On December 10th, the Bank of Canada released it’s Financial System Review for 2014. It outlined numerous problems that continue to grow and potentially undermine the Canadian economy. Globally this report attracted a great deal of attention, not something the BoC is used too, but with a rising concern that the Canadian housing market is overvalued, an official document like the FSR gets noticed.

On December 10th, the Bank of Canada released it’s Financial System Review for 2014. It outlined numerous problems that continue to grow and potentially undermine the Canadian economy. Globally this report attracted a great deal of attention, not something the BoC is used too, but with a rising concern that the Canadian housing market is overvalued, an official document like the FSR gets noticed.

To understand why Canada is growing in focus among financial analysts around the world you need to turn the clock back to 2008. While major banks and some countries went bankrupt, Canada and its banking system was relatively unscathed. And while the economy has suffered due to the general economic slowdown across the planet, the relative health of our financial system made us the envy of many.

To understand why Canada is growing in focus among financial analysts around the world you need to turn the clock back to 2008. While major banks and some countries went bankrupt, Canada and its banking system was relatively unscathed. And while the economy has suffered due to the general economic slowdown across the planet, the relative health of our financial system made us the envy of many.

But the problems we’d sidestepped now seem to be hounding us. Low interest rates have helped spur our housing market to new highs, while Canadians in general have continued to amass debt at record levels. Attempts to slow the growth of both house prices and improve the standard of debt for borrowers by the government have only moved loan growth into subprime territory.

But the problems we’d sidestepped now seem to be hounding us. Low interest rates have helped spur our housing market to new highs, while Canadians in general have continued to amass debt at record levels. Attempts to slow the growth of both house prices and improve the standard of debt for borrowers by the government have only moved loan growth into subprime territory.

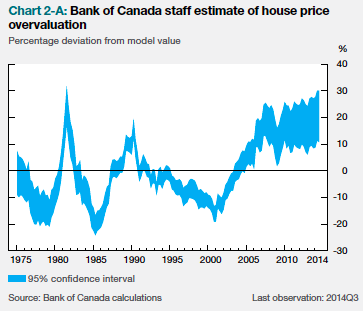

If all this sounds familiar, it’s because we’ve been talking about it for sometime, and sadly the BoC hasn’t been able to add much in the way of clarity to this story. While we all agree that house prices are overvalued, no one is sure quite how much. According to the report the range is between 10% to 30%. Just keep in mind that if you own a million dollar home and the market corrects, it would move the price from $900,000 to as low as $700,000. That can make a considerable dent to your home equity and its too big a swing to plan around.

On top of this is the growth of the subprime sector in the market. Stiff competition between financial institutions and an already tapped out market has encouraged “certain federally regulated financial institutions” to increase “their activities in riskier segments of household lending.” This is true not just in houses but also in auto loans, where growth as been equally strong.

On top of this is the growth of the subprime sector in the market. Stiff competition between financial institutions and an already tapped out market has encouraged “certain federally regulated financial institutions” to increase “their activities in riskier segments of household lending.” This is true not just in houses but also in auto loans, where growth as been equally strong.

The Financial System Review also goes on to talk about problems growing in both cybersecurity and in ETFs (both subjects we have written about). It also talks about some of the positive outlooks for the economy, from improving economic conditions globally and support for continued economic activity. But its quite obvious that the problem Canadians are facing now is significant underlying risk in our housing and debt markets. These problems could manifest for any number of reasons (like a sudden drop in the price of oil, a significant slowdown in China, or a fresh set of problems from Europe), or they may lay dormant for months and years to come.

For Canadians the big issues should be getting over our sense of economic specialness. As I heard one economist put it “Canadians feel that they will be sparred an economic calamity because they are Canadian.” This isn’t useful thinking for investors and as Canadians we are going to have separate our feelings about our home from the realities of the market, something that few of us are naturally good at. But long term investor success will depend on remaining diversified (I know, I link to that article a lot), and showing patience in the face of market panic.