When economists get things wrong their missteps are practically jaw dropping. Despite making themselves the presumed source of useful information about economies, interest rates and economic management, often it seems that the economists are learning with the rest of us, testing ideas under the guise of sage and knowledgable advice. Their bias is almost always positive and the choices they make can be confounding.

As an example, let us consider the case of the Bank of Canada (BoC).

If there are perennial optimists in this world they must be employed at the BoC, for no one else has ever stared more danger in the face and assumed that everything will be fine.

For those not in the know, the BoC publishes a regular document called the Financial System Review, a bi-annual breakdown of the largest threats that could undo the Canadian economy and destabilize our financial system. Because they are the biggest problems we tend to live with them over a long time and thanks to the Financial System Review we can see how these dangers are presumed to ebb and flow over time.

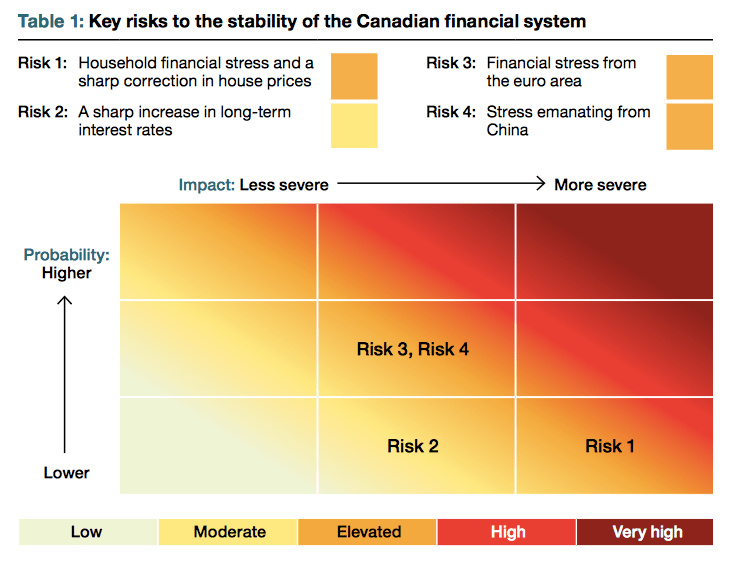

For instance, two years ago the four biggest dangers according to the BoC were:

- A sharp correction in house prices

- A sharp increase in long-term interest rates.

- Stress emanating from China and other Emerging Markets

- Financial stress from the euro area.

Helpfully the BoC doesn’t just list these problems but also provides the presumed severity and likelihood of them coming to pass and places them in a useful chart.

Here is what that chart looked like in June of 2014:

The worst risk? A Canadian housing price correction. The likelihood of that happening? very low. Meanwhile stress from the Euro area and China rate higher in terms of possibility but lower in terms of impact.

By the end of 2014 the chart looked like this:

Unchanged.

Interestingly the view from the BoC was that there was no perceivable difference in the risks to the Canadian market. Despite a Russian invasion of the Ukraine, the sudden collapse in the price of oil and the continued growth of Canadian debt, the primary threats to Canada’s economy remained unmoved.

So what changed by the time we got to mid 2015?

The June 2105 FSR helpfully let Canadians know that, presumably, threats to Canada’s economy had actually decreased, at least with regards to problems from the euro area. This is curious because at that particular moment Greece was engaged in a game of brinkmanship with Germany, the IMF and the European Bank. Though Greece would go on to technically default and then get another bailout only further kicking the can down the road, the view from the BoC was that things were better.

Interestingly the price of oil had also continued to decline in that period, and the BoC had been forced to make a surprise rate cut at the beginning of the year. Debt levels were still piling up, and there was a worrying uptick in the use of non-regulated private lenders to help get mortgages.

None of that, according to the analysts at the Bank of Canada, apparently mattered. At least not enough to move the needle.

The December 2015 FSR is now out, and if we are to take a retrospective on the year we might point to a few significant events. To begin, the economy was doing so poorly in the summer that the BoC did a second rate cut, which was followed by further news that the country had technically entered a recession (but nobody cared). Europe’s migrant crisis reached a tipping point, costing money and the risking the stability of the EU. Germany’s largest auto maker is under investigation for a serious breach in ethics and falsifying test results. China’s stock market began falling in July, and the Chinese government was forced to cut interest rates 5 times in the past year. The United States did their first rate hike, a paltry 25 bps, but even that has helped spur a big jump in the value of the US dollar. Meanwhile the Canadian dollar fell by nearly 20% by the end of 2015.

And the Bank of Canada says:

Things are better? Or not as severe?

In two years of producing these charts, despite continued worsening of the financial pictures for Canada, China, the EU and even the United States, the BoC’s view is still pretty rosy. What would it take to change any of this?

Whether they are right or not isn’t at issue. It’s the future and it is unknowable. What is at issue is how we perceive risk and how ideas about risk are communicated by the people and institutions who we trust to provide that guidance. This information is meaningless if we can’t understand its parameters and confusing if a worsening situation seems to change nothing about underlying risk.

As you read this I expect the Chinese and global markets to be performing better this morning on reassuring news about Chinese GDP. But I would ask you, has the risk dissipated or is it still there, just buried under positive news and investor relief? It’s a good question and exactly the kind that could use an honest answer from an economist.