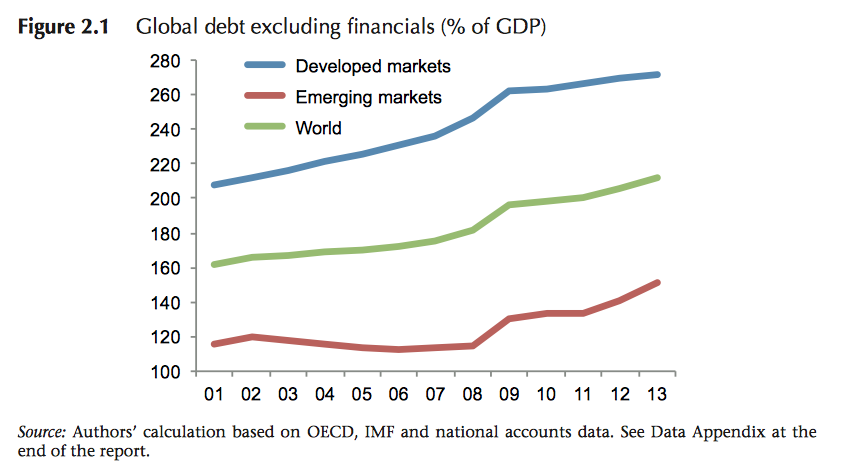

Yesterday the 16th Geneva Report was released bearing bad news for everybody that was hoping for good news. The report, which highlighted that debt across the planet had continued to increase and speed up despite the market crash of 2008, is sobering and seemed to cast in stone that which we already knew; that the global recovery is slow going and still looks very anemic.

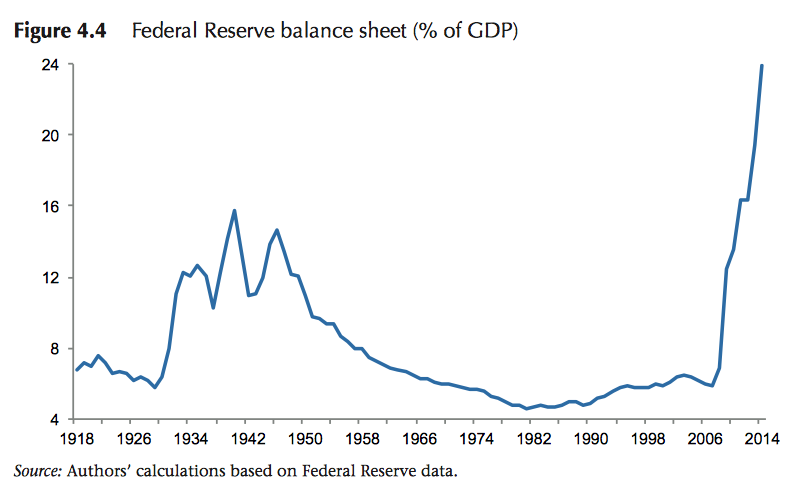

The report is detailed and well over a hundred pages and only came out yesterday, so don’t be surprised if all the news reports you read about it really only cover the first two chapters and the executive summary. What is interesting about the report is how little of it we didn’t know. Much of what the report covers (and in great detail at that) is that the Eurozone is still weak, that the Federal Reserve has lots of debt on its balance sheets, but that it has helped turn the US

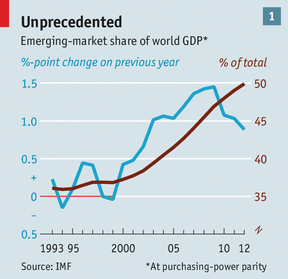

economy around, that governments have been borrowing more while companies and individuals borrow less, and that economic growth in the Emerging Markets has been accompanied by considerable borrowing. All of this we knew.

What stands out to me in this report are two things that I believe should matter to Canadian investors. First is the trouble with low interest rates. Governments are being forced to keep interest rates low, and they are doing that because raising rates usually means less economic growth. But as growth rates have been weak, nobody wants to raise rates. This leads to a Catch-22 where governments are having to take direct measures to curb borrowing because rates are low, because they can’t raise rates to curb borrowing.

This has already happened in Canada, where the Bank of Canada’s low lending rate has helped keep housing prices high, mortgage rates down and debt levels soaring. To combat this the government has attempted to change the minimal borrowing requirements for homes, but it hasn’t done much to curb the growing concern that there is a housing bubble.

The second is the idea of “Economic Miracles” which tend to be wildly overblown and inevitably lead to the same economic mess of overly enthusiastic investors dumping increasingly dangerous amounts of money into economies that don’t deserve it just to watch the whole thing come crashing down. Economic miracles include everything from Tulip Bulbs and South Sea Bubbles to the “Spanish Miracle” and “Asian Tigers”, all of which ended badly.

The rise of the BRIC nations and the recent focus on the Frontier Markets should invite some of the same scrutiny, as overly-eager investors begin trying to fuel growth in Emerging Markets through lending and direct investment, even in the face of some concerning realities. It’s telling that the Financial Times reported both the Geneva Report on the same day that the London Stock Exchange was looking to pursue more African company listings, even as corruption and corporate governance come into serious question.

All of this should not dissuade investors from the markets, but it should be seen as a reminder about the benefits of diversification and it’s importance in a portfolio. It is often tempting to let bad news ruin an investment plan, but as is so often the case emotional investing is bad investing.

I’ve added an investment piece from CI Investments which has been floating around for years. It pairs the level of the Dow Jones Industrial Average with whatever bad news was dominating the market that year. It’s a good way to look at how doom and gloom rarely had much to do with how the market ultimately performed. Have a look by kicking the link! I don’t want to Invest Flyer

***I’ve just seen that the Globe and Mail has reported on the Geneva Report with the tweet “Are we on the verge of another financial crisis” which is not really what the report outlines.