices.

Nissam Taleb’s book “The Black Swan” highlighted that negative Black Swan events tended to be fast, like 2008, while positive Black Swan events tended to be slow moving, like the progressive improvement in standards of living since the end of the Second World War. But it would be fair to say that creating a negative event requires a prolonged period of danger creep, a period where a known danger continues to grow but remains benign, fooling many to believe that there isn’t any real danger at all.

I would argue we are living in such a period now. The housing market is continuing to grow more precarious and many Canadians are finding that their own financial well being is connected to their home’s appreciating value. Between large mortgages and HELOCs, Canadians are deeply indebted and need their home prices to continue to inflate to offset the absurd level of borrowing that is going on.

As an example of how the “danger creeps” have a look at this article from last week’s Globe and Mail which highlights a young couple living in Mississauga with a burdensome debt and an unexpected pregnancy. They are classified as some of the “most indebted” of Canadians; house rich and cash poor. By their own estimates they are over budget every month and 100% of one of their incomes goes exclusively to pay the mortgage, stressful as that is they aren’t worried. It may seem irresponsible on their part to buy such a home, but they couldn’t do it if there weren’t many others complicit in making such a bad financial arrangement. Between lax rules from the government, a willing lending officer and well intentioned families that help out, it turns out that creating a financially fragile family takes a village.

A nation of debtors is a vulnerable one indeed. I’ve often said that financial strength comes through being able to withstand financial shocks, and this is exactly where Canadians are falling short. It’s the high debt load and minimal savings (and that these two issues are self-reinforcing) that make Canadians vulnerable. A change in the economic fortunes would force many Canadians to deleverage and in the process would inflict further damage to the economy and likely many homes onto the market.

Such an event is strictly in the “uncharted seas” sector of the economy. No one has a clear idea what it would take to shift the housing sector loose, or what would happen once it did. And that’s just the unknown stuff. With interest rates at an all time low it would also only take a small increase in the interest rate (say 2%) to bump up many people out of their once affordable mortgage and into unaffordable territory.

That’s the problem with slow growing danger, it has a glacial pace but when it arrives it is already too large to be dealt with easily. In one of my favorite movies, the Usual Suspects, Kevin Spacey utters the line “The greatest trick the devil ever pulled was convincing the world he didn’t exist”. That’s something we should all be wary of, the longer the housing market stays aloft the more convinced we become that not only is it not dangerous, but that there was never any danger at all.

Margaret Wente is both enjoying the perks of her “seniority” and worries that we may be undermining the future.

Over the weekend one of my clients posted an article from Margaret Wente about the many privileges bestowed upon seniors in Canada. Listing an almost unbelievable number of perks for “elderly” Canadians, which ranged from discounts at drug stores and movie theaters to government pensions and new federal tweaks to retirement programs, in every way seniors in Canada have it pretty good.

So good in fact that Margaret Wente has begun to despair. Not for herself, but for the future. The younger generation is definitely having a tougher time than their parents. And while none of this predicts that the Millennial’s will be poor, it does go to the heart of the uneven balance about finances that exists between generations.

What’s happening is that we live in unprecedented times. Unprecedented in the life span of those living, the material wealth we have available to us, and the inverted demographics that comprise many countries around the globe. Everywhere people are richer, living longer and getting older. Many of our concerns about the economy, the cost of living, or the security of programs like CPP, or Social Security in the United States, are born directly from our success at creating a higher standard of living. Higher wages, better medicine and a declining birth rate make us materially richer, until they don’t.

Courtesy of Gapminder

What you are looking at in the above chart is the changing nature of both Canada’s and the worlds age. From 1950 on Canada briefly saw a boom in the birth rate that has since reversed itself. The number of Canadians over 60 (the y-axis) is now better than 20% of the total Canadian population, while the number of children (on the x-axis) has been steady at about 5%.

“So, we’ll give them a little money to tide them over until they die, which will only be in a couple of years anyway, no long term financial entitlements for us!”

All the goodies that benefit the senior class of Canadians are getting more costly both because Canadians are living longer, but also because the tax-base needed to support many of those services is shrinking. But are seniors “too rich” as Margaret Wente thinks? Probably not. While Canadian poverty rates for the elderly are some of the lowest in the world, people who retire at 65 need to make all their savings last them until they are ninety, or older. You try and figure out what you are going to spend for the next 20-30 years. When Otto Von Bismark introduced the worlds first old age pension, it was for people who were 70 years old and their life expectancy was for maybe two more years. Today people retire and they live another lifetime. As we’ve previously said, when you’ve retired you’ve earned your last dollar. That can be a pretty scary thought.

The solution? There isn’t one. As I said these are unprecedented times. We still treat retirement like those who hit 65 are “old”. When my grandfather was 12 he had finished school, worked in

This book was written in 1997. 1997! It’s taken 20 years for it to be relevant.

a factory and eventually fought in the Second World War. By the time he was 65, suffering from lung deterioration after a life time of smoking, his face bore every year like the rings of a felled tree. My father on the other hand just had his 70th birthday and looks barely 60. That isn’t good genetics, that’s the product of good living. This trend is global, affecting everyone from China to Canada, and it will be with us for a long time. For many years people have been sounding the alarm about the demographic storm that is approaching, but such storms are slow moving. This is the beginning of a much larger set of conversations that will begin to address how we perceive retirement, savings, economic growth and government programs like the CPP. How we ultimately address and resolve the burgeoning conflicts about age and wealth will put many of us, and our retirement plans, to the test.

“Justin is in favour of making you pay more taxes! Vote Justin!” Okay, maybe it needs work…We recognize that articles that involve politics can be pretty personal. The Walker Report is not endorsing or denouncing any politician or party, but merely commenting on current events.

The growth of TFSAs definitely will hit tax revenues for the government. This year alone it is estimated to reduce revenue by $85 million, and in a few years that number will be over $350 million. By 2035 estimates put it will be close to $650 million in lost tax revenue. However we should be wary about attaching too much importance to long term estimates. Economic growth, population trends, even the price of oil will play a larger role in government revenues than the TFSA. We can barely get a fix on the price of oil over the next six months, so there is little use in getting worked-up over decade scaled predictions.

This leaves the other chief complaint about the TFSAs, that they only benefit the wealthy. There is some truth to this. The wealthiest Canadians are certainly in a better place to capitalize on multiple different forms of tax sheltering. But that is always the case. The wealthiest among us are able to capitalize on all things more effectively, from designer purses to sports cars. The question for average Canadians is can we also benefit from TFSAs?

Notably, this car will likely only benefit the wealthy.I think the answer here is a resounding yes, and in some ways we may be able to capitalize on TFSAs more effectively. For young Canadians who still find their finances precarious it can be beneficial to place money somewhere to grow while still retaining access to it. For Canadians who receive an inheritance (a situation that will become increasingly common in the coming decades) such a sum might overwhelm available RRSP room. The TFSA will prove to be welcome relief for intergenerational wealth. For retirees who are forced to take more from their RRIFs than they would like or need, the TFSA is a suitable home to reinvest going forward.

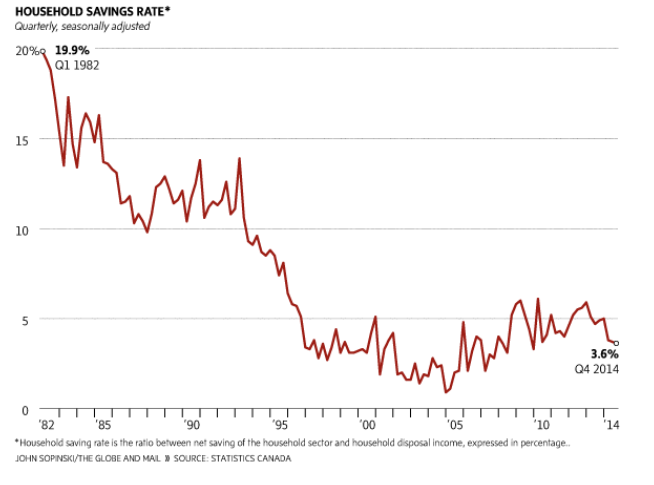

But we should all keep in mind how often a dollar that is earned, invested and spent again will be taxed. Income taxes come off your earnings, capital gains and dividend taxes will be carved from your investments, and sales taxes will be collected when it is spent again. TFSAs promise to relieve only one part of this equation, we should welcome even this small relief. Canadians in particular have need of it. Our savings’ rate is pitifully small, and has been declining for decades. The number of Canadians without pensions and suitable retirement funds is alarmingly high, and we have no simple solution to fix any of it. Decreasing long term tax revenues in favour of creating better savings opportunities isn’t a crime, it’s a blessing, one that we can all benefit from.

Well not really, but they have joined my cause on the problems we face with regards to urbanism and increasing urban density. It’s not everyday that you can say that the economist endorses your position (even if they don’t know it) but in early April my constant nagging about the insane price of housing became a feature for the weekly.

Canada’s housing market is therefore a confusing and expensive mess. The risk is high but the need for housing is great and this fuels a great deal of arguments over how great the problem in Canadian housing really is.

But the problem goes beyond merely being frustrated by increasing realty costs. Housing is a significant aspect to any economy. Building homes makes a lot of jobs, but affordable housing encourages a growing economy. As home prices eat up income there is simply less money to go around. It hurts domestic growth, slows trade and reduces standards of living.

The culprit is not a big bogeyman like the banks (though they are benefiting from this situation) but ourselves. In an effort to improve aesthetic standards of living by restricting changes to our surroundings we have unwittingly hurt our economic standard of living. Almost every city today is burdened with development guidelines and urban bylaws that restrict density and height. These rules run into the hundreds of pages and fill volumes in most city halls around the globe. It’s made cities like Bombay one of the most expensive in the world in a country that is one of the poorest. It restricts taxes and hinders economic and city improvements.

And cities need taxes. We tend to be critical of enormous budgetary outlays for cities, but whether it’s a new subway line in Toronto or a super-sewage pipe in Mexico City, cities depend on the taxes that are generated primarily through dense urbanization. This week the free newspaper Metro published an article showing which wards in the city of Toronto contribute the greatest amount in taxes. Unsurprisingly the “downtown” wards contributed the bulk of city revenue. Wards out in Scarborough had some of the lowest, a difference in the hundreds of millions of dollars for city revenue. Some are quick to point out that the “lie” about spoiled downtowners, but the reality is that density improves economic performance and reduces the burden of taxes while improving its efficiency.

The Economist argues that we waste space in cities, and that comes with a high cost. According to their article the US economy is 13.4% smaller than it could have been in 2009, a total of $2 trillion. Because cities that offer high incomes (like San Francisco) become too expensive people endup working in lower productivity sectors, while making it difficult to live for those that choose to reside in those cities. In the case of Canada this potentially fueling an enormous and dangerous housing bubble while undermining our economic growth. But this is a problem of our own doing. Through our own efforts we have masterminded a situation that threatens our own economic well being. The question that remains is whether we can be clever enough to undo it before it hurts us all.

As for The Economist I will assume they should be calling me anytime to start writing for them regularly….

As Canadians we are all familiar with the dispiriting feeling of traveling abroad and finding out our money just doesn’t travel as far with us. Canadians for generations have felt the plight of coughing up extra to go to the United States, the UK and Europe. That was until recently. As the Canadian Dollar hit parity back in 2007 and remained strong through the financial crisis we may have felt that we could hold our heads a little higher on vacation. Perhaps daring to order the steak while out with the family.

Our dollar is sometimes called a petrodollar, or petrocurrency, which means that the price of oil and the value of our currency are interlinked. As the price of oil rises so too does our dollar, hurting domestic manufacturing and improving the lives of Canadian tourists everywhere. But rising and falling dollars also have an impact on our investments, complicating portfolios and either diminishing or improving returns, like an unwelcome fifth column.

For instance, back in 2007 the sudden rise in the dollar made two types of investments popular. Canadian equity funds, (specifically energy and natural resources) and currency hedged global funds. While other markets had done well they couldn’t keep up with the ascension of the dollar, and by the end of the year the buying power of the dollar had outpaced the growth of many investments. Since 2013 the dollar has lost 20% of its value, undoing that previous balance and making unhedged foreign investments more attractive.

Hedging works by protecting the value of the currency against future changes. If you hold a currency hedged investment, the true performance will always show through, regardless of good or bad markets. When a dollar is falling unhedged investments are more appealing since a falling local currency means your foreign investments are worth more. This can mitigate bad markets, so if performance is anemic in the United States, but the Canadian dollar has dropped by 5% or 6%, you will still show a strong gain on your US holdings.

So how much time and energy should people dedicated to currency hedging? Some people argue that you should always currency hedge (so you see the accurate performance) while others prefer to let it currencies play out, and still others like to tactically manage both. In my experience it has been easier to pick funds where managers either always or never hedge, since claims to be “tactically managed” are either too small to matter, or currency swings are too fast and unpredictable to be suitably countered. For myself I prefer to use currency hedging to try and reduce volatility rather than capture more performance.

George Soros – Currency Superhero!

Currency trading is very risky, and those who do it successfully may be super human. Nevertheless there are books that encourage mere mortals to gamble with the direction of currencies and try and profit from those swings in value. That seems crazy, if only because my approach to dealing with currencies is to try and mitigate their impact, not try and profit from their unpredictability. Regardless, opportunities abound for individual “do-it-yourself-ers” to throw money at currencies and try and make some money.

The title of this book is called Currency Trading for Dummies. Take the hint.

So how should Canadians mange currency exposure? One (terrible) idea is to only invest in Canada, but after a couple of years of writing this blog I don’t think I should need to explain why. Another, perhaps better, idea is for Canadians to be mindful of when they need their money. If saving for retirement is about balancing risk versus time, currency hedging or employing some currency hedging can become more useful as you get closer to needing your money on a regular basis. It may reduce growth as dollars depreciate, but protect against significant and unwelcome swings. If you are younger and investing for the long run currency swings tend to work themselves out and the fluctuations will mean less over time. But the best thing for all investors to do is ask their financial advisors for guidance about currency hedging and what will make them most comfortable with their retirement plans.

Last week most of the world was expecting a chaotic, but unavoidable Greek exit from the Euro, but following more final, final negotiations a deal was ultimately hammered out between Greece and it’s creditors. A quick glance over much of the media shows that many view the new bailout as a temporary reprieve at best, and an extension of a cruel policy at worst. Greece gets more debt, more austerity and zero concessions from Europe.

Last week most of the world was expecting a chaotic, but unavoidable Greek exit from the Euro, but following more final, final negotiations a deal was ultimately hammered out between Greece and it’s creditors. A quick glance over much of the media shows that many view the new bailout as a temporary reprieve at best, and an extension of a cruel policy at worst. Greece gets more debt, more austerity and zero concessions from Europe.