Since I first wrote about the Ukraine much has happened. Russia has been unmasked as a bizarre cartoon villain seemingly hellbent on destabilizing the Ukrainian government, assisting “rebels” and being indirectly responsible for the murder of a plane full of people. All of which came to a head last week when it appeared that Russia might have just started a war with the Ukraine (still somewhat indeterminate).

Since I first wrote about the Ukraine much has happened. Russia has been unmasked as a bizarre cartoon villain seemingly hellbent on destabilizing the Ukrainian government, assisting “rebels” and being indirectly responsible for the murder of a plane full of people. All of which came to a head last week when it appeared that Russia might have just started a war with the Ukraine (still somewhat indeterminate).

Russia’s moves with the Ukraine may have more to do with challenging the West, and some of the other recent militaristic actions show that may be its real intent. Russia announced in July that it would be reopening both an arctic naval base and a listening post in Cuba built back in the 1960s. Combined with many heavy handed tactics at home including essentially banning homosexuality, Putin is making a brazen attempt to assert its regional dominance and stem the growth of Europe’s influence in the most aggressive way it can. To some extent this seems to be working with his own population, but it isn’t making him popular globally.

Europe’s response to Russia has been to hurt it with economic sanctions, which since the Ukrainian situation first began have been escalating in severity. Two weeks ago Russia responded in kind. How? By banning food imports from sanctioning nations.

If you don’t know much about the Russian or European economies this may seem like potent response from one of the BRIC countries and major global economies. But Europe is a big economy, and agricultural exports don’t make up a significant part of GDP, with the same being true for the United States. And while sanctions targeted at farms can be politically dangerous (farmers are typically a well organized and vocal lobby) the most interesting thing about these sanctions is what it tells us about the Russian and European economies respectively.

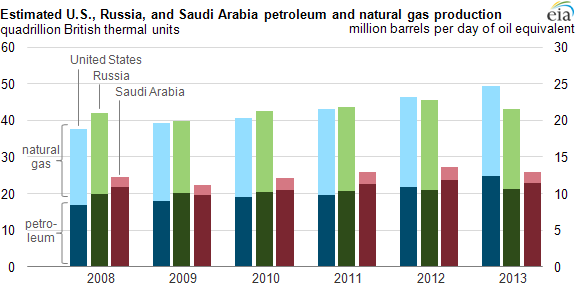

First, Russia imports a great deal of food, mostly from Denmark, Germany, the United States and Canada. So sanctions imposed by Russia are really going to hurt the Russians as food prices begin to rise and new food suppliers (expected to be from Latin America) have to ship food farther. But more interesting is the sanctions Russia chose not to impose. Europe is heavily dependant on oil & gas for its energy needs. So why not really make Europe feel the pinch and create an energy crisis? Because Russia needs oil revenue.

16% of Russia’s GDP is made up from the oil and gas sector. Beyond that oil and gas make up more than half of Russia’s tax revenues and 70% of it’s exports. In other words Russia can’t stop selling its oil without creating an economic crisis at home every bit as severe as in Europe. Banning imports of food and raising the cost of living may not be the ideal outcome from sanctions you impose, but it is mild in comparison to creating a full on catastrophe.

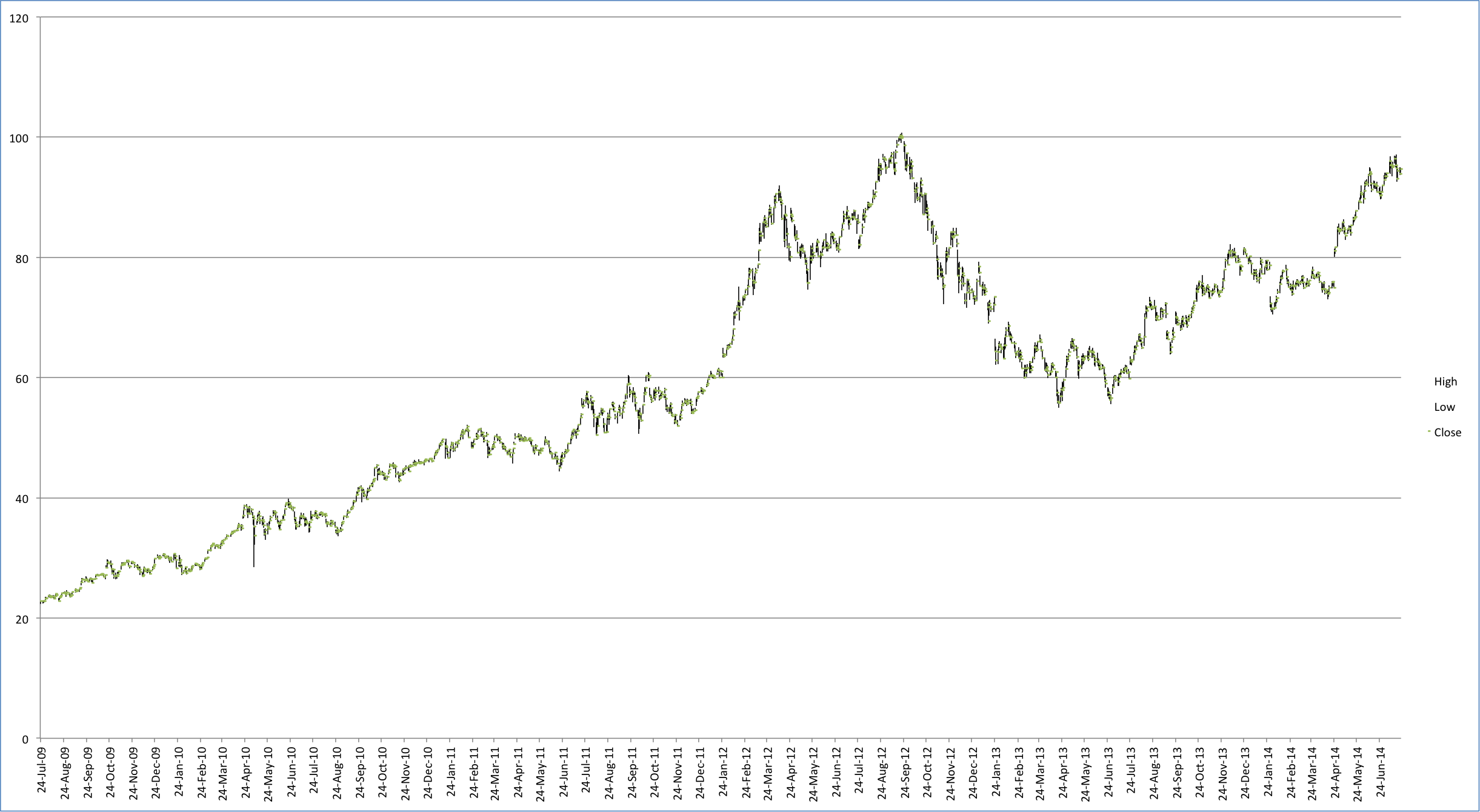

By comparison Europe starts to look very good, and it’s a reason that investors shouldn’t be quick to write off Europe and all its recent economic troubles. It’s a large and dynamic economy, filled with multi-national companies that do business the world over. It is backed by stable democracies and a relatively prosperous citizenry. By comparison Russia is a very narrow economy, dependent on one sector for its economic strength run by a (in all but name) dictator with an incredibly poor populace. A few years ago it was quite trendy in the business news to write off Europe as a top heavy financial mess, and while I wouldn’t want to dismiss Europe’s problems (some of which are quite serious) it’s important to have some perspective about how economies can rebound and which ones have the flexibility to recover.

That’s just its phone division. The iPad, whose sales numbers are definitely plateauing if not declining is still a valuable business netting $5.9 billion in revenues, greater than Facebook, Twitter, Yahoo, Groupon, and Tesla combined.

That’s just its phone division. The iPad, whose sales numbers are definitely plateauing if not declining is still a valuable business netting $5.9 billion in revenues, greater than Facebook, Twitter, Yahoo, Groupon, and Tesla combined.