Following up from a previous video (Why investors are told to stay invested in bad markets), we must recognize that we can’t always pick and choose when we need money from our savings. So how should we pick what investments to sell in a poorly performing market? Here’s one strategy to consider and help guide you!

As always, I’m available to talk any time and can be reached on my cell phone, through our office number or via email!

Sincerely,

Adrian Walker

Information in this commentary is for informational purposes only and not meant to be personalized investment advice. The content has been prepared by Adrian Walker from sources believed to be accurate. The opinions expressed are of the author and do not necessarily represent those of ACPI.

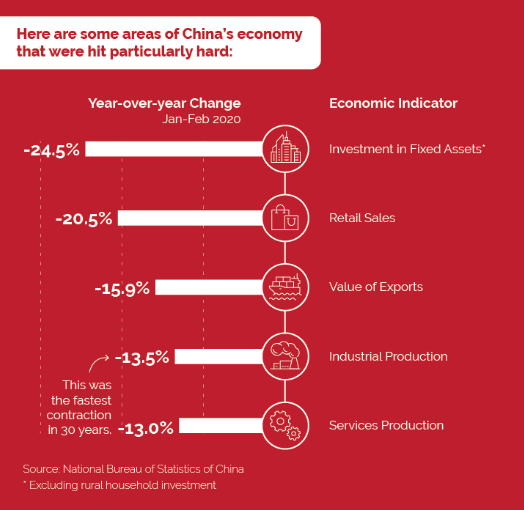

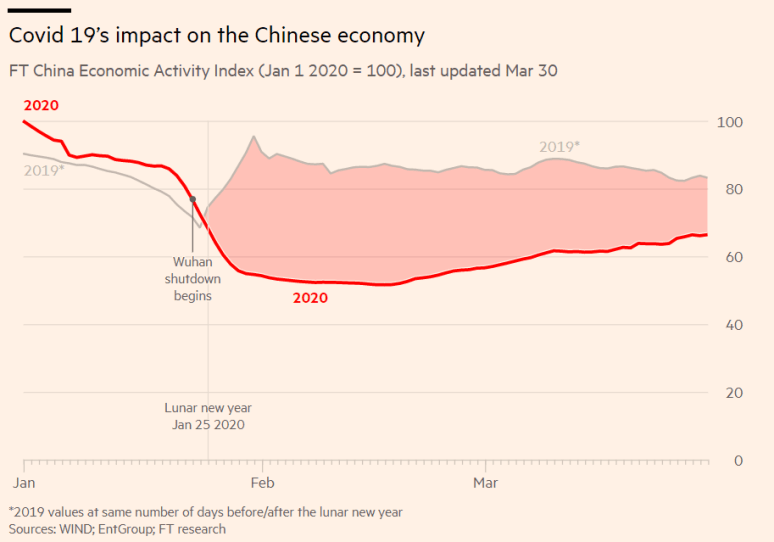

China, the first hit by the coronavirus and the first to emerge from its enforced hibernation, is the global centre of attention as people watch to see how fast its economy can recover from the from the pandemic chaos unleashed in January. If China is able to bounce back quickly it will be good news for other countries and should raise spirits of investors, businesses, and governments that a global shut down may not lead to the worst of all worlds.

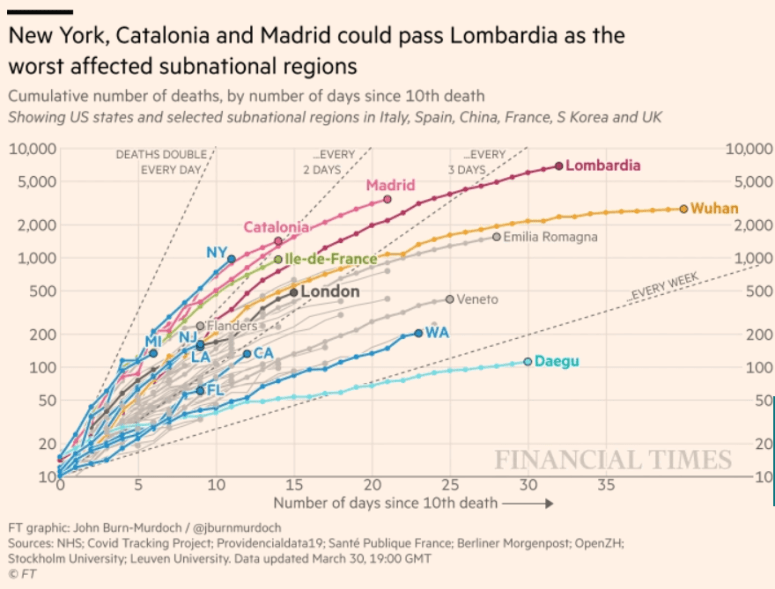

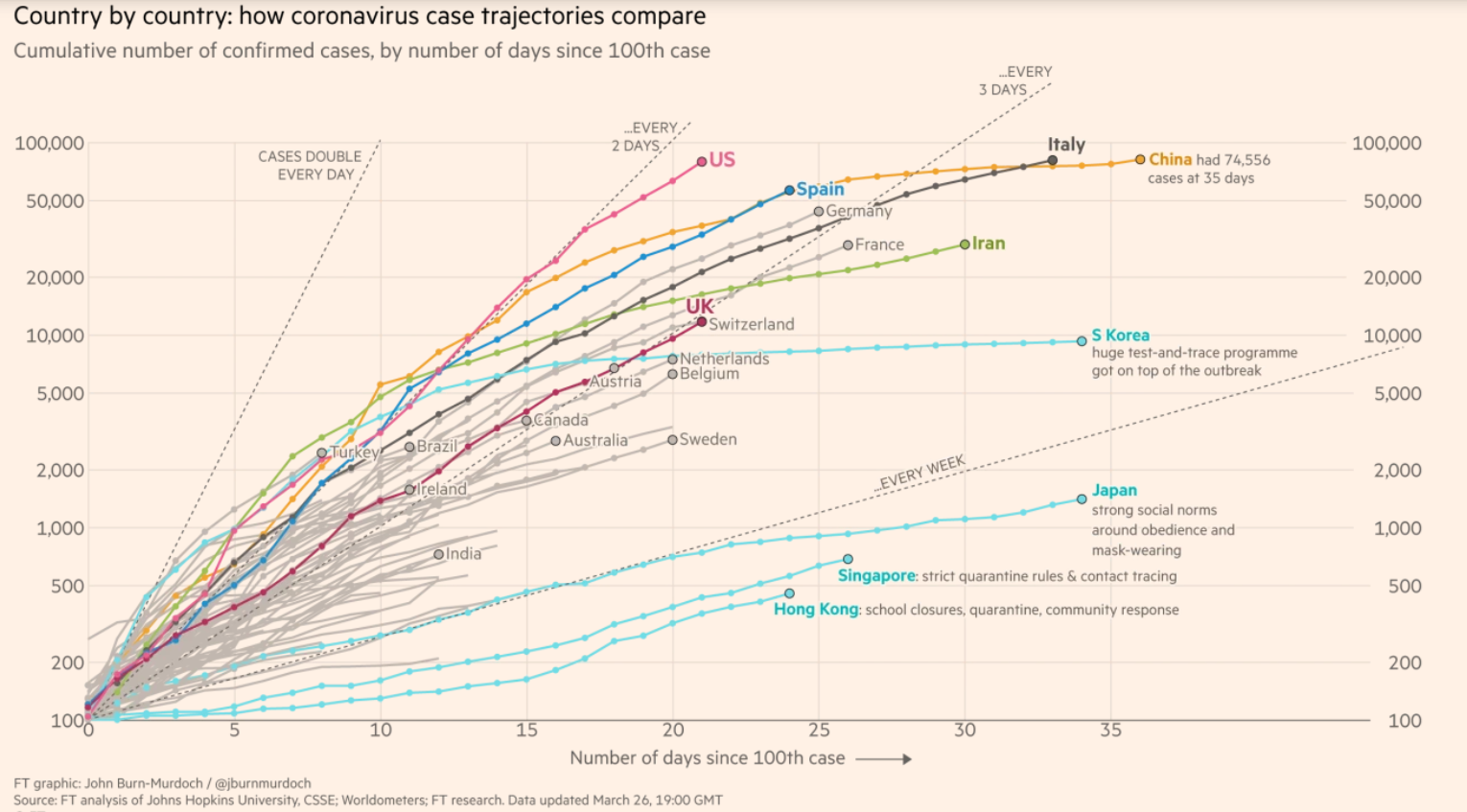

But economic activity is still well below 2019 levels and have a way to recover. In addition, China is one nation, the Western economy is made up of many, and the countries worst hit by the COVID-19 outbreaks have yet to peek and plateau. Italy, Spain and the United States are all fairing poorly, with Italy and Spain perhaps just finally reaching peak of cases now. The United States on the other hand now has more officially recorded cases than any other country, while New York, Catalonia, and Madrid are on track to pass Lombardia as the worst affected cities both in infections and mortalities.

The coronavirus remains the central unknown in this story. If tamed, can it be permanently subdued? If not, can new cases be dealt with on a case by case basis, or will we have to revert to aggressive forms of social distancing? Concerns remain about whether there will be a second wave of infections in Asia, while China has maintained that all new cases are being imported and can be dealt with proactive screening and testing.

In Europe and North America the best news has been to see production of ventilators, masks and the deployment of field hospitals ramp up to deal with the threat. In the wider Asian region, wide testing and a willingness to follow government dictates and a focus on personal protection through the adoption of wide mask usage has had a direct impact on taming the virus in Taiwan, South Korea and Japan (the exception here might be Japan, which seems to have relaxed prematurely and now is considering shutting down Tokyo). But the best news may still be from China and a sudden and rapid improvement in their economy as restrictions are lifted. If prolonged the early rally than began last week, and has continued yesterday and through overnight trading may become the foundation for a more sustained recovery. If not markets may be thrown back into turmoil.*(Please note, markets seem to be in turmoil again.)

Today, at the end of March, I think the potential for a slower recovery remains possible. Huge stimulus packages have been put in place by governments to help ease the worst of the economic fallout. Governments and their citizens seem to be facing the challenge head on, even if they have been late to the game. America’s enormous manufacturing capacity is being used usefully to deal with the pandemic (better late than never) and early economic news from China is encouraging, but should be treated with caution.

Information in this commentary is for informational purposes only and not meant to be personalized investment advice. The content has been prepared by Adrian Walker from sources believed to be accurate. The opinions expressed are of the author and do not necessarily represent those of ACPI.

A quick video looking at the sudden rise in markets last week and what conclusions we can draw from it.

Information in this commentary is for informational purposes only and not meant to be personalized investment advice. The content has been prepared by Adrian Walker from sources believed to be accurate. The opinions expressed are of the author and do not necessarily represent those of ACPI.

Markets have been bullish the last few days, moving off the most recent lows and easing the strain on investors who have watched their savings tumble by up to 35% since the beginning of the year. Any enthusiasm that this will be a sustained recovery should be tempered by the sheer scope of the economic disruption that we are facing, how early into the problem we currently are, or the potential for a pandemic disaster in the United States, which now has officially more cases than China ever did.

While I remain grateful for the respite we’ve seen, however fleeting, the problem that sticks out in my mind is that of the tangled web of Canadian debt, growing insolvencies, and hundreds of empty condos in downtown Toronto.

Problems rarely exist in isolation, and a problem’s ability to fester, grow and become malignant to the health of the wider body requires an interconnected set of resources to allow its most pernicious aspects to be deferred. In Canada the problem has been long known about, a high level of personal debt that has grown unabated since we missed the worst of 2008. What has allowed this problem to become wide ranging is a banking system more than happy to continue to finance home ownership, a real estate industry convinced that real estate can not fail, and a political class that has been prepared to look the other way on multiple issues including short term rental accommodation, in favour of rising property values to offset stagnant wages.

Recently I was at a round table event on Toronto real estate shortly after the COVID-19 situation started to gain real traction in late February. Benjamin Tal, Deputy Chief Economist for CIBC Capital Markets, described the Canadian real estate scene as “having 9 lives”, every time it seems like house prices can go no higher, something happens to prop up the market. At that moment it was the likely cut in interest rates and an easing of the stress test for mortgages which might breathe more life into the over heated housing market. But that was before international travel dropped off, before national states of emergency, before social distancing, before borders were closed, before essential services, before #lockdowns and #quarantinelife. Tal may not have been wrong conceptually, he simply hadn’t considered that the world might close for business.

Canadian debt has been kept afloat because nothing could conceivably undermine it. And now, in downtown Toronto, condos sit empty. Airbnb hosts have no customers. Costs are mounting and there is no immediate end in sight to the pandemic, no end date that people can bank on. This week 3.3 million Americans filed for EI. In Canada the number was around 1 million. Even the most generous stimulus packages are unlikely to fix a debt problem as big as Canada’s.

True, there is some hope in mortgage deferrals, but scuttlebutt is that banks aren’t very liberal on this matter, telling many that they don’t qualify regardless of political pronouncements. This problem isn’t limited to Toronto. In Dublin rental accommodation jumped by 64% as COVID-19 became a crisis and people began looking for long term tenants to replace the short term ones. Short term thinking by investors, banks, and politicians has facilitated a serious economic problem. But to its enablers it seemed unlikely that there was a scenario that could conceivably expose its flaws.

It is becoming ever clearer that the focus for citizens in the 21st century should be on resilience. Expedience and an assumption that the stability of the recent past is prologue is now a dangerous and toxic combination, creating risks and magnifying bad decisions. Whether the coronavirus ushers in a fiscal reckoning for Canadians, or somehow we sidestep the worst of the crisis through quick action and nimble minds remains to be seen. But how much easier would life be for all had politicians adopted a more hostile stance to Airbnb pushing into the traditional rental markets? Had investors not eagerly dumped savings into condo developments, and had banks been more willing to question the wisdom of lending into what most acknowledged was a real estate bubble.

In December I wrote that the Canadian insolvency rate was the highest it had been in a decade. The city of Toronto recently took action to curb the growth of payday advance loan businesses, as though the problem was the businesses and not people in general need of credit to make ends meet. Whatever is coming in the wake of the COVID-19 shutdown, the issue long predates it. And if insolvencies go up and, for the first time in a long time, a portion of the Canadian real estate sector comes under real pressure there will be a lot of finger pointing at the individuals who have over extended themselves with an illiquid pool of investments. But the truth will be that this problem will have had many facilitators; enablers that were happy to ignore the problem, even help grow it, because they didn’t want to believe that things could go wrong or didn’t see it was their responsibility curb its malignancy.

Information in this commentary is for informational purposes only and not meant to be personalized investment advice. The content has been prepared by Adrian Walker from sources believed to be accurate. The opinions expressed are of the author and do not necessarily represent those of ACPI.

A series of bad days, a moment of respite, and then more selling. This was the story of 2008, and it lasted for months. The rout lasted until finally investors felt that enough was going to be done to save the economy that people stopped selling. Massive quantitative easing, an interest rate at 0%, aggressive fund transfers, bailouts to whole industries, and the election of a president who seemed to embody the idea of “hyper competence”. That’s what it took to save the economy in 2008. Big money, an unconditional promise to save businesses and people, and the rejection of a political party that oversaw the bungled early handling of a crisis and had lost the public confidence.

I don’t think Donald Trump has never had been viewed as hyper competent. I doubt even his most ardent supporters see him as incredibly clever, but instead a thumb in the eye of “elites” who have never cared to take their concerns seriously, and to an establishment that seemed incapable of making politics work. Trump was a rejection of the status quo and a “disruptor in chief”. A TV game show host who played the role of America’s most sacrosanct character, the self made man, asked now to play the same role in politics.

There’s nothing I need to cover here you don’t already know. A history of bad business dealings, likely foreign collusion to win an election, surrounded by sycophants and yes men with little interest or understanding of the machines they have been put in charge of, and an endless supply of criminal charges. Like a dictator his closest advisors are members of his own family, and perhaps more shockingly he fawns over and publicly admires the dedications of respect other dictators get from their oppressed populations. Never has a person been so naked in their desires and shortfalls as Donald Trump.

Markets have played along with this charade because Trump seemed, if anything, largely harmless to them. Indifference to the larger operation of the government and the laser like focus on reduced regulations and tax cuts made Trump agreeable to the Wall Street set. If he could simply avoid a war and keep the economy humming, Trump was a liveable consequence of “good times”. Until the coronavirus issue, Trump had not done terribly. The economy wasn’t exactly humming. It had a bad limp due to a trade war with China. It had a chest cold because wealth inequality was continuing to worsen despite decreasing unemployment. And its general faculties were diminished as issues around health care, deficit spending, and other aspects of the society began to languish. But as far as unhealthy bodies go, the American economy still had its ever strong beating heart, the American consumer.

Today, @realdonaldtrump said: “I’ve always known this is a pandemic. I’ve felt that it was a pandemic long before it was called a pandemic … I’ve always viewed it as serious.”

Whatever name you prefer; COVID-19, the coronavirus, SARS-CoV-2, or the #Chinesevirus (as Trump is now busy trying to get it renamed) has exposed the fault lines in the administration and the danger of such blinkered thinking by Wall Street. Having spent the last few weeks downplaying the severity of the outbreak and hoping China would be able to contain it, until finally, grudgingly, acknowledging its seriousness. Markets have suddenly come face to face with a problem that bluster and bravado can’t fix. Trump is a political liability for markets, and his leadership style, which is heavy on cashing in on good times with little management for rainy days, means that markets may not really have any faith that he can properly address these problems.

Other efforts to calm markets, largely through the federal reserve, have not reassured anyone. Two emergency rate cuts are not going to fix the economy but did spook investors globally (it did signal to banks that they should take loans to cover potential shortfalls). The promise of a massive set of repo loans to provide liquidity will keep markets open and lubricated, but again won’t save jobs and won’t prop up the physical economy. What will fix markets is an end to the pandemic, a problem with the very blunt solutions of “social distancing”, “self isolation” and the distant hope of a vaccine.

What investors are facing are three big problems. First, that we don’t know when the virus will be contained. Optimistically it could be a month. Realistically it could be three. Pessimistically people are talking about the rest of the year. Even under the best conditions we are also likely facing a recession in most parts of the globe, and even then stimulus spending and financial help won’t be as effective until people can leave their homes and partake in the wider market (postponing tax filings and allowing deferrals on mortgages are good policies for right now, but at some point we need to spend money on things). But the last problem is one of politics. The Trump administration is uniquely incompetent, has shown little interest in the mechanisms of government, and in a particularly vicious form of having something come back to bite you, dismantled the CDC’s pandemic response team.

The best news came last week, when it seemed a switch had been flicked and the general population suddenly grasped the urgency of the situation and people began self isolating and limiting social engagements (I am now discounting Florida from this statement). Those measures have only been strengthened by government action over the last few days. Similarly, while I write this, Trudeau has announced a comprehensive financial package to come to the aid of small businesses and Canadian families. All this is welcome news, and I expect to see more like this over the coming weeks as Western governments take a more robust and wide ranging response to the crisis. So there is just one issue still unaddressed. The political mess in Washington.

I can’t say that markets will improve if Trump is voted out of office, but its hard to imagine that they could be made worse by his exit. Markets, and the investors that drive them, are emotional and it is confidence, the belief that things will be better tomorrow, that allow people to invest. Trump promised a return to “good times”, to Make America Great Again, and it is his unique failings that have left it, if anything, poorer.

Information in this commentary is for informational purposes only and not meant to be personalized investment advice. The content has been prepared by Adrian Walker from sources believed to be accurate. The opinions expressed are of the author and do not necessarily represent those of ACPI.

*A quick note – next week I will be discussing the recent market events, but had this written already last week and didn’t want it to go to waste.

** Performance numbers presented here all come from Questrade’s own website. They also represent the most recent numbers available.

Questrade is Canada’s fastest growing online advisory service that has built its business on the back of a catchy refrain: “Retire up to 30% richer”. There ads are everywhere and the simple and straightforward message has landed with a punch. The principle behind their slogan is that, over enough time, the amount of money you can save in fees by transferring to their online platform can be worth a substantial amount when that saved money is able to compound.

Competing on the price of financial advice has become common place, especially as people have become increasingly comfortable doing more online. Online “robo-advisors” dispense with all that pesky one-on-one business through your bank and have focused on providing the essentials of financial planning with a comfortable interface. Champions of lowering the costs of investing have hailed the arrival of companies like Questrade and Wealth Simple, believing that they would unsure in an era of low-cost financial advice.

Such a time has yet to materialize. For one thing, traditional providers of investments, like mutual fund companies, have learned to compete heavily in price, while an abundance of comparable low-cost investment solutions have given financial advisors a wider range of investments to choose from while being mindful of cost. Meanwhile, because internet companies have a business model called “scaling” which encourages corporations to rapidly expand on the backs of investors before they become profitable, its not clear whether robo-advisors are actually all that successful. Wealthsimple, one of the earliest and most prominent such services has broadened their business to include actual advisors meeting actual people, a decidedly more retrograde approach in the digital age.

Nevertheless, efforts to win over Canadians to these low cost model continue apace, and the market leader today is Questrade. So, what should investors make out of Questrade’s signature line? Can they really retire 30% richer?

Probably not.

First we should understand the mechanics of the claim. Looking through Questrade’s website we can see through their disclaimers that for each of their own portfolios they have taken the average five year returns for categories that align with each portfolio, the average fees for those categories and added back the difference in the costs. So, for their Balanced Portfolio they refer to the “Global Neutral Balanced Category” and the five-year number associated with that group of funds (the numbers seem to be drawn from Morningstar, the independent research firm that tracks stocks, mutual funds and ETFs).

Thus, they arrive at an assumed ROR of 6.21% for five years, and then project that number into the future for the next 30 years. They also calculate the fee of 2.22% (the average for the category) and subtract that from the returns. And using those assumptions Questrade isn’t wrong. Assuming you received the average return and saved the difference in fees, over 30 years you’d be 30% richer.

Except you probably wouldn’t.

Questrade actually already has a five year performance history on their existing investments, and we can go and check to see how well they’ve actually done. Unfortunately for Questrade, their actual performance in practice is not considerably better than the average return against the categories they are comparing. For the last five years, Questrade’s 5 year annualized performance is 4.92%, less than 0.3% better than the category average of 4.66%.

Keep in mind that Questrade’s secret sauce is not the intention to outperform markets, merely to get the average return and make up the difference in fees, but when put into practice it isn’t even 1%, let alone 2% ahead of their average competitors. In fact, we could go so far as to say the Questrade is a worse than average performersince if we assumed the same fees were to apply, Questrade’s performance would be significantly below the average return. In fact, for the purposes of their own history the above performance is shown GROSS of fees. Yes, if you read the fine print you discover that Questrade has not deducted its own management costs from these returns, meaning that the real rate of return would be 4.54%, officially below the average they are trying to beat!

Figure 4 This has been taken from Morningstar and compares the B Series Fidelity Global Balanced Portfolio performance against its category, Global Neutral Balanced. Performance for the individual fund is better than the 5 year average of Questrade’s comparable investment, and ahead of the five year average for the category of 4.66%. This should not be construed as an endorsement of Fidelity or any investment they have.

There is a temptation towards smugness and finger wagging, but I think its more important to ask the question “Why is this the case?” The argument for passive index ETFs has been made repeatedly, and its argument makes intuitive sense. Getting the market returns at a low price has shown to beat active management over some time periods. So why would Questrade underperform, particularly when markets have been relatively stable and trending up? I have my theories, but it should really be incumbent on Questrade to explain itself. What does stand out about this situation is that if you are unhappy with your performance THERE IS NOTHING YOU CAN DO ABOUT IT! Questrade’s portfolios represent their best mix, and do not allow you to make substitutions or even really get an explanation for the under-performance. The trade off in low cost alternatives is all the personalization, flexibility and face to face conversations that underpin the traditional advisor client relationship.

Given all the regulations that surround investing, I remain surprised that Questrade is able to advertise a hypothetical return completely detached from their actual returns, but that is yet another question that should be settled by people who are not me. Questrade has some benefits, not least is their low fees, but investors should be honest with themselves about how beneficial low fees are in a world when there are many options and the cost of navigating those options represents their best chance at retiring happy and secure.

As always, if you have questions, need some guidance or just a second opinion, please contact me directly at adrian@walkerwealthmgmt.com

Information in this commentary is for informational purposes only and not meant to be personalized investment advice. The content has been prepared by Adrian Walker from sources believed to be accurate. The opinions expressed are of the author and do not necessarily represent those of ACPI.

Late last week markets began to take the novel corona virus very seriously, and returns started to walk back from the all time highs earlier in the month. That retreat accelerated this week as COVID-19 virus fears exploded and the potential of a wide ranging global pandemic seemed possible despite the enormous efforts of the Chinese to quarantine and contain the virus. In South Korea, Italy, Iran, Japan, Canada and the United States the virus has appeared in varying states of severity, and are sparking varying degrees of public health responses.

COVID-19 strikes me as a black swan event, an unpredictable outlier that can’t really be planned for. An “unknown unknown”. Governments have plans in place to deal with epidemics, and learn from past outbreaks, but can’t plan for a virus they don’t know about and proves to be better than the precautionary measures already established to contain such events. In the instance of COVID-19, the virus seems very virulent, spreading rapidly but also having a long incubation time. You may not show any signs of the virus, and, in a cruel twist, many people with the disease may only have mild symptoms, making it easily confused with the common cold and less likely for an infected person to seek treatment while being an effective transmitter.

The Dow Jones Industrial Average over the last month.

Markets have capitulated to the fear that this virus is dangerous and will have an outsized impact on the global economy, already in a much weaker state than market returns suggested. But like all black swans what happens next will determine how serious it becomes. For my own part I believe the virus is serious, but that the 2% mortality rate may only apply to China, and that it is likely lower with a much larger pool of diagnosed people obscuring the data. This is backed up somewhat by the much smaller number of fatalities in other countries, including Japan and South Korea. What black swans really do is expose a society’s resiliency.

But resiliency covers a wider range of issues. From an investment standpoint diversified portfolios containing a wide selection of asset classes and geographic allocations are safer because they tend to be more resilient, and not through any confusing magic. Debt, both long term and short term, erode resiliency as they eat away at your ability to respond to new problems while shackling you to existing commitments. In terms of managing the economy, interest rates are also a form of resiliency, and the ability to cut rates or raise them speaks to the strength of an economy. A cursory glance at these issues might give one pause, since Canadians have all time records of debt, and an attempt in 2018 to raise interest rates for the wider health of the economy led to a rapid sell off at the end of the year, while in 2019 central banks cut rates almost everywhere to prop up a softening global economy.

COVID-19 is a significant challenge that I believe the world is up for, but as a black swan I suspect its impact will be felt more in its economic fallout. As we move into the second quarter of the year a clearer picture will emerge at just how serious the economic impact of the virus, and efforts to contain it, really have been. Given some of the existing issues within the economy, as well as those currently being stressed by the fraying of international trade, the corona virus has the potential to push economies into recession. At which point all citizens should ask, just how resilient is my country, and just how resilient am I?

Have questions about the resiliency of your portfolio? Please feel free to give me a call or send an email.

Information in this commentary is for informational purposes only and not meant to be personalized investment advice. The content has been prepared by Adrian Walker from sources believed to be accurate. The opinions expressed are of the author and do not necessarily represent those of ACPI.

This year possibly saw Canada’s most pointless election. Though it was meant to be A VERY SERIOUS AFFAIR, the election was a gong show misleading personal attacks, the exposure of embarrassing histories and the revelation that the Prime Minister of the country couldn’t say how many times he wore blackface. Amidst all of this was the arrival of Canada’s first angry populist party under the leadership of Maxime Bernier. Bernier started his People’s Party of Canada in response to narrowly losing the leadership of the Conservative Party of Canada, in a contest that many within the party saw as rigged against him. Bernier may have agreed, and having crafted a libertarian brand as “Mad Max” thought this was the time to strike out on his own (I met Bernier during his run for leader of the CPC and was surprised at how short he was. I’m not saying that Bernier started another party due to small man syndrome, but his loss to the 6’3” Scheer may have played some roll). His party was a grab bag of disaffected curmudgeons and, unsettlingly, a number of quasi-racists who were obsessed with immigration.

The outcome of the election seemed to put Canada’s populism to rest, such as it was. A short lived attempt to start a “yellow vest” movement here, like in France, failed badly and tainted Andrew Scheer, the only politician to make overtures to various populist movements. Maxine Bernie’s party failed to win a single seat, including his own, and concerns that a populist wave was crashing down on Canada seemed unfounded. And yet shortly after the election we seemed embroiled in “WEXIT”, a nascent movement for Western Independence.

WEXIT probably won’t go anywhere, but Canada does have serious problems in the west that the much of the rest of the country seems disinterested in, and if left unaddressed could fuel years of populist outrage and self destructive behaviour. For instance, where you aware that mortgages more than 90 days in arrears in Alberta and Saskatchewan were now wildly out of step with the rest of the country?

Or that the unemployment rate among young men in Alberta had now reached 20%? For much of the last two decades Alberta has been a major engine of economic growth for the country and a source of opportunity for people across Canada. Today it has been reduced to the status of a Spain or Portugal (albeit with better financials).

In their book “Revolt on the Right: Explaining Support For The Radical Right in Britain” by Matthew Goodwin and Robert Ford, the authors note that the rise of populist UKIP party is “not primarily the result of things the mainstream parties, or their leaders, have said or done…instead, is the result of their inability to articulate, and respond to, deep-seated and long-standing social and political conflicts”.

This problem has been exasperated by an increasing focus on middle-class swing voters who have become seen as central to political success compared to people who have been considered “left behind” in a political and economic sense. They go on to point out that the major parties have “avoided high-profile efforts to mobilize the concerns of the ‘left behind’ voters because both parties have concluded, that electoral success or failure will depend on the support of educated middle-class voters, who hold a very different set of values and priorities.”

This rings particularly true where the priorities of Alberta have be seen to be dismissed by the federal government (despite the acquisition of a pipeline) which has rushed to the aid of an Oshawa car plant and was so embroiled in helping SNC Lavalin it led to a damaging scandal. Over the last two elections Alberta looks increasingly isolated, a sea of blue in a country of red, more politically hegemonic and less diverse than the rest of the country, single-mindedly focused on one industry to the detriment of everything else. For its part Alberta feels under siege, suspicious of political parties that would sacrifice their economic future for environmental priorities they now regard as suspect.

In an article for The Atlantic in January of 2018, David Frum notes that “If conservatives become convinced that they cannot win democratically, they will not abandon conservatism. They will reject democracy.” The situation isn’t quite that dire for Western Canada, but I think that if political parties cannot learn to articulate and respond to deep seated social and political conflicts in Canada, western Canadians will not abandon their own self interests, but they might abandon some of the tenants of confederation.

Over the last few years the rise of populism has frequently been treated like some kind of fever waiting to break, or a tide that must eventually recede. From a political standpoint this makes some sense, as political historian Richard Hofstander had noted about third parties in the US; “challenger parties are like bees: once they have stung the system they quickly die.” But political upheavals and realignments do happen, and with Brexit now almost a certainty and confidence growing that Trump may win a reelection despite impeachment our recession of democracy may be more prolonged than we’d like to believe.

As most people have noted our current situation has a great deal to do with the events of 2008, which a decade on has left a lasting economic impression on society. Canada sidestepped the worst of 2008 and has enjoyed relative economic strength and political stability. Mostly. But with Canadians being one of the most indebted within the OECD, its worth asking the question what will the rest of Canada look like if we face a serious economic crisis? Will the words “peace, order and good governance” still define the country, or will we awaken a more politically agitated populace? One that has less tolerance for slow and steady results and is far less kind to politicians that seem incapable of addressing major issues?

Many populists already exist in our politics. Issues around education, housing and debt remain hot buttons for the electorate. And yet our last election spent far more time focused on a speech by Andrew Scheer from over a decade ago. Does that seem like a political class articulating and responding to long standing and deep seated issues, or one that has learned to master the art of getting elected? Education costs continue to climb and yet the return to students is considerably lower, and prospects much worse for those with only high school diplomas. Debt in Canada has continued to rise, a story that seems evergreen, but insolvencies have also started climbing. Currently insolvencies remain low overall, but given the large amount of Canadian debt, what might it take to push people over the edge? Which politician can honestly say they’ve got a good plan to deal with these problems?

So, is the populist tide turning? I think it is too early for us to say, and Canadians should be wary of people arguing that Alberta’s WEXIT is a silly tantrum. Instead we should watch with a cautious eye towards the West. Where Alberta goes we may well follow.

Information in this commentary is for informational purposes only and not meant to be personalized investment advice. The content has been prepared by Adrian Walker from sources believed to be accurate. The opinions expressed are of the author and do not necessarily represent those of ACPI.

Launched to much derision and the collective snort of Canada’s journalist class, the government introduced a new cabinet position, “Minister of Middle-Class Prosperity”. Shockingly the new minister seemed incapable of defining what the middle class actually is, and in an effort to clarify her earlier non-position, went on TV to describe understanding the middle class as different things to different people that needs to be viewed through different lenses.

This answer, such as it was, was uniquely terrible since any applied thought to the question of “middle class prosperity” should yield several interesting ideas that deserve close examination.

For instance, an office focused on middle class prosperity might provide a useful take on inflation in terms of how it affects the middle class. Rather than relying on the aggregate rate that economists talk about at national levels, some clarity might come in about where that inflation is felt, like in housing, child rearing and education. We might also find something useful to say about savings and retirement, both of which are going to be increasingly serious questions into the very near future.

But let’s start with the basics. What is a middle class? First, the middle class is a result of an industrialized society. Though there is evidence of times of improving and deteriorating living conditions for humans in our pre-industrialized past, sustained and persistent improvements in living standards exist as a result of industrialization. This is not just because people got richer (and skills became more specialized) but because the cost of things dropped.

This really picked up steam after the Second World War when Western nations went toe to toe with Soviet command economies and showed, despite all their inequality, that more prosperity for more people came about as a result greater innovation in production in the pursuit of reducing prices. Yes, many people had good jobs, but luxury items like refrigerators, dishwashers, and microwaves all became standard kitchen appliances, as did (in time) TVs, cell phones and computers because prices for those items have been in free fall since the 1950s.

If we are looking for a definition of the middle class we could do worse than something along these lines: “The middle class represents a working sector of our society that is sufficiently monetarily rewarded to save for future financial stability, retains ample discretionary income in the present, and can reasonably aspire to help their future generations.” Threats to the middle class, both to people trying to enter it and to those trying to maintain their status within it, come from the erosion of the cost effectiveness of certain services. Housing, education and long retirements threaten this class of people and some of their ills are obscured by how we understand and talk about the economy.

Consider for instance why we talk so much about taxes. Taxes represent one of the few and very clear levers that a government can pull to change personal finances. They can take less money, or they can take more. As of this week the Liberal government has promised another “middle class tax cut” that should leave an average middle class Canadian $300 richer every year, or $600 for a family. Not bad, and for an individual that works out to being 25% of one month’s rent in Toronto for a single bedroom (average) or three weeks of groceries for the average Canadian family! If you are struggling as a Canadian family despite two good jobs, its hard to imagine that this will make or break a retirement or fund a university tuition.

In a survey done by BDO, 2047 Canadians were asked about their personal finances. The results were less than encouraging. 57% were carrying credit card debt and a third couldn’t pay off their short-term credit. 39% said they had no savings for retirement and 69% said they didn’t have enough savings to get through retirement. These findings match repeated surveys and studies done over the past decade that continue to suggest that Canadians are simply not saving enough and are drowning in debt.

Small tax cuts seem unlikely to fix problems that look like this, and I think its important to note that solutions to these problems are not readily apparent. It should also be noted that being middle class should not mean that you are always financially whole and never struggle. Part of the reason that the middle class has financial issues is because it strives for a life above mere subsistence. Its goals are materially aspirational, and people live their lives according to that aspiration.

A more productive focus should be on helping people enter the middle class. Far too much energy has been dedicated to using houses to boost middle class wealth, both through restricting development to preserve neighbourhoods, and relying on the equity within homes to boost standards of living. This is the wrong place to hoard wealth and it should be replaced with more aggressive home development within cities to boost density, improve services, and reduce the price of homes. Just as importantly the role of higher education should go under a microscope. The costs of University have jumped as more Canadians get degrees and those degrees are worth less in the market. Canadian parents regularly save for children’s education, to the detriment of their retirement savings. The cost of that education is expected to be over $120,000 for a four year degree very soon. Attacking the issue of education head-on would be an enormous help in easing access to middle class security.

Lastly, dealing with debt should be a priority. Lending should have tighter restrictions, especially for younger Canadians in their early 20s when their financial needs are lower, and a state run bank set up to help Canadians get out of debt (the use of which should preclude any other financial lending) would be an enormous asset in terms of allowing Canadians get on going debt help and learn to better manage budgets and connect people to financial help.

Far from having little idea of what constitutes the middle class, we are, if anything, too certain of what a middle-class life looks like and the path to getting there. This is a moment when we should be experimenting with how we create a growing middle class, not calcifying a particular version of life that no longer fits a world that has dramatically changed since the 1950s. A minister for “Middle Class Prosperity” need not be a pointless fluff position making vague pronouncements. Instead it could be a cabinet position that spearheads exciting new ways to improve access to financial security and create paths to long term growth.

Information in this commentary is for informational purposes only and not meant to be personalized investment advice. The content has been prepared by Adrian Walker from sources believed to be accurate. The opinions expressed are of the author and do not necessarily represent those of ACPI.

His party was a grab bag of disaffected curmudgeons and, unsettlingly, a number of quasi-racists who were obsessed with immigration.

His party was a grab bag of disaffected curmudgeons and, unsettlingly, a number of quasi-racists who were obsessed with immigration.

In their book “Revolt on the Right: Explaining Support For The Radical Right in Britain” by Matthew Goodwin and Robert Ford, the authors note that the rise of populist UKIP party is “not primarily the result of things the mainstream parties, or their leaders, have said or done…instead, is the result of their inability to articulate, and respond to, deep-seated and long-standing social and political conflicts”.

In their book “Revolt on the Right: Explaining Support For The Radical Right in Britain” by Matthew Goodwin and Robert Ford, the authors note that the rise of populist UKIP party is “not primarily the result of things the mainstream parties, or their leaders, have said or done…instead, is the result of their inability to articulate, and respond to, deep-seated and long-standing social and political conflicts”.

Many populists already exist in our politics. Issues around education, housing and debt remain hot buttons for the electorate. And yet our last election spent far more time focused on a speech by Andrew Scheer from over a decade ago. Does that seem like a political class articulating and responding to long standing and deep seated issues, or one that has learned to master the art of getting elected? Education costs continue to climb and yet the return to students is considerably lower, and prospects much worse for those with only high school diplomas. Debt in Canada has continued to rise, a story that seems evergreen, but insolvencies have also started climbing. Currently insolvencies remain low overall, but given the large amount of Canadian debt, what might it take to push people over the edge? Which politician can honestly say they’ve got a good plan to deal with these problems?

Many populists already exist in our politics. Issues around education, housing and debt remain hot buttons for the electorate. And yet our last election spent far more time focused on a speech by Andrew Scheer from over a decade ago. Does that seem like a political class articulating and responding to long standing and deep seated issues, or one that has learned to master the art of getting elected? Education costs continue to climb and yet the return to students is considerably lower, and prospects much worse for those with only high school diplomas. Debt in Canada has continued to rise, a story that seems evergreen, but insolvencies have also started climbing. Currently insolvencies remain low overall, but given the large amount of Canadian debt, what might it take to push people over the edge? Which politician can honestly say they’ve got a good plan to deal with these problems?