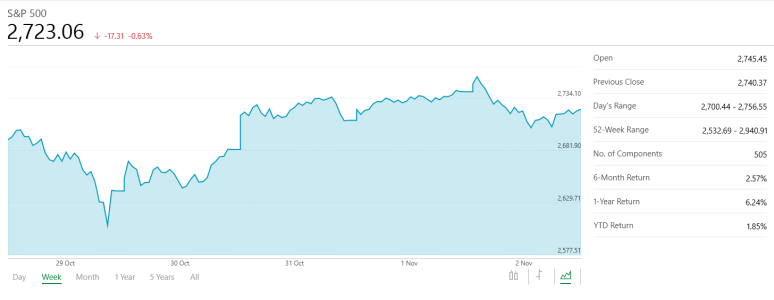

*At the time that I wrote this markets had just finished several positive sessions, however by the time it was ready markets had once again changed directions!

I’m going to potentially embarrass myself and go on the record as saying we shouldn’t place too much trust in the current market rally, though the upturn is welcomed.

Rallies present opportunities for potential short-term gain, and with markets having shed roughly 10% over the month of October, there is certainly money to be made if you’re feeling sufficiently opportunistic and have a plan. For the rest of us, the rally is a welcome break the punishment the market has been delivering, and an opportunity to see portfolios stabilize and regain some ground.

The long-term viability of a rally, its ability to transition from opportunistic buying to sustained growth, very much depends on the fundamentals of that rally. Are markets sound, but oversold? Or are fundamentals deteriorating and represents more hopefulness than anything else?

Readers of this blog will not be surprised to find out I have no set answer to this question. As always, “it depends”. But as I look over the news that has supposedly rekindled the fire in the markets much of it seems at best temporary, perhaps even fanciful. Up against the wall of risk that investors are currently starring down, the best news currently available is that Trump had a phone call with Xi Jinping and has asked for a draft to be prepared to settle the trade disputes between the two countries.

I’m of the opinion that a recession isn’t imminent, but it should be obvious that recessions happen and the longer we go without one, the more likely one becomes. That seems especially true in a world that is undergoing a seminal shift when it comes to international trade and multilateral deals. To take one example, in the last year U.S. soybean exports to China have dropped by 97%, with no exports for the last quarter. This is a trade war still in its infancy. Other market data is mixed. Even as job growth exceeds expectations it will also keep the Fed raising rates. Housing starts have dropped significantly below expectations, driven in part by rising costs.

All this is to say that market rallies like the one we’ve just seen should be treated with trepidation. Investors should be cautious that a bottom has been reached and that this is a good time to rush into the market looking for deals, and we should keep an eye on the fundamentals. Rallies falter precisely because they can be based more on hope than on reality.

So what should investors do if they want to invest but are unsure about when to get into the markets? Come talk to us! Give us a call and help get a plan together that makes sense for your needs! Check out our new website: www.walkerwealthmgmt.com or give us a call at 416-960-5995!

An essential part of the business of investing involves figuring out how well you are doing. In some respects, the best benchmark for how well you are doing should be personalized to you. How conservative are you? What kind of income needs do you have? How old are you? While the case remains strong for everyone to have a personal benchmark to compare against their investment portfolios, in practice many people simply default to market indexes.

I’ve talked a little about market indexes before. They are poorly understood products, designed to give an impression about the overall health and direction of the economy and can serve as a guide to investment decisions. Large benchmarks, like the S&P 500, the TSX, or the FTSE 100, can tell us a great deal about the sentiment of investors (large and small) and what the expected direction of an economy may be.

But because these tools are usually poorly understood, they can contribute to as much confusion as they do clarity. For instance, the Dow Jones uses a highly confusing set of maths to determine performance. Last year General Electric lost about 50% of its market capitalization, while at the same time Boeing increased its market capitalization by 50%, but their impact on the Dow Jones was dramatically different. Boeing had an outsized positive contribution while General Electric had a much smaller negative impact.

The S&P 500 currently is one of the best preforming markets in 2018. Compared to most global indexes, the S&P 500 is ahead of Germany’s DAX, Britain’s FTSE 100 and FTSE 250, Japan’s Nikkei and Canada’s TSX. Yet if you are looking at your US focused investments, you might be surprised to see your own mutual funds lagging the index this year. If you were to ask an ETF provider or discount financial advisor why that is they would likely default to the answer “fees”, but they’d be wrong.

While the S&P 500 isn’t exactly “running away” it is doing considerably better than the TSX and the UK’s FTSE 100

This year is an excellent example of the old joke about Bill Gates walking into a bar and making each patron, on average, a millionaire. While the overall index has been performing quite well, the deeper story is about how a handful of companies are actually driving those returns, while the broader market has begun to languish. Of the 11 sectors in the S&P 500, only two are up, technology and consumer discretionary, while a further 6 were down for the year. In fact the companies driving most of the gains are: Facebook, Amazon, Apple, Alphabet (Google), Netflix and Microsoft. The 80 stocks in the consumer discretionary space not in that list have done almost nothing at all.

What does this portend for the future? There is a lot to be concerned about. The narrowing of market returns is not a good sign (although there have been some good results in terms of earnings), and it tends to warp investment goals. Investors demand that mutual fund returns keep up with their index, often forcing portfolio managers to buy more of a stock that they may not wish to have. In the world of Exchange Traded Funds (or ETFs), they participate in a positive feedback loop, pulling in money and buying more of the same stocks that are already driving the performance.

In all, indexes remain a useful tool to gage relative performance, but like with all things a little knowledge can be deceptive. The S&P 500 remains a strong performing index this year, but its health isn’t good. Healthy markets need broad based growth, and investors would be wise to know the details behind the stories of market growth before they excitedly commit money to superficially good performance.

Did that make you worried? Don’t be scared, call us to set up a review of your portfolio to better understand the risks!

For the past week I’ve been tinkering with a piece around the allegations that TD’s high pressure sales tactics had driven some staff to disregard the needs of their clients and encourage financial advisers in their employ to push for unsuitable products, and in some instances drove employees to break the law.

My general point was that the financial advising industry depends on trust to function, and runs into problems when those that we employ for those jobs serve more than one master. The sales goals of the big banks are only in line with the individual investor needs so long as investor needs serve the banks. In other words, clients of the banks frequently find that their interests run second to the profit and management goals of Canada’s big five.

For the uninitiated, Canada’s mutual fund industry can seem a little confusing, so let me see if I can both explain why a mutual fund company would do what it did, and how you can avoid it.

First, there are several different kinds of mutual fund companies:

There are companies like those of the banks, that provide both the service of financial advice and the mutual funds to invest in. This includes the five big banks and advice received within a branch.

There are also independent mutual fund companies that also own a separate investing arm that operate independently. Companies like CI Investments own the financial firm Assante, IA Clarington owns FundEx, and the banks all have an independent brokerage (for example TD has Waterhouse, RBC owns Dominion Securities and BMO owns Nesbitt Burns).

Lastly, there are a series of completely independent mutual fund companies with no investment wing. Companies like Franklin Templeton, Fidelity Investments, AGF Investments and Sentry Investments all fall into that category.

The real landscape is more complicated than this. There are lots of companies, and many are owned by yet other companies, so it can get muddy quickly. But for practical purposes, this is a fair picture for the Canadian market.

In theory, any independent financial adviser (either with a bank-owned brokerage, or an independent brokerage, like Aligned Capital) can buy any and all of these investments for our clients. And so, the pressure is on for mutual fund companies to get financial advisers to pay attention to them. If you are CI Investments, in addition to trying to win over other advisers, you also have your own financial adviser team that you can develop. But if you are a company like Sentry, you have no guarantee that anyone will pay attention to you. So how do you get business?

Sentry is a relatively new company. Firms like Fidelity and Franklin Templeton have been around for more than half a century. Banks have deep reserves to tap into if they want to create (out of nothing) a new mutual fund company. By comparison, Sentry has been around for just 20 years, and has had to survive through two serious financial downturns, first in 2000 and then 2008, as an independent firm. By all accounts, they’ve actually been quite successful, especially post 2009. You may have even seen some of their advertisements around.

Over the past few years independent mutual fund companies have increasingly turned to public advertising to try and encourage individual investors to bug their advisers about their funds.

But while Sentry has had some fairly good performance in some important sectors (from a business standpoint, it is more important to have a strong core of conservative equity products than high flying emerging market or commodity investments) it has also had some practices that have made me uncomfortable.

For a long time, Sentry Investments paid financial advisers more than most other mutual fund companies. For every dollar paid to an adviser normally, Sentry would pay an additional $0.25. That may not sound like much, but across enough assets thats a noticeable chunk of money. And while there is nothing illegal about this, it is precisely the kind of activity that makes regulators suspicious about the motives of financial advisers and the relationships they have with investment providers. Its no surprise that about a year ago Sentry scaled back their trailer to advisers to be more like the rest of the industry.

The fact is, though, that Sentry is in trouble because of their success. No matter how much Sentry was willing to pay advisers, no-one has a business without solid performance, and Sentry had that. The company grew quickly following 2008 and has been one of the few Canadian mutual fund companies that attracted new assets consistently following the financial meltdown. When times are good, it’s easy for companies to look past their own bottom line and share their wealth. That Sentry chose to have a Due Diligence conference in Beverly Hills and shower gifts on their attending advisers was a reflection of their success more than anything else.

And yet, from an ethical standpoint, it is deeply troubling. I have always been wary of companies that offer to pay more than the going market rate for fear that the motives of my decision could be questioned or maligned. Being seen to be ethical is frequently about not simply following the law, but doing everything in your power to avoid conflicts of interest (Donald Trump: take notice). The financial advisers attending the due diligence (who would have paid for their own air travel and hotel accommodation) probably had no reason to believe that the gifts they were receiving exceeded the annual contribution limit. But now those gifts cast them too in the shadow of dubious behaviour.

This is a man who has a hard time creating the impression that he is above ethical conflicts.

So how can you protect yourself from worries that your adviser is acting unethically, or being swayed to make decisions not in your interest? First, insist that your adviser at least offers the option of a fee for service arrangement. While the difference between an embedded trail and a transparent fee may be nominal, a fee-for-service agreement means that you have complete transparency in costs and full disclosure about where your advisers interests lie.

Second, if an embedded trail is still the best option, ask your adviser what the rationale was behind the selection of each of the funds in your portfolio, and what the trail commission was for each of those investments. This is information that you are entitled to, and you shouldn’t be shy about asking for.

Lastly, ask what mutual funds have given your adviser, but be open to the answer. Gifts to advisers are meant to fall into the category of “trinkets and trash”, mostly disposable items that are visibly branded by the company providing them, though gifts can be moderately more expensive. The difference between receiving cufflinks from Tiffany’s and cufflinks that bare the logo of a mutual fund firm is the difference between ethically dubious and openly transparent.

Regulators in Canada are pushing the industry towards a Fiduciary Responsibility for financial advisers. While that may clarify some of the grey areas, it will certainly create its own series of problems. Until then though, investors should not hesitate to question the investments they have, and why they have them. It may be unfair to expect the average Canadian to remember all the details about the types of investments that they have, but you should absolutely expect your financial adviser to be able to transparently and comprehensively explain the rationale and selection method behind the investments that you own.

If you would like an independent review of your current portfolio, please don’t hesitate to give us a call. 416-960-5995.

There is going to be lots of news around Brexit for the next while, and we have many other things to look at. So until more is known and more things are resolved this will be our last piece looking at the In/Out Referendum of June 23rd.

<> on September 12, 2015 in London, England.

So far the best thing that I’ve read about Brexit is an essay by Glenn Greenwald, who has captured much of the essential cognitive dissonance that revolves around the populist uprisings we’ve seen this year, from Bernie Sanders to Jeremy Corbyn and from Donald Trump to UKIP. You can read the essay here, but I think he gives a poignant take down of an isolated political class and an elitist media that fails to capture what drives much of the populism intent on burning down modern institutions. In light of that criticism, what should investors think about the current situation and how does it apply to their investments?

Let’s start with the basics; that leaving the EU is a bad idea but an understandable one. The Eurozone is rife with problems, from bureaucratic nonsense to democratic unaccountability, the whole thing gets under many people’s skin, and not just in the UK. Across Europe millions of people have been displaced from good work, have lost sight of the dignity in their lives and have come to be told repeatedly that the lives they lead are small, petty and must make way for a new way of doing things. The vast project that is the EU has been to reorder societies along new globalized lines, and if you live in Greece, Spain, Portugal or Italy those lines have come with terrible burdens of austerity and high unemployment.

It’s easy to see that the outstanding issues of the 21st century are going unchecked. Wealth inequality and increasing urbanization are colliding with the problems of expensive housing markets, wage stagnation and low inflation rates. The benefits of economic growth are becoming increasingly sparse as the costs of comfortably integrating into society continue to rise.

In response to these problems the media has shown little ability to navigate an insightful course. Trump is a fascist, Bernie Sanders is clueless, “Leave” voters are bigots, and any objection to the existing status quo that could upset the prescribed “correct” system is deemed laughably impractical or simply an enemy of free society.

This is a dynamic that can plainly not exist and if there is any hope in restoring or renewing faith in the institutions that govern much of our lives. We must find ways to more tactfully discuss big issues. Trump supporters are not idiots and fascists. Bernie supporters are not ignorant millennials. Leave campaigners are not xenophobic bigots. These are real people and have come to the feeling that they are disenfranchised citizenry who see the dignity of their lives is being undercut by a relentless march of progress. Addressing that will lead to more successful solutions to our collective woes than name calling and mud slinging.

For investors this continued disruption could not happen at a worse time. In some ways it is the needs of an aging population that have set the stage of much of the discontent. As one generation heads towards retirement having benefited from a prolonged period of stability and increasing economic wealth, the generations behind it are finding little left at the table. Fighting for stability means accepting that the current situation is worth fighting for. For retirees stability is paramount as years of retirement still need to be financed, but if you are 50 or younger fighting for a better deal may be worth the chaos.

For anyone doubts that cities are the most important part of our society and economic wealth, here is the history of cities over the past 5000 years. – From the Guardian

Investors should take note then that this is the new normal. Volatility is becoming an increasing fact of life and if wealth inequality, an unstable middle class and expensive urbanisation can not be tamed and conquered our politics will remain a hot bed of populist uprisings. So what can investors do? They need to broaden their scope of acceptable investments. The trend currently is towards more passive investments, like ETFs that mimic indices, but that only has the effect of magnifying the volatility. Investors should be speaking to their advisors about all options, including active managers, guaranteed retirement investments, products that pay income and even products with limited liquidity that don’t trade on the open market. This isn’t the time to limit your investment ideas, its the time to expand them.

Do you need new investment ideas? Give us a call to learn about all the different ways that investments can help you through volatile markets!

The buyers remorse now swirling around the UK seems to have ignited a renewed “Remain” campaign. Already there is a petition to have another referendum, citing the quite reasonable objections that a 52-48 split does not indicate the kind of definitive turnout to, in good conscience, topple the British economy and break up the UK. In other corners some of the bloom has quickly come off the rose.

Nigel Farage, the UKIP leader who has been championing the leave vote while Boris Johnson (BoJo for short) has parading across the country with a bus emblazoned with the phrase “we give the EU £350 million a week, let’s fund the NHS instead” has said that was a poor choice of campaign phrase. In other words the NHS will not be getting an additional £350 million per week. JoJo on the other hand has said that there is no urgency in triggering Article 50 of the Lisbon treaty, and instead there should be preliminary discussions before actually starting the leaving process.

Liars! Lying Liars!

In Cornwall, the picturesque seaside county with a crumbling and weak economy, it has suddenly dawned on the residents that they are hugely dependent on cash transfers from Brussels, an idea that had apparently not occurred to them when they overwhelmingly voted in favour of leaving.

It is worth taking some time to consider some underlying facts. The referendum is non-binding, merely advisory to the government. As the impact of a leave vote starts to set in and people begin to reject the emotional tenor of the campaign in favour of some hard truths, the next government will have time to try and potentially weasel out of the deal. The current front-runner for the next Prime Minister is BoJo himself, a man who had said that he sided with Leave (and became its very public face) because he didn’t think Brussels would really negotiate with the UK unless they knew the Britain might seriously leave.

So I’m going to go out on a limb here and say that Brexit will not happen, at least not like the worst case scenarios have made it out to be. David Cameron has said triggering Article 50 will fall to the next Prime Minister, which is months away. The chief proponents of Brexit don’t seem eager to start the clock on an official leave at all. Despite calls from within the EU to get the ball rolling on leaving, the real appetite to lock down a time table for a permanent withdrawal from the eurozone isn’t there. Instead it seems the winners are happier to let everyone know that they’ve got the gun, and that it’s loaded.

There are months to still screw this up, but the leave camp has had its outburst and now its time to look in the mirror and see the outburst for what it is; and ugly distortion of what the future could be. Nigel Farage and UKIP have had their moment, letting everyone know they are a serious force that needs to be addressed. But the stakes are far higher than I think many believed or thought could come to pass. The GBP fell dramatically, markets convulsed, Scotland and Northern Ireland might leave and starting Monday many financial jobs will start being cut in London. Now is the time to calm markets not with more interest rate cuts but with some measured language that could open the door to another referendum, or at least avoid the worst outcomes of an isolated and petulant Britain.

* this article had initially incorrectly identified Boris Johnson’s nickname as JoJo

As proof that the robot revolution will spare no one, even our industry is feeling the intense weight of cheap human alternatives in the form of “robo-advisors”. Given some glowing press by the Globe and Mail over the last weekend, robot advisors now represent a real and growing segment of the financial services markets and are forcing many advisors, including us, to ask how they and we will live together and what our respective roles will be.

To say that robo-advisors are a hot topic among financial advisers is to understate the collective paranoia of an industry that has come to see itself as besieged with critical and often unfair press. We haven’t been to a conference, meeting or industry event that doesn’t at some point involve financial advisors attempting to rationalize away the looming presence of cheap and impersonal financial advice. While there are some good questions that get asked at these events, there is a whiff of denial that must have given false hope to autoworkers in the 80s and 90s in these conversations.

For the uninitiated, robo-advisors are investing algorithms that provide a model portfolios based on a risk questionnaire that people can complete online. Typically using passive investment strategies (ETFs), these services charge lower fees than their human counterparts and offer little in the way of services. There isn’t anyone to talk to, no advice is dispensed and you won’t ever get a birthday card. But you can see your portfolio value literally anytime you like on your iPhone.

Looking past the idea of reducing your lifetime financial needs down to a level equivalent to a Netflix subscription, the concern around robo-advisors illustrates everything that our industry gets wrong about what services we provide that are most valuable. The pitch of automated cheap portfolio alternatives revolves entirely around the cost of the investments and has little to say about what it is that leads to bad financial self management.

The distinguishing feature between what we do, and what a computer algorithm can offer extends well past the price of the investment. Time and time again investors have shown themselves to be bad at investing regardless of their intentions. Financial advisors do not exist because there haven’t been cheap ways to invest money, they exist because there is an existential struggle between planning for events decades away and the fight or flight responses burned into our most reptilian brains. When times get tough investors make bad choices. Financial advisors are there to stop those decisions before they permanently define or destroy an investor’s long term plans.

That multi-decade struggle between an advisor and their client’s most primal instincts is an intangible quality and takes many forms. Genial conversations about new investing ideas, gentle reminders not to overweight stocks that are doing well, trimming earnings and investing in out of favour sectors and sometimes just being there to listen to people as they make sense of their problems and financial concerns is an ongoing roll that we, and thousands of other advisors, have been happy to fill. These qualities can be difficult to quantify, but can be best expressed in two ways. First, by the independent research which has shown that Canadians who work with a financial advisor have 2.7x the assets of investors who didn’t and second, by the number of our clients who have remained clients for the near quarter of a century of our family practice.

Fees, by comparison, are very tangible and as a rule people hate fees. And while bringing down costs is a reasonable expectation in any service, there is a snarky cockiness to proponents of robo-advisors that see the job of financial management as both straight forward and simple. Robot champions are quick to say that financial advisors must adapt to the new world that they are forging, but it is unclear just how different and liberating this world will be. Far from creating a new utopia of cheap financial management for everybody, what seems more likely is that they will have merely created a low cost financial option for low income Canadians, a profitable solution for banks and other large financial firms but not for their investors.

The proof of the pudding is in the tasting, as they say. When the markets suddenly collapsed in the beginning of the year, bottoming out in mid-February, robo-investors did not sit idly by and let their robot managers tend to their business unmolested. Robot advisory practices were swamped with phone calls and firms relied on call centres and asked employees to stay later and work more hours to deal with the sudden influx of concerned investors wondering what they should do, whether they should leave the markets and what was going to happen to their investments. As it turns out, when times are bad people just want to talk to people.

Most Canadians started saving with an adviser when they had few assets. Start saving for your future now by sending us a message!

With Brexit around the corner, the potential for a Donald Trump presidency and a host of other global problems (big problems), it’s hard not to talk about all the chaos and what it might mean to investors even when there is lots of other things to go over. For now, this will be our last article on the subject of Brexit until next week following the vote. I will take a look at some other issues later in the week.

Here's our piece on the potential for a "Brexit," which is a not great word and a worse idea. https://t.co/VGYmalNGZq

— Last Week Tonight (@LastWeekTonight) June 20, 2016

One thing that jumps out at me about “Brexit” is how fragile much of our world is. Progress is most often thought of as making things stronger or better, but that is only true to a point. Progress also has the unfortunate downside of making things much more fragile. The more progress allows us to do, the more fragile each step makes us.

Beautiful tall buildings like this remain a testament to our progress and how profoundly fragile it all is.

Historically that fragility can frequently be seen during times of war. Britain, undoubtedly the world’s most powerful empire at the outset of the first and second world war, saw how quickly its strengths could be overcome by the weaknesses of a far flung empire. The supply lines, the distant resources and the broad reach of the war all exposed the underlying frailty of the British Empire. Two World Wars was all it took to end an empire that had been 500 years in the making.

What we hold in common with the British Empire is the causal assumption that things are the way they are naturally, that we cannot change the inherent status quo in our lives. Canada, the United States and Europe are rich nations because they are naturally rich nations, and not the result of a combination luck, science, philosophy and culture that have conspired to land us where we are today.

We live in a breakable society, one that doesn’t realize how fragile it is. In the past few years it has been tested in a multitude of ways, and this year is no exception. Brexit isn’t even the worst of how it can be. Syria has been reduced to rubble, Turkey has essentially lapsed into a dictatorship, with Russia having gone the same way. Venezuela, which I wrote about earlier, has moved from breadlines to mob violence.

Progress isn’t just uneven, it also isn’t guaranteed. Nations, empires and great civilizations have all come and gone, each of them burning brightly, however briefly, before being extinguished. The speed of a decline in Venezuela isn’t just a result of bad management, it is a reflection to just how much support our civilization needs. The rise of the new introverted nationalism doesn’t see this, and has sought an imagined self sufficiency as a way to relieve temporary difficulties. If people thought that the EU was difficult to deal with when you were a part fo it, wait until you aren’t.

Brexit is a choice that is both scary and appealing because it is scary. For an entire generation there may never be a choice like this again, a chance to permanently alter the geopolitical landscape, even with little understanding of what those changes can mean or do. Whether Britain will be poorer or richer over the next decade may ultimately hinge on the vote this Friday. Far more frightening is whether our ability to build something lasting, powerful but fragile will be permanently undone in the European sphere.

With the BREXIT vote now only days away its worth taking a moment to consider the dramatic political shift that seems to be happening around the globe. Where once left/right politics dominated, or pro-capitalism vs. pro-socialist forces clashed, today the challenge is far more frightening. Today we sit on the brink of the end of the new internationalism and face the rise of old nationalism.

In Jon Ronson’s funny and insightful book THEM: Adventures with Extremists, the author describes his final meeting with a founding member of the Bilderberg Group (yes, that Bilderberg Group) Lord Healy, who explains that at the end of the Second World War a real effort was made to encourage trade and economic growth as a way of deferring future wars. The Bilderberg Group is but one of many, slightly shadowy and often undemocratic, organizations that exist to further those goals, encouraging powerful people to air out their issues and discuss ways to make that vision of the world more likely.

The response to the growing frustration on all these issues has been a resurgence of nationalism and political “strong-men”. Putin’s Crimea grab was as much about returning pride to Russia as it was about diverting attention from his own domestic issues, reestablishing Russia’s place as a significant regional power. Across Europe there are rumblings, both of renewed regional nationalism from within countries, as well as growing concern that a “leave vote” in Brexit could destabilize the entire EU experiment. In the United States these issues have given power to the Donald Trump populism, but have also fired the Bernie Sanders campaign.

Energy to these issues have undoubtedly been fueled as a result of 2008, a disaster so wide reaching and so disruptive to the Internationalist narrative about the skill set of the political and corporate classes that it shouldn’t be surprising that millions of people seem ready to do irreparable harm to the status quo. The subsequent inability to provide a strong and sustained economic recovery like some recessions of the past has only made matters worse. Every ill, every short coming, every poor decision and every injustice inherent within the structure that we inhabit is now expected to be resolved by setting the whole thing on fire and assuming that the problem is solved.

I am constantly surprised by how little people actually want to see changed by referendums like these. During the Scottish Referendum, the expectation was that Scotland would continue on exactly as it does, but without any association to London. The Leave campaign in Britain is quite sure that while Britain will no longer be part of the common market, a deal can be worked out that will allow free trade to continue unabated and for British people who live in places like Spain and Italy to continue to do so without visas or travel restrictions. Donald Trump is quite convinced that he can have a trade war with China without upsetting American business interests there, and the host of smaller countries like Venezuela or Turkey can slide into despotism without adverse impacts to their international reputation.

We’re at the edge, with the mob pushing for change (any change) with little real understanding of the consequences. It is little surprise that the technocrats and political establishment are so unlikable and so uninspiring in the face of the radicals and revolutionaries that want to see a sizable change that can’t be brought about until everything is torn down. And while it is true that the status quo can’t remain, it is equally unlikely that the end of the EU, or a British exit will stem the tide of migrants from Eritrea, or that tearing up NAFTA will return factories to Michigan, or that Marine Le Pen can turn the clock back on France and bring back the beret.

I expect market volatility over the next while as investors and deal makers try and figure out the correct response to either a leave or remain vote. If Britain does leave, the next 100 days will be telling as pronouncements will be made to try and smooth the troubled waters. But the real work will come in the next 2 years, as negotiations will begin to do all the hard work that the referendum creates. You can’t just burn it all down, you have to build something in its place. How successful the reformers are at the latter will be the real test of the new nationalism.

This house sold for $1,000,000 in Vancouver. Is it houses that are in demand, or land?

In the mountains of articles written about Toronto’s exuberant housing market, one aspect of it continues to be overlooked, and surprisingly it may be the most important and devastating outcome of an unchecked housing bubble. Typically journalistic investigation into Toronto’s (or Vancouver’s) rampant real estate catalogues both the madness of the prices and the injustice of a generation that is increasingly finding itself excluded from home ownership, finally concluding with some villain that is likely driving the prices into the stratosphere. The most recent villain du-jour has been “foreign buyers”, prompting news articles for whether their should be a foreign buyer tax or not.

What frequently goes missing in these stories are the much more mundane reasons for a housing market to continue climbing. That is that in the 21st century cities, like Toronto, now command an enormous importance in a modern economy while the more rural or suburban locations have ceased to be manufacturing centres and are now commuter towns. Combined with a growing interest in the benefits of urban living and the appeal of cities like Toronto its no surprise that Toronto is the primary recipient of new immigrants and wayward Canadians looking for new opportunities.

Toronto itself, however, has mixed feelings about it’s own growth. City planners have made their best efforts to blend both the traditional idea of Toronto; green spaces, family homes and quiet neighbourhoods, with the increasing need of a vertical city. Toronto has laid out its plans to increase density up major corridors while attempting to leave residential neighbourhoods intact. Despite that, lots of neighbourhood associations continue to fight any attempt at “density creep”. Many homeowners feel threatened by the increasing density and fear the loss of their local character and safety within their neighbourhoods, at times outlandishly so. Sometimes this comically backfires, but more often than not developers find themselves in front of the OMB (Ontario Municipal Board) fighting to get a ruling that will allow them to go ahead with some plan, much to the anger of local residents and partisan city councillors.

The result is that Toronto seems to be growing too fast and not fast enough simultaneously, and in the process it is setting up the middle class to be the ultimate victims of its own schizophrenic behaviour.

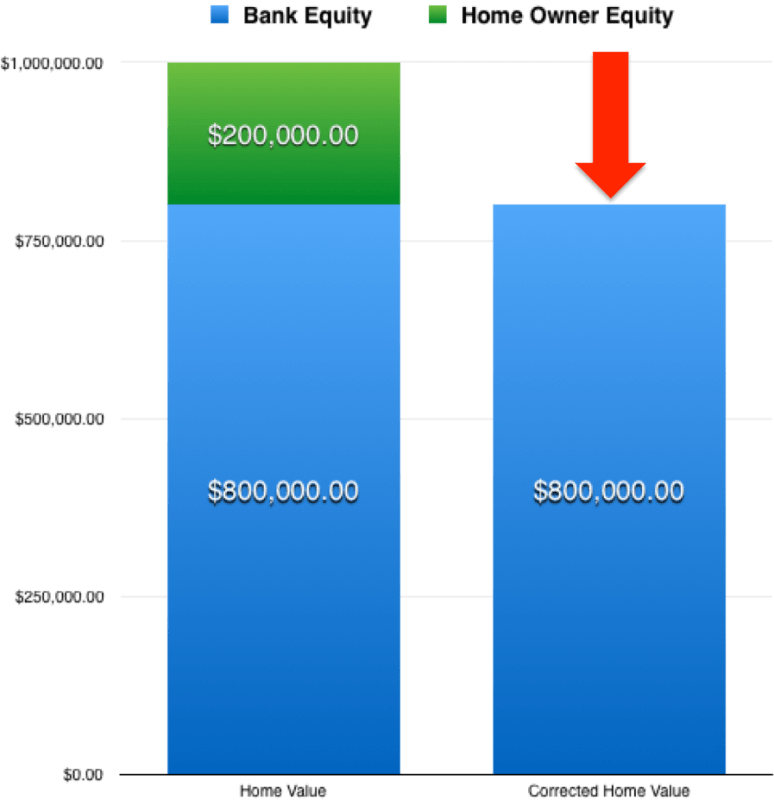

High house prices go hand in hand with big mortgages. The bigger home prices get the more average Canadians must borrow for a house. Much of the frightening numbers about debt to income ratios for Canadians is exclusively the result of mortgage debt, while another large chunk is HELOCs (home equity lines of credit). Those two categories of debt easily dwarf credit cards or in store financing. This suits banks and the BoC not simply because houses are considered more stable, but because banks have very little at risk in the financial relationship.

To illustrate why banks have so little at risk, you only need to look at a typical mortgage arrangement. Say you buy a $1 million home with a 20% down payment, the bank would lend you $800,000 for the rest of the purchase. But assume for a second that housing prices then suddenly collapse, wiping out 20% of home values, how much have you lost? Well its a great deal more than 20%. Because the bank has the senior claim on the debt, the 20% of equity wiped out translates into a 100% loss for you, the buyer. The bank on the other hand still has an $800,000 investment in your home that must be paid back.

By itself this isn’t a problem, but financial stability and comfort is built around having a set of diversified resources to fall back on. In 2008, in the United States, home owners in the poorest 20% of the population saw not just their home prices collapse, but also all of their financial resources. On average if you were part of the bottom 20% you only had $1 in other assets for every $4 in home equity. By comparison the richest 20% had $4 in other assets for every $1 in home equity. The richest Americans weren’t just better off because they had more money, but because they had a diversified pool of assets that could spread the risk around. Since the stock market bounced back so quickly while much of the housing market lagged the result was a widening of wealth inequality following 2008.

The impact of 2008 on household net worth by quintile. From House of Debt by Atif Mian and Amir Sufi

In Toronto the situation is a little different. Exorbitant house prices means lots of people have the bulk of their assets tied up in home equity. Funding the enormous debt of a house may preclude investing outside the home or building up retirement reserves in RRSPs and TFSAs. A change in interest rates, or a general correction in the housing market would have the effect of both wiping out savings while simultaneously raising the burden that debt places on families.

There will probably never be as full throated a reason for my job than the burden the Toronto housing market places on Canadians. From experience we know that concentrating wealth inside a home contributes to economic fragility, potentially robbing home owners of longer term goals and squeezing out smart financial options. But far more important now is that city councillors and home owners come to realize that the housing market is more prison than home, shackling the city to ever more tenuous tax sources and weakening the finances of the middle class. Until then, smart financial planning alongside home ownership is still in the best interests of Canadian families.

Yesterday a disturbing article came across my desk. From Bloomberg, it was titled “It Just Got Even Harder to Trust Financial Advisors” and is a brief summary of a new report out of the United States that suggests that there is wide spread misconduct within financial services. Far from being an isolated number of financial advisors, the scale of the disciplinary actions is extensive and has encompassed some of the largest banking institutions in the United States (for those mistrustful of the Wall Street crowd that may not be a big shock) including some well known names like Wells Fargo and UBS.

Being disciplined within the world of financial services is controversial and being reprimanded does not necessarily denote contrition from advisors. The two chief complaints from investors, both in Canada and the United States, revolves around suitability of investments and subsequent fees. Those might seem like straight forward complaints to have, but many investors have a difficult time wrapping their heads around “risk”, showing great comfort in investments that can rapidly rise, while expressing dismay when they fall just as rapidly back to earth. Thus investors and advisors can mistakenly assume that they are on the same page with each other, only to find that at a later point that they have badly misunderstood one another.

This will be so awesome if I don’t fall!

Regulators have correctly understood that the problem is a misalignment of education and comfort. If investors knew more about investing they would be better at understanding risk. If that were the case though investors would be unlikely to need the services of financial advisors. Thus financial advisors are expected to treat their clients as though they know little, and should be expected to challenge investors, even reject investor requests if the investment is deemed too risky by the advisor.

What regulators want is for advisors to understand their role now as “risk managers” rather than product floggers and order takers. In an industry where the average age is north of 55, most advisors got their start and built their business around exactly that, selling interesting and exciting ideas. The transition from that to telling investors that they can’t do what they want with their money (it’s their money after-all) has not been simple.

One move, cited in the article, is to move to a fiduciary model to rectify outstanding issues around fees in particular. There is a persistent fear that advisors might choose high fee-low returning investments when cheaper and better performing options exist. Curiously, in Canada at least, there is not much evidence to suggest that this happens. But even if this avenue resolves such a problem many within the industry fear that “high fee/low return” will not be apparent until well after the fact, opening up practitioners to hindsight litigation.

The simple fact is though that regardless of the nuances and difficulties that surround properly managing and regulating the financial services industry, no good can come from a growing sense of mistrust in an industry that has become so essential to the retirement plans of so many. So what should investors know that will protect them from bad decisions or unfair fees?

First, be familiar with the nature of fees:

There is a tendency to assume that the best fee is the lowest, but costs frequently correspond to the complexity of the investments, the size of the assets under management and the support around the product. Be sure to find out what the MER (management expense ratio) is and find out whether it is comparable to other similar products. It’s fair to have questions about what products cost and whether those costs make sense.

Second, be more than a number:

The article contains one of those slights of hand when people try and diffuse blame, pointing out that it isn’t “just small dealers” that have been guilty of misconduct. This suggestion that small is typically the problem seems challenged by evidence. Big problems require scale, and it isn’t uncommon for some brokers in the banks to have thousands of clients. Brokers aren’t happy with that arrangement and neither are investors, but it is very common. It shouldn’t be surprising that misconduct can come from large banks seeking easy solutions with proprietary product.

Third, independent options are better than proprietary ones:

A frequent issue I come across are investors who have been sold a proprietary product when other better options exist. It strikes me that there are real conflicts of interest in companies that both manage people’s assets and sell investments for that purpose. Most brokers I know have all felt better knowing that their responsibility is to a client sole, without having to hit bottom line targets for other interests. A wide range of product offerings doesn’t guarantee you’ll get the best product, but does remove the threat someone will deliberately sell you the wrong one.

Fourth, be Canadian:

The concerns of America and Canadian regulators are very similar, but the good news is that Canadians have a better system. Despite complaining Canadians have some clear advantages. First, performance disclosure rules favour investors here. Rather than show returns with costs yet to be deducted, returns in Canada are shown net of all costs, meaning you see accurate performance. Second, the use of commissions and deferred sales charges, the source of ire for regulators and critics, have been dropping for years. Many financial advisors now rely on exclusively trailers or disclosed fees. Third, even trailers aren’t that bad. Where as there has been an outstanding concern is that embedded trail fees could unduly influence advisors to make poor choices. But while there is some truth to this statement, the vast bulk of investments within Canada have standardized their fees, with companies paying bigger payouts to entice sales having become the outlier.

Fifth, be with us:

As part of a small and independent firm one of the things we pride ourselves most on is to be in the right place to help Canadians. An open shop, we have both the luxury of picking the best investments from across the industry while offering investors competitive fees. But most importantly, we value transparency and clarity in managing your retirement savings.

As a family business that has been around for nearly a quarter of a century, the essential difference between being a number and receiving personal care is whether you have someone to work with that doesn’t just know your name, but comes to know you as well.

Also they should have a blog.

Give us a call if you are looking for some personal guidance in dealing with difficult markets or have questions about protecting your accounts.

If there was ever going to be a moment to gain some clarity about what the Brexit would truly and ultimately mean, Friday was the day. Following the win by the leave camp, markets were sent reeling on the uncertainty stirred up by the referendum, and by the day’s end Britain had gone from being the

If there was ever going to be a moment to gain some clarity about what the Brexit would truly and ultimately mean, Friday was the day. Following the win by the leave camp, markets were sent reeling on the uncertainty stirred up by the referendum, and by the day’s end Britain had gone from being the

As proof that the robot revolution will spare no one, even our industry is feeling the intense weight of cheap human alternatives in the form of “robo-advisors”. Given some glowing press by the Globe and Mail over the last weekend, robot advisors now represent a real and growing segment of the financial services markets and are forcing many advisors, including us, to ask how they and we will live together and what our respective roles will be.

As proof that the robot revolution will spare no one, even our industry is feeling the intense weight of cheap human alternatives in the form of “robo-advisors”. Given some glowing press by the Globe and Mail over the last weekend, robot advisors now represent a real and growing segment of the financial services markets and are forcing many advisors, including us, to ask how they and we will live together and what our respective roles will be. To say that robo-advisors are a hot topic among financial advisers is to understate the collective paranoia of an industry that has come to see itself as besieged with critical and often unfair press. We haven’t been to a conference, meeting or industry event that doesn’t at some point involve financial advisors attempting to rationalize away the looming presence of cheap and impersonal financial advice. While there are some good questions that get asked at these events, there is a whiff of denial that must have given false hope to autoworkers in the 80s and 90s in these conversations.

To say that robo-advisors are a hot topic among financial advisers is to understate the collective paranoia of an industry that has come to see itself as besieged with critical and often unfair press. We haven’t been to a conference, meeting or industry event that doesn’t at some point involve financial advisors attempting to rationalize away the looming presence of cheap and impersonal financial advice. While there are some good questions that get asked at these events, there is a whiff of denial that must have given false hope to autoworkers in the 80s and 90s in these conversations.

One move, cited in the article, is to move to a fiduciary model to rectify outstanding issues around fees in particular. There is a persistent fear that advisors might choose high fee-low returning investments when cheaper and better performing options exist. Curiously, in Canada at least, there is not much evidence to suggest that this happens. But even if this avenue resolves such a problem many within the industry fear that “high fee/low return” will not be apparent until well after the fact, opening up practitioners to hindsight litigation.

One move, cited in the article, is to move to a fiduciary model to rectify outstanding issues around fees in particular. There is a persistent fear that advisors might choose high fee-low returning investments when cheaper and better performing options exist. Curiously, in Canada at least, there is not much evidence to suggest that this happens. But even if this avenue resolves such a problem many within the industry fear that “high fee/low return” will not be apparent until well after the fact, opening up practitioners to hindsight litigation.