Getting old is something that comes to us all and is rightly considered a blessing of our modern world. Free from most wars, crime and disease the average age of Canadians continues to rise, with current life expectancy just over 82 years.

But being old is no fun. From your late 70s onward quality of life begins to decline in a multitude of ways. From a media perspective we tend to focus on outliers, like the oldest marathon runner, or the oldest male model, men and women who seem to exemplify youth well past their physical. In truth though the aging process is simply a battle that we have gotten good at slowing down.

In his excellent book Being Mortal, author and practicing surgeon Atul Gawande goes through the effects of aging, the limits of science to combat it and how we could be using medicine better to improve quality of life for the elderly. It’s a great and sometimes upsetting read that I recommend for everyone.

In his excellent book Being Mortal, author and practicing surgeon Atul Gawande goes through the effects of aging, the limits of science to combat it and how we could be using medicine better to improve quality of life for the elderly. It’s a great and sometimes upsetting read that I recommend for everyone.

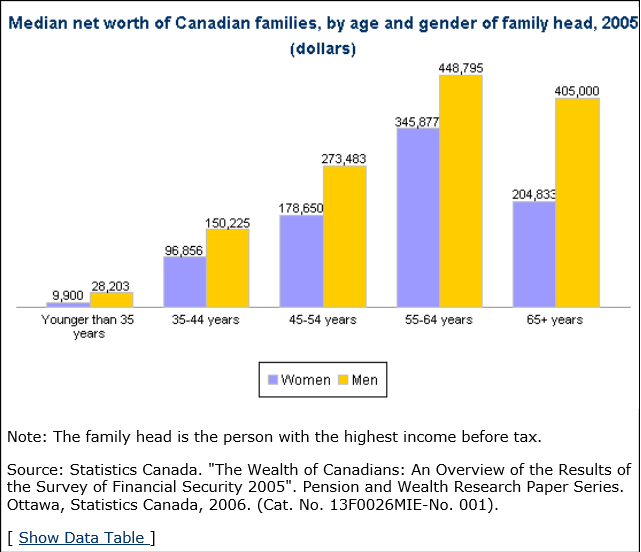

One of the great challenges that looms on the horizon is the cost of an aging population. The dependency ratio for the elderly (the metric of people over 65 against those between the working ages of 20-64) is rising, putting higher living costs on a smaller working base. In Canada the dependency ratio is expected to climb to 25% by 2050, and is currently at 23.77% as of 2015. That may not seem like much, but in 1980 (the year I was born) the ratio was 13.84%.

Since old age is also the point where you consume the most in terms of health care costs we should be aware that Canada’s population isn’t just aging, but that our retiring seniors are poised to become the biggest and most expensive demographic; financially dependent on a shrinking workforce and more economically fragile than they realize. That’s a problem that nations like Japan have been struggling with, where old age benefits are extensive, but the workforce has dwindled.

In other articles we’ve touched on the various aspects of the rising costs of old age. I’ve written about: the importance of wills, the impact of an aging population on our public health care, how demographics shift both investing patterns and warp our economic senses, why seniors may be getting too much of a break economically, how poor land management has made cities too expensive and that’s hurting retirement, and how certain trends are making retirement more expensive. Often these are written as issues in a distant (or not too distant) future. But increasingly they won’t be.

This past week eight long term care facilities have said they will be leaving Toronto. As part of a bigger project, long term care spaces are being rebuilt to meet new guidelines. A new facility is larger, more spacious and designed to maximize medical care. However land costs within Toronto are proving to be too high to be considered for the updated facilities. Why is that? The government pays $150 a day per bed in a facility like the ones leaving. From that subsidy costs for maintenance, nurses, janitors, medicine and food as well as the profit of the business must all be extracted. Margins are thin and building costs in the city are huge. Six more facilities are also considering leaving the GTA for cheaper land.

Eric Hoskins, health minister for the province, is arguing that the subsidy the government provides is enough, but he is already embroiled in other fights with the medical community. In 2015 the ministry cut doctors fees and began clawing back previously earned money as well. Currently lots of people in Ontario struggle to see their family doctor, and there are 28,000 elderly waiting to get access to long term care facilities, and only 79,000 beds. Coincidentally this is also the year that the Ontario Liberals balanced the books. Something about that should give us pause.

This is the reality of getting old in 2017. Costs are rising and are expected to continue growing. Some of this you can’t avoid, and many of us will end up in private retirement homes, assisted living situations, dependent on the government or even family. But there are steps that can be taken to protect assets and insulate against protracted medical or legal disputes.

Here’s a list of eight things that can help you with retirement and your estate:

- Keep an updated will and a named executor young enough to handle your affairs. I know it goes without saying, but its extremely important and many of us don’t do it.

- Ensure that you’ve got a Power of Attorney (POA) established and that it is current.

- Make sure you have a living will and discuss with your family your expectations about how you want your life to end.

- Look into your funeral arrangements while you can. It seems macabre, but funerals can be wildly expensive and burdensome to thrust onto grieving family.

- Create a space where all important documents can be found by your next of kin and with a detailed contact sheet so people can help settle your estate.

- Look into assisted living options early and consider what you might be able to afford. Have your financial plan reflect some of these income needs.

- Consider passing along family heirlooms early. Is there a broach, or a clock that you would like to see in someone’s hands? These conversations are easier to handle when you are well than when you aren’t, and downsizing frequently involves saying goodbye to long loved possessions.

- Big assets like houses and cottages should be discussed with family, especially if there is a large family and the assets might need to be shared. A lot of family strife comes from poor communication between generations and among siblings.

There will be much more to say about getting old, about protecting quality of life and managing the rising costs of living on fixed incomes. We gain little from sticking our heads in the sand and hoping that we will be healthy and strong to the day we die. In reality our retirement plans should better reflect not our most hopeful ideas of retirement but instead our greatest concerns and seek ways to preserve our quality of life.