One of the challenges of being a financial advisor is finding ways to convey complex financial issues in simple ways to my clients and readers. I believe I do this to varying degrees of success, and I am informed of my failures by my wife who doesn’t hesitate to point out when I’ve written something boring or too convoluted.

One such subject where I feel I’ve yet to properly distill the essential material is around the housing market. While I’ve written a fair amount about the Canadian housing market, I feel I’ve been less successful in explaining why the current housing situation is eating the middle class.

In case you’re wondering, my thesis rests on three ideas:

1. The middle class as we know it has come about as a result of not simply rising wages but on sustained drops in the price of necessities.

2. The rise of the middle class was greatly accelerated by the unique historical situation at the end of the Second World War, which split the world into competing ideological factions but left the most productive countries with the highest output and technological innovation to flourish.

3. A global trend towards urbanization and a plateauing of middle-class growth has started reversing some of those economic gains, raising the cost of basic living expenses while reducing the average income.

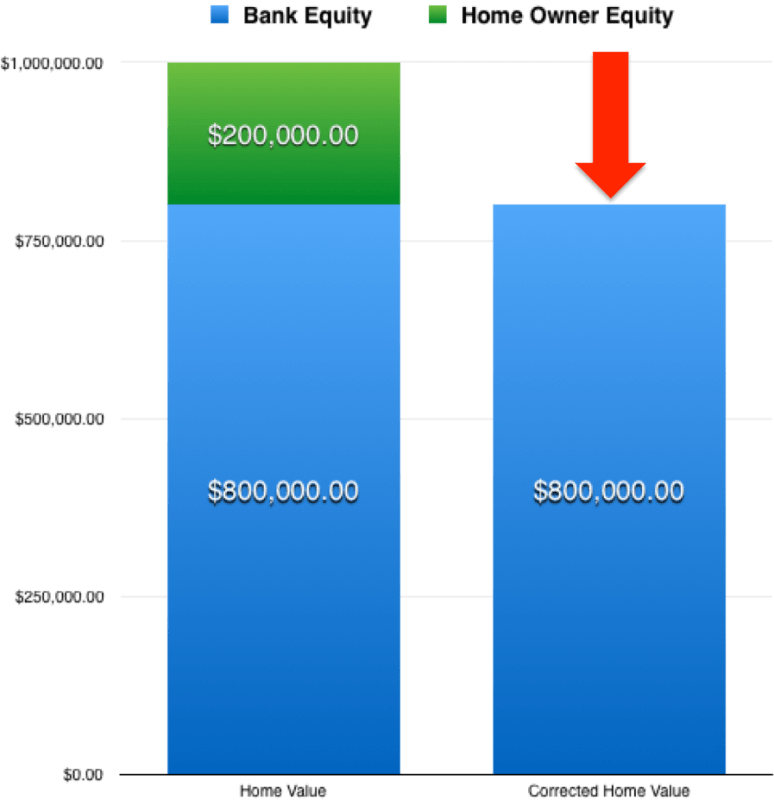

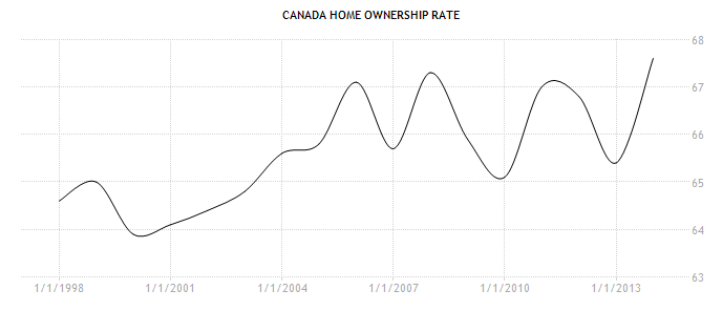

The combination of these three trends has helped morph housing from an essential matter of accommodation into a major pillar of people’s investment portfolios and part of their retirement plan. The result is that homeowners are both far more willing to pay higher prices for a home in the belief that it will continue to appreciate into the future, while also attempting to undercut increases in density within neighborhoods over fears that such a change will negatively impact the value of the homes. In short, stabilizing the housing market is getting harder, while Canadians are paying too much of their income to pay for existing homes. All of this serves to make the Canadian middle class extremely vulnerable.

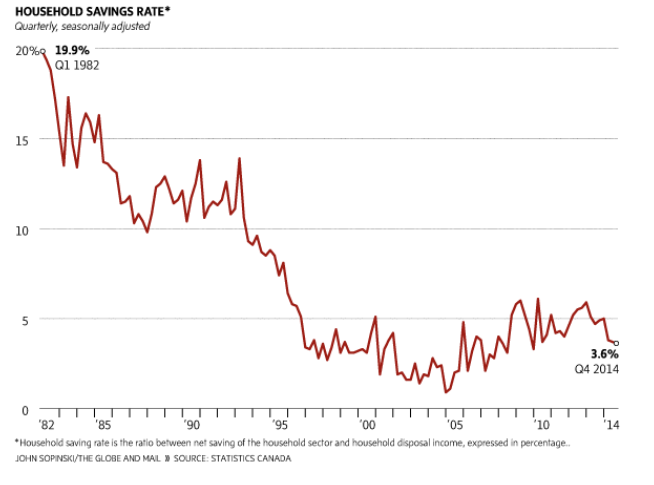

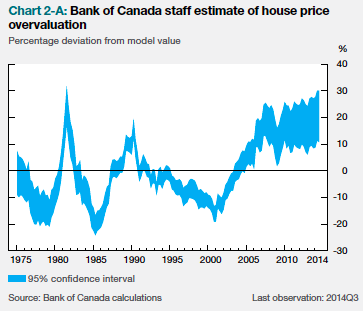

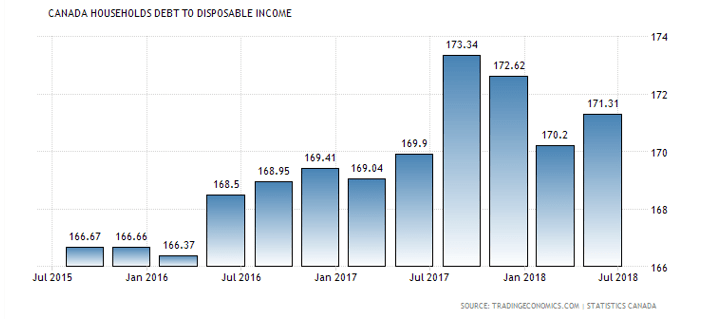

Proving some of this is can be challenging, but there are some things we know. For instance, we know that Canadians are far more in debt than they’ve ever been before and the bulk of that debt is in mortgages and home equity lines of credit (HELOC), which means much of that debt is long-term and sensitive to hikes in interest rates. We also have abundant evidence that zoning restrictions and neighborhood associations have diligently fought against “density creep”. But to tie it all together we need the help of HSBC’s Global Research division and a recent article from the Financial Times.

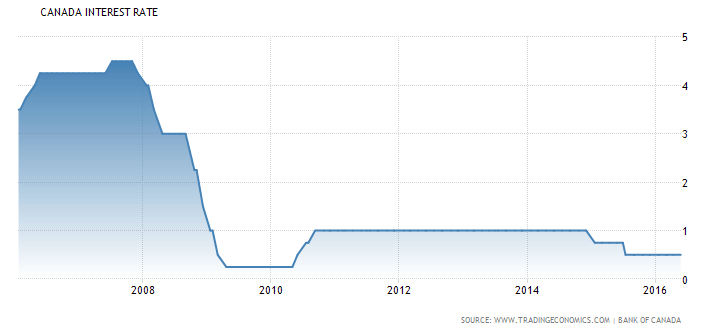

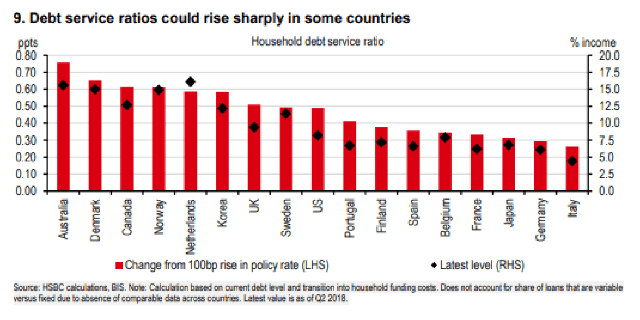

Last week, HSBC issued a research paper on global leverage. Providing more proof that since 2008 the world has not deleveraged one bit. In fact, global debt has settled just over 300% of global GDP, something that I wrote about in 2016. An interesting bit of information though came in terms of the country’s sensitivity to increasing interest rates. Charting a number of countries, including Canada, the report highlights that Canadians (on average) pay 12.5% of their income to service debt. A 1% increase in the lending rate would push that up over 13%. For a country already heavily in debt, a future of rising rates looks very expensive indeed.

It would be wrong to say that fixing our housing market will put things right. There is no silver bullet and to suggest otherwise is to reduce a complex issue to little more than a TED Talk. But the reality is that our housing market forms a major foundation of our current woes. A sustained campaign to grow our cities and reduce regulatory hurdles will do more to temper large debts that eat at middle-class security than anything I could name.