*In an act of hubris I have written this before companies have begun releasing their earnings reports. I can only assume I will be punished by the animal spirits for such reckless predictions!

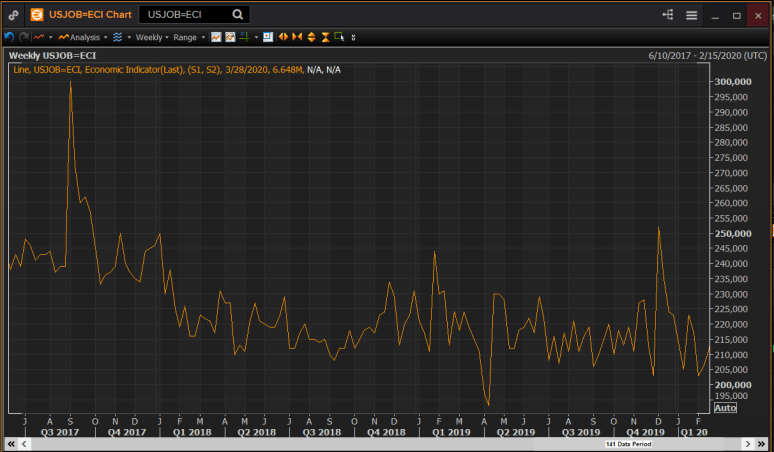

The news has been grim. The number of people seeking EI has spiked so much, so quickly that it reduces the previous unemployment numbers to a flat line (this is true in both Canada and the United States, US EI graph below). Countries remain in lockdown and some of the worst hit countries like Italy and Spain are starting to plateau, adding ONLY between 500 to 1000 deaths a day. In Canada the numbers continue to climb and the economy has been largely shut down, with governments rolling out unprecedented quantities of money to stem the worst of this. Talk of a deep economic depression has been making rounds, while the Prime Minister has reluctantly suggested that we may be in a restricted environment until July.

And yet.

And yet.

And yet, I suspect we may be too negative in our outlook.

First, just how restricted is the economy? Despite the wide-ranging efforts to restrict the social interaction that daily economic activity produces, much of the economy continues to function. Office and white-collar jobs have quickly adapted to remote working. Few have been laid off in that respect. Industrial production is down, unless they are deemed essential, but the essential label has applied to a lot of businesses. Until the recent additional restrictions applied on Sunday April 5, 2020 in Ontario, Best Buy, Canadian Tire, Home Depot and a number of other stores remained open to the public. Those businesses have had to restrict access to their stores, but remain functioning through curb pick and online delivery.

Even the service economy is still largely functioning. Most restaurants remain open providing take out and delivery. Coffee shops, gas stations, grocery stores, convenience stores are all open, as are local grocery providers like butchers and bakers (and candle stick makers). Its’ true that large retail spaces like Yorkdale or the Eaton Centre are closed but this too tells us something.

The government has helped make it easier to get money since people have been laid off, and many of the people who have been let go will only be out of work for a short time. They are the waiters, union employees and airline pilots who will be rehired when the society begins to reopen. Even in the period I began writing this, Air Canada rehired 16,500 employees, West Jet will be rehiring 6,500 employees, and Canadians applying for the new CERB (Covid-19 Emergency Response Benefit) have reportedly already begun receiving it.

You might be reading this and thinking that I’m being callous or simply ignoring the scope of the problem that we are facing, but I want to stress that I am not. I recognize just how many people have found themselves out of work, how disruptive this has been, how scared people are and how this pandemic and its response has hit the lower income earners disproportionately more. But just as few people correctly saw the scale of the impact of the coronavirus, we should remain cautious about being too certain that we can now anticipate how long the economic malaise may last, or how permanent it will likely be, and what its lasting impacts will look like.

The sectors of the economy worst hit will likely be those already suffering a negative trend line. The auto sector, for instance, is one that has been hemorrhaging money for a while, with global car sales in a serious slump. Some retail businesses, already on the ropes from Amazon’s “retail apocalypse” may find they no longer can hold on, though government aid may give them a limited second life. Hotels and travel will likely also suffer for a period as they carry a high overhead and have been entirely shut down through this process (sort of).

Longer term economic problems may come about from mortgage holders who have struggled to fulfill their financial obligations to banks, and it may take several months to see the full economic fallout from the efforts to fight the pandemic, so some of the effects may be staggered over the year.

But even if that’s the case, the current thinking is that the market must retest lows for a considerable period, with few people calling for a rapid recovery and many more calling for a “W” shape (initial recovery then a second testing of previous market lows) and in the Economist this week “one pessimistic Wall Street banker talks of a future neither v-shaped, u-shaped or even w-shaped, but ‘more like a bathtub’”.

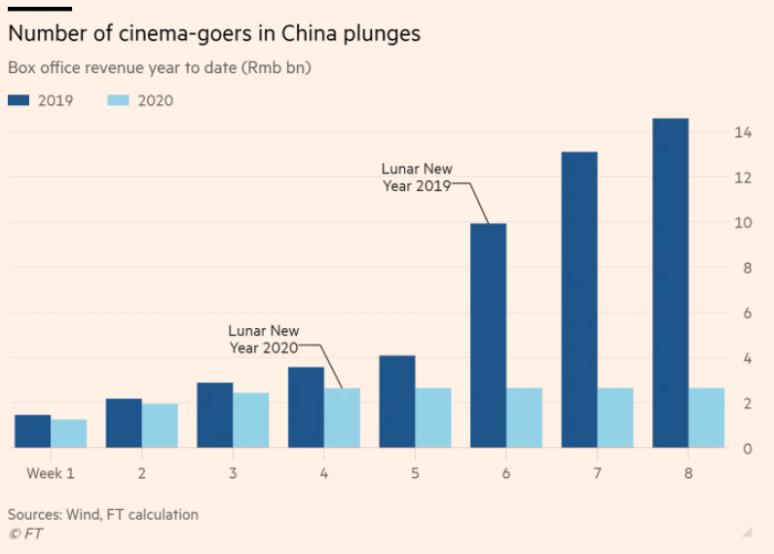

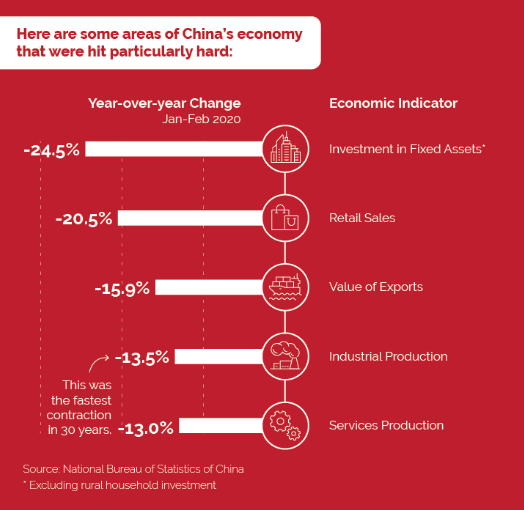

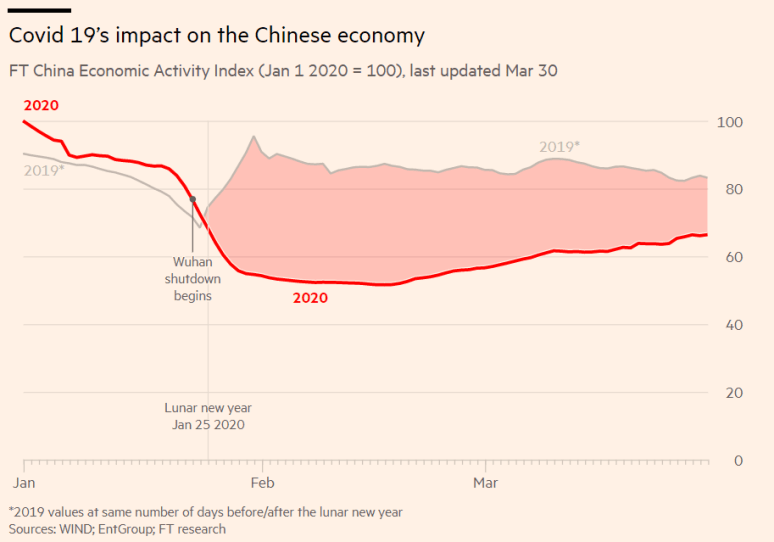

That pessimism is well warranted, and I count myself among those expecting markets to have a second dip. But I admit to having my doubts about the full scale of the impact to the real economy. There will no doubt be some fairly scary charts, like thre were from China, showing the drop off in cinema goers and people eating out. But the more certain, the more gloomy, the more despairing the outlooks get, the more I wonder if this is an over compensation for having overlooked the severity of the virus, or if it is the prevailing mood biasing these predictions? Only time will tell, but I am taking some comfort in knowing that there is still a case for the best possible case.

Information in this commentary is for informational purposes only and not meant to be personalized investment advice. The content has been prepared by Adrian Walker from sources believed to be accurate. The opinions expressed are of the author and do not necessarily represent those of ACPI.

If there was ever going to be a moment to gain some clarity about what the Brexit would truly and ultimately mean, Friday was the day. Following the win by the leave camp, markets were sent reeling on the uncertainty stirred up by the referendum, and by the day’s end Britain had gone from being the

If there was ever going to be a moment to gain some clarity about what the Brexit would truly and ultimately mean, Friday was the day. Following the win by the leave camp, markets were sent reeling on the uncertainty stirred up by the referendum, and by the day’s end Britain had gone from being the

Markets have reached six or seven week highs, (HIGHS I say!) and questions are arising as to whether this represents a sustained recovery.

Markets have reached six or seven week highs, (HIGHS I say!) and questions are arising as to whether this represents a sustained recovery.