Amidst all the various news during this ongoing pandemic, reports that American billionaires are getting richer, particularly those focused in tech, is unlikely to bring anyone much comfort. Though much is often made of income inequality, I tend to believe that inequality in of itself is not a pressing concern for most people. What does stick in the minds of your average citizen is that no matter what tragedy seems to befall the world, the richest keep getting richer, while their own situation continues to erode.

There are two interconnected factors at play here. One is how billionaires continue to do so well. The other is related to declining fortunes and mobility for a middle class that is less middle, but increasingly more class orientated.

The rise of a super-rich has a great deal more to do the dominance of the stock market in an age of globalization than any other single factor. You’ve probably heard some statistic like this before, that in the past a CEO would only have made 20x more than their lowest paid employee, only to find now that the ratio is 278x more than the average worker. Much of this shift has been a result of moving compensation for CEOs and C-level executives into stock options, a move aimed at improving governance, but has instead hyper charged the importance of stock returns in an increasingly globalized world.

In his book Land of Promise by Michael Lind, he has this to say about globalization and global trade: “Between the end of the Cold War and the crash of 2008, globalization resulted in the organization of one global industry after another as an oligopoly, with most of the transnational enterprises headquartered in the United States, Europe, or Japan…Two companies, US-based Boeing and Europe’s Airbus, had 100 percent of the global market share in large jet airliners. Among their suppliers, the global market for jet engines was divided among three firms: GE, Pratt and Whitney, and Rolls-Royce. Microsoft enjoyed 90 percent of the global market share for PC operating systems. Four firms divided 55 percent of the PC market among themselves, while three companies shared 65 percent of the mobile handset phones. Three firms dominated the world market in agricultural equipment (69 percent) and ten companies dominated the global pharmaceutical market (69 percent). Ninety-five percent of microprocessors (chips) were made by four companies – Intel, Advanced Micro Devices, NEC, and Motorola. Four automobile companies – Gm, Ford, Toyota-Daihatsu, and DaimlerChrysler – manufactured 50% of all cars, while three firms – Bridgestone, Goodyear, and Michelin – made 60% of the tires. Owens-Illinois and Saint Gobin made two-thirds of all glass bottles in the world. Concentration in global finance was accelerated by US deregulation, which allowed the emergence of a small number of US megabanks, some of which grew even more during the Great Recession when, with the support of the US government, they absorbed failing banks, as Bank of America took over Merrill Lynch and JP Morgan Chase acquired Washington Mutual.”

However you may wish to slice it the system of globalization has been a huge boon to the wealthiest globally, consolidating wealth amongst an increasingly narrow group of companies and the people who own the bulk of the shares within those companies. And the more importance share holder returns have taken on, the more consolidated those companies have become.

The second problem I’ve mentioned is that of a middle class that is increasingly stratified. While the wealthiest keep getting wealthy, the middle class has followed suit, locking in wealth and reducing income mobility. While we may not consider life in the 1950s or 1960s particularly egalitarian, aspects about that more sexist and racist time in our past better facilitated economic mobility. For instance, a world where women did not hold many corporate positions of authority and didn’t work after marriage was also a world where women were more capable of “marrying up”. In contrast, today educated professionals marry other educated professionals. A surgeon is less likely to be married to a secretary and more likely to be married to another surgeon. The economist Tyler Cowen has called this “matching” in his book The Complacent Class, with people better able to “match” to those with similar interests and backgrounds. The effect of this “matching” has been to stratify wealth and decrease social mobility within the middle class.

Education represents another significant change that is stultifying the middle class. Education, particularly secondary education took on increasing importance in the 1980s, as those with university degrees started to out earn those with just high school, and those with professional designations (like lawyers and doctors) out paced those with just an undergraduate degree. Would more education fix this? Not really. As the cost of education continues to rise and new technologies filter into even white-collar jobs, young lawyers and accountants struggle to find work, while the management of major companies hangs in longer. The return on education continues to decline even as the costs go up, leaving those who come from wealthier educated families financially better off and better socially connected than those coming from lower income families trying leverage education into higher tax brackets.

Education represents another significant change that is stultifying the middle class. Education, particularly secondary education took on increasing importance in the 1980s, as those with university degrees started to out earn those with just high school, and those with professional designations (like lawyers and doctors) out paced those with just an undergraduate degree. Would more education fix this? Not really. As the cost of education continues to rise and new technologies filter into even white-collar jobs, young lawyers and accountants struggle to find work, while the management of major companies hangs in longer. The return on education continues to decline even as the costs go up, leaving those who come from wealthier educated families financially better off and better socially connected than those coming from lower income families trying leverage education into higher tax brackets.

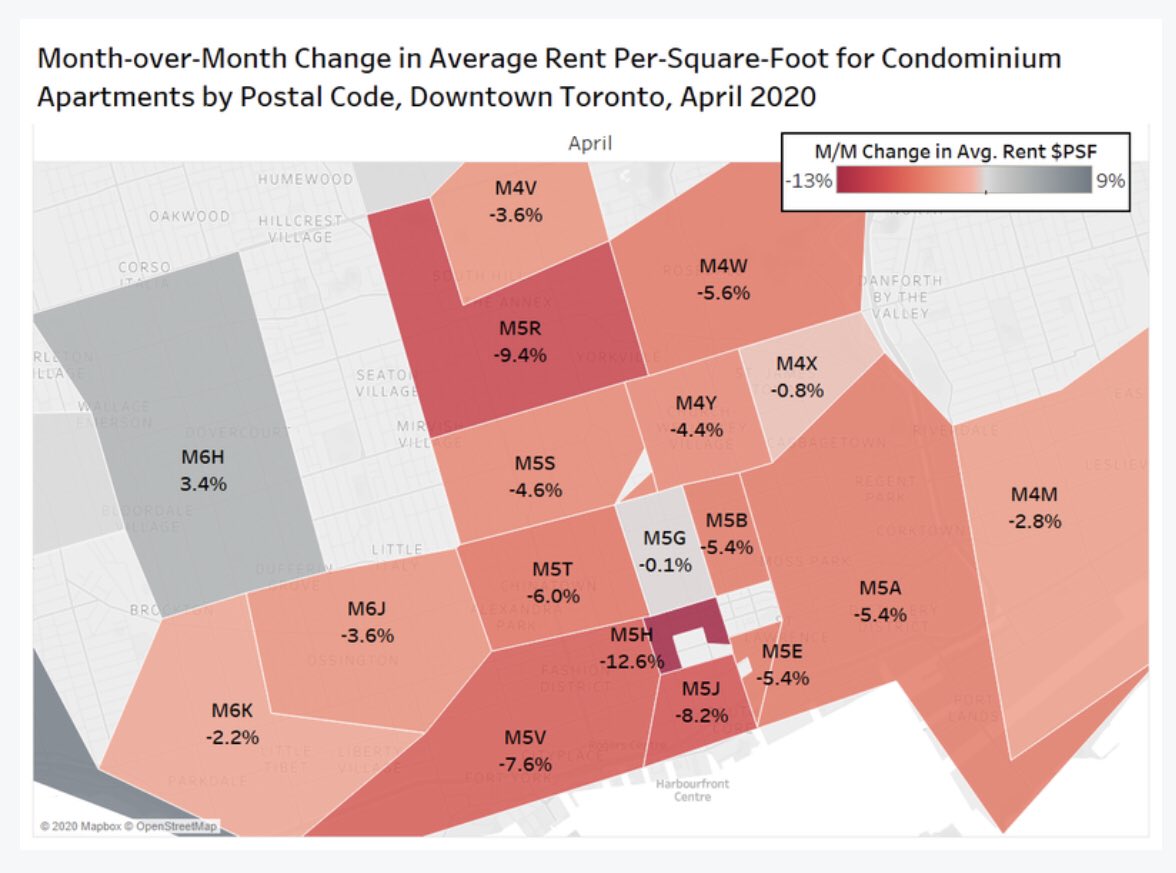

Similarly, costs of living continue to climb in essentials. In Toronto, where housing prices have climbed steadily for the last two decades, it has given birth to an intransient NIMBYism. Homeowners, having taken on large amounts of debt to get into the housing market are generally protective of their neighborhoods and tend to push back hard on attempts to increase density for fear it pulls down housing value. Poorer neighborhoods in cities like Toronto find themselves pushed out by gentrification, an ironic blend of resistance to development that increases the price of living while denying the development that could keep prices lower for a more diverse group of residents to live together. The effect is one where neighborhoods may indeed be racially diverse, but not income diverse. The effect to a middle class is to be both more precarious and less open.

The response from governments to both these changes hasn’t been encouraging. Playing around with the tax rates, trying to force people into expensive four-year degrees, potentially embracing a universal basic income (UBI) amounts to tinkering with the system, not fixing it. And while UBI has garnered a lot of interest, it smacks of an acceptance of the current situation. If you can’t get ahead, here is some money to make life more tolerable. A population of people dependent of a government stipend is not a population that is very free. But if politicians efforts are well meaning, distrust of them remains understandable, as the political class and billionaire class rub elbows at places like Davos, recommitting to strengthening the very system that seems to be the source of many of the present issues.

Over the past several years I have dedicated this blog to the issues I think that remain most pressing from a financial standpoint to our society, frequently touching on issues of housing prices, technology, anti-urbanization, populism and the middle class. All these issues seem to be accelerating, and if there is a thought that might bind these ideas together it is a sense of loss of imagination on how we deal with major issues. In addition to a consolidation of corporate power and wealth amongst a smaller group of people, we also see fewer companies with IPOs, and fewer companies listed on the stock market in general. There is also less imagination from our political class, which remain wedded to a narrow set of ideas about how to deal with new problems.

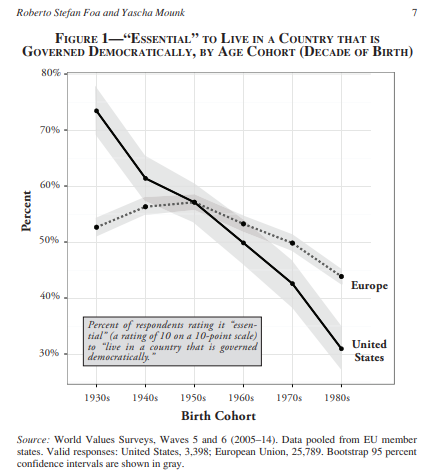

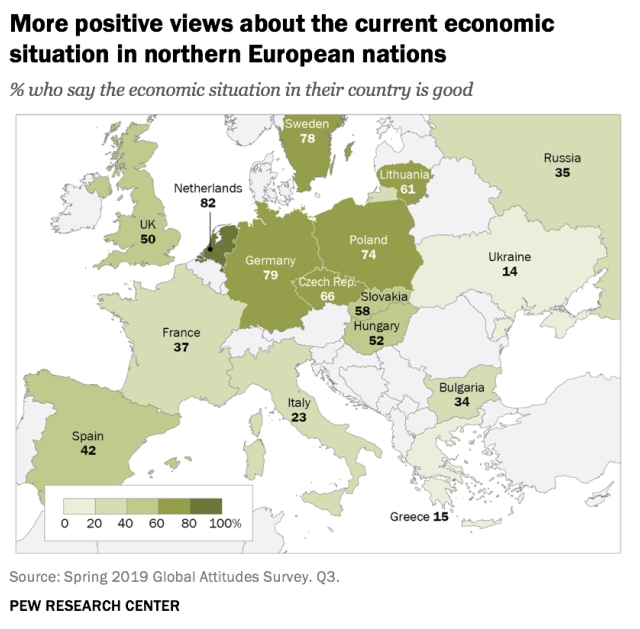

Successful societies like Canada can be handcuffed by their past achievements, limiting options to things already tried before. But problems that do not get fixed don’t go away. Instead they fester, presenting themselves in other more threatening ways. As I write this there are riots in Minneapolis, ostensibly about the death of a citizen in police custody (part of a long list of Black Americans killed at the hands of police for nonviolent offences) but that riot has swiftly turned towards an affordable housing project and local big box stores in addition to the police. In a 2016 poll, only 30% of Americans born in the 1980s believed that living in a democracy is essential, the lowest since such polling had begun. In Europe polling showed that the core countries of the EU; Spain, France and Italy, had largely negative views about their current economic situation a decade on from the Great Recession.

Now, in the middle of this global pandemic, many of these fault lines are being exposed. There may be no better way to sum up our situation than to speak of Walmart, a store that exists and thrives because of the globalized order, importing products from China. According to Ian Bremmer, the largest employer among Fortune 500 companies is Walmart, employing 2.2 million people, easily out pacing any other single company. In 2003 the CEO of Walmart, H. Lee Scott, earned 1500 times as much as a full time Walmart employee.

This trend is not confined to Canada or the United States. It is global, and affects China and India as much as it does the West. But the effect on populations of an economic story that increasingly benefits the wealthiest, while making middle classes more precarious and defensive is to undermine the legitimacy of democracies. The backsliding of democratic countries, and the erosion of the international order is connected to these domestic economic challenges. The pandemic is speeding up this inequality effect, and how we rise to meet it will play a large roll in deciding who calls the shots in the 21st Century.

Author’s Note – In addition to the normally sourced articles I’ve relied on several books for this article, they include:

- Plutocrats: The Rise of the New Global Super-Rich and the Fall of Everyone Else by Chrystia Freeland

- The Retreat of Western Liberalism by Edward Luce

- The Complacent Class by Tyler Cowen

- Income Inequality, The Canadian Story (Volume 5), Edited by David A. Green, W. Craig Riddell and France St. Hilaire

- Land of Promise by Michael Lind

Information in this commentary is for informational purposes only and not meant to be personalized investment advice. The content has been prepared by Adrian Walker from sources believed to be accurate. The opinions expressed are of the author and do not necessarily represent those of ACPI.

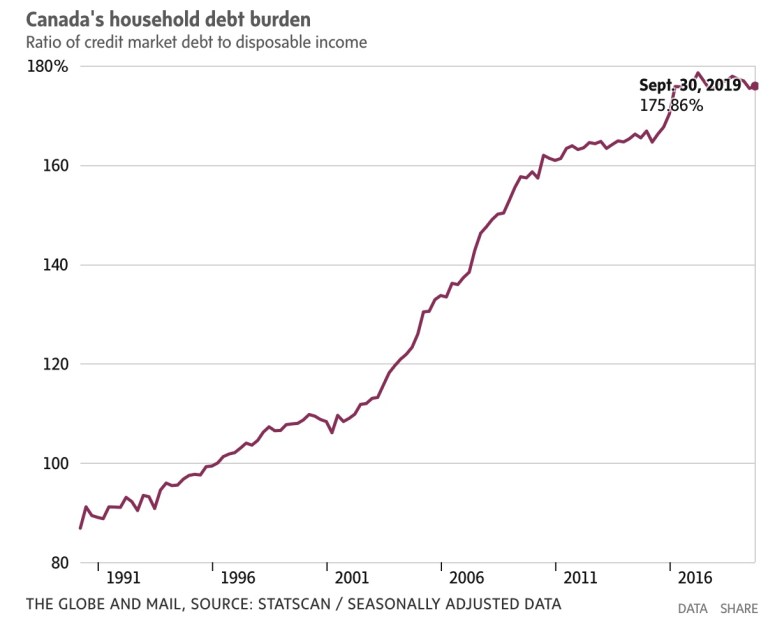

Real estate remains at the heart of the Canadian economic story for the last 20 years. Appreciating housing prices are the chief source for growth in Canadian families’ net worth. Borrowing to buy houses and borrowing against home equity remain our chief sources of debt. Our politics revolves around the tension of needing more housing in certain highly desirable areas while preserving those areas from over development. That dynamic has revolved around a status quo that seemed to have no conceivable end. The pandemic may have radically altered the Canadian real estate landscape regardless of how people feel about it or what they want. Whether we can walk back changes of this magnitude remains very much unknowable. For now we can only watch the changes our society and economy are undergoing and hope that what we are witnessing will be for the best, those changes that have happened, and those yet to come.

Real estate remains at the heart of the Canadian economic story for the last 20 years. Appreciating housing prices are the chief source for growth in Canadian families’ net worth. Borrowing to buy houses and borrowing against home equity remain our chief sources of debt. Our politics revolves around the tension of needing more housing in certain highly desirable areas while preserving those areas from over development. That dynamic has revolved around a status quo that seemed to have no conceivable end. The pandemic may have radically altered the Canadian real estate landscape regardless of how people feel about it or what they want. Whether we can walk back changes of this magnitude remains very much unknowable. For now we can only watch the changes our society and economy are undergoing and hope that what we are witnessing will be for the best, those changes that have happened, and those yet to come.