Markets have reached six or seven week highs, (HIGHS I say!) and questions are arising as to whether this represents a sustained recovery.

Markets have reached six or seven week highs, (HIGHS I say!) and questions are arising as to whether this represents a sustained recovery.

The crystal ball is decidedly opaque on that question, not simply because there is an abundance of conflicting data, but because more of it is produced everyday. Add to that the fact that the “mood” often dictates much of the day’s trading, plus the often counter-intuitive reality that sometimes sufficiently bad news is considered good news in its own right.

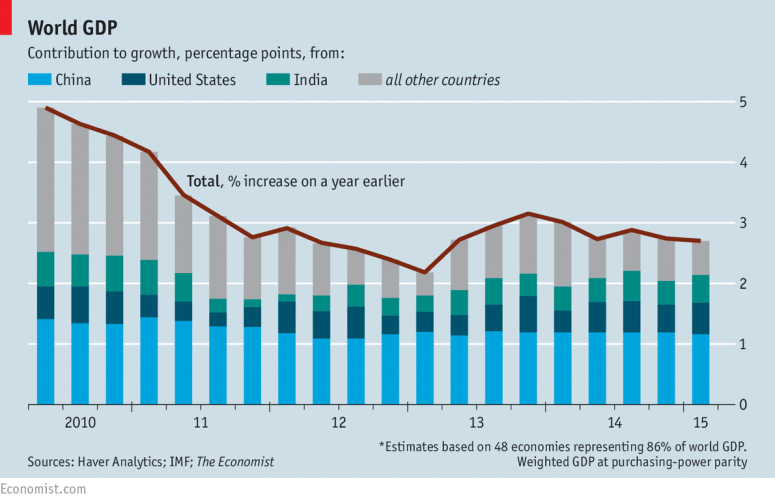

Take for example China’s financial woes. China’s economy is definitely slowing, and the tools used in the past to spur Chinese growth are no longer useful in the same way. To summarize, the Chinese economy got big by building big things; cities, ports, factories, and other big infrastructure to facilitate its role as a manufacturer to the world. In turn the world sold China many of the resources needed to do that. Now the Chinese are up their eyeballs in highways and empty cities they must “transition” to a service economy, essentially an economy that now serves its people rather than the rest of the planet.

Such a transition is no easy thing, and to the best of my knowledge there is no law that says the Chinese government is somehow more adept at managing such a transition. But every bit of bad news may either make investors nervous, or give them hope that the Chinese government may be encouraged to do more economic stimulus. Moody’s, the ratings agency, recently downgraded their outlook on Chinese debt from stable to negative, and downgraded their credit rating. The market’s response?

That big jump is after they received the downgrade! We see similar patterns out of Europe and the United States. Raising US interest rates has been widely decried by various financial types and talking heads, urging the Federal reserve chairman Janet Yellen to either reverse, stop or even consider negative rates to help the economy. Why such panicked response? Because it has become a common thought that raising rates is now more damaging that the requirement of lowering them!

This has less to do though with distortions in the market and more to do with people trying to accurately read and project from various data points, even when many of those reports conflict. In the short term the abundance of conflicting news creates a blind men and the elephant relationship between investors and economies. Everybody is feeling their way around but all coming back with wildly different descriptions of what is happening.

What we do know is that there are some big problems in the markets and economies, and the threat of a global recession is very real. What day traders and analysts are looking for is confirmation on whether this threat is easing or not. So, if we suddenly read that managers see a contraction in oil production we might see a sudden rise in the value of crude oil. That news has to be weighed against that fact that global oil supply is still growing, and whether it still makes sense to price oil by its available supply, or against its expected future reduced production.

And that is the challenge. Big problems take time to sort out, and in the intervening period as they are addressed the blind men of the markets make lots of little moves trying to bet on early outcomes, attempting to assess the correct value of a thing often before a clear picture is actually there. For investors the message is to be cautious, both in making large bets or by trying to avoid risk all together. It is a mantra here in our office on the benefits of diversification and risk management, precisely because it reminds us to hold positions even when the mood has soured greatly, and shy away from investments that have become too popular. The goal of investors should to not be one of the blind men, guessing about what they touch, but to make irrelevant that shape of the markets altogether.

Since 2008 governments the world over have tried to fight the biggest banking collapse since the great depression with modest success. Eight years on and you would be loath to say that the world has turned a corner, ushering in a return of unrestrained economic growth.

Since 2008 governments the world over have tried to fight the biggest banking collapse since the great depression with modest success. Eight years on and you would be loath to say that the world has turned a corner, ushering in a return of unrestrained economic growth.