In the mountains of articles written about Toronto’s exuberant housing market, one aspect of it continues to be overlooked, and surprisingly it may be the most important and devastating outcome of an unchecked housing bubble. Typically journalistic investigation into Toronto’s (or Vancouver’s) rampant real estate catalogues both the madness of the prices and the injustice of a generation that is increasingly finding itself excluded from home ownership, finally concluding with some villain that is likely driving the prices into the stratosphere. The most recent villain du-jour has been “foreign buyers”, prompting news articles for whether their should be a foreign buyer tax or not.

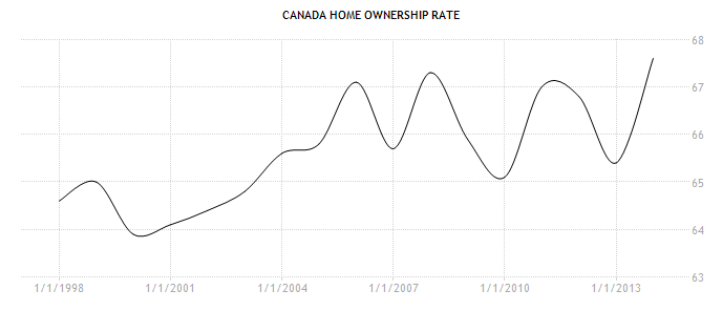

What frequently goes missing in these stories are the much more mundane reasons for a housing market to continue climbing. That is that in the 21st century cities, like Toronto, now command an enormous importance in a modern economy while the more rural or suburban locations have ceased to be manufacturing centres and are now commuter towns. Combined with a growing interest in the benefits of urban living and the appeal of cities like Toronto its no surprise that Toronto is the primary recipient of new immigrants and wayward Canadians looking for new opportunities.

Toronto itself, however, has mixed feelings about it’s own growth. City planners have made their best efforts to blend both the traditional idea of Toronto; green spaces, family homes and quiet neighbourhoods, with the increasing need of a vertical city. Toronto has laid out its plans to increase density up major corridors while attempting to leave residential neighbourhoods intact. Despite that, lots of neighbourhood associations continue to fight any attempt at “density creep”. Many homeowners feel threatened by the increasing density and fear the loss of their local character and safety within their neighbourhoods, at times outlandishly so. Sometimes this comically backfires, but more often than not developers find themselves in front of the OMB (Ontario Municipal Board) fighting to get a ruling that will allow them to go ahead with some plan, much to the anger of local residents and partisan city councillors.

The result is that Toronto seems to be growing too fast and not fast enough simultaneously, and in the process it is setting up the middle class to be the ultimate victims of its own schizophrenic behaviour.

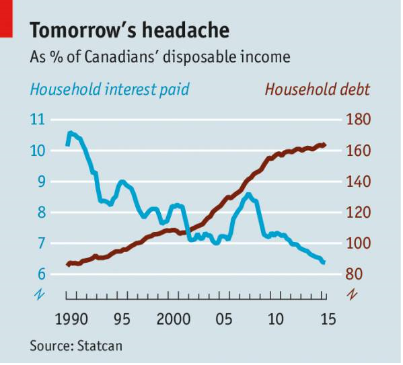

High house prices go hand in hand with big mortgages. The bigger home prices get the more average Canadians must borrow for a house. Much of the frightening numbers about debt to income ratios for Canadians is exclusively the result of mortgage debt, while another large chunk is HELOCs (home equity lines of credit). Those two categories of debt easily dwarf credit cards or in store financing. This suits banks and the BoC not simply because houses are considered more stable, but because banks have very little at risk in the financial relationship.

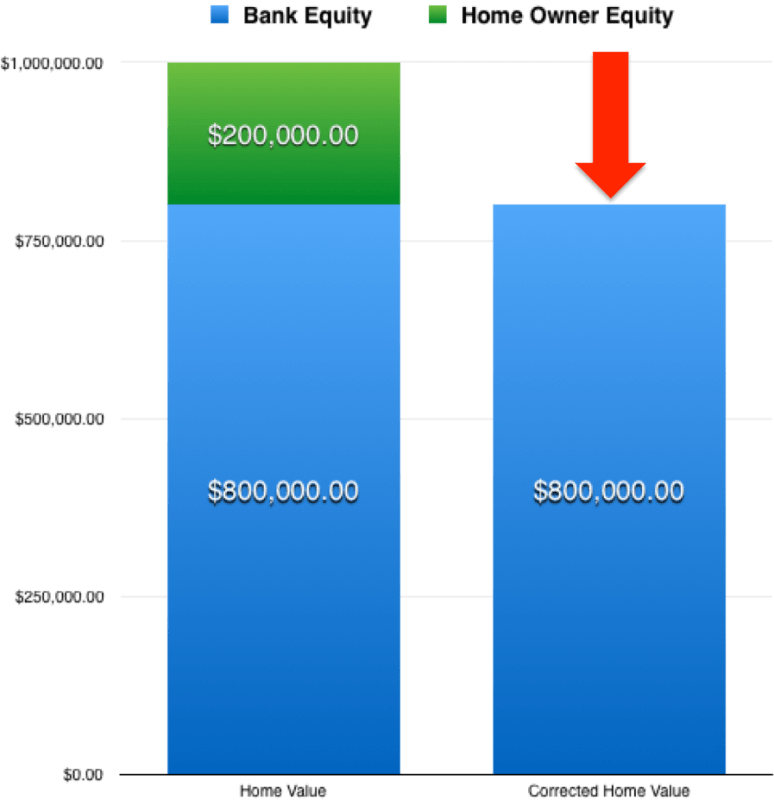

To illustrate why banks have so little at risk, you only need to look at a typical mortgage arrangement. Say you buy a $1 million home with a 20% down payment, the bank would lend you $800,000 for the rest of the purchase. But assume for a second that housing prices then suddenly collapse, wiping out 20% of home values, how much have you lost? Well its a great deal more than 20%. Because the bank has the senior claim on the debt, the 20% of equity wiped out translates into a 100% loss for you, the buyer. The bank on the other hand still has an $800,000 investment in your home that must be paid back.

By itself this isn’t a problem, but financial stability and comfort is built around having a set of diversified resources to fall back on. In 2008, in the United States, home owners in the poorest 20% of the population saw not just their home prices collapse, but also all of their financial resources. On average if you were part of the bottom 20% you only had $1 in other assets for every $4 in home equity. By comparison the richest 20% had $4 in other assets for every $1 in home equity. The richest Americans weren’t just better off because they had more money, but because they had a diversified pool of assets that could spread the risk around. Since the stock market bounced back so quickly while much of the housing market lagged the result was a widening of wealth inequality following 2008.

In Toronto the situation is a little different. Exorbitant house prices means lots of people have the bulk of their assets tied up in home equity. Funding the enormous debt of a house may preclude investing outside the home or building up retirement reserves in RRSPs and TFSAs. A change in interest rates, or a general correction in the housing market would have the effect of both wiping out savings while simultaneously raising the burden that debt places on families.

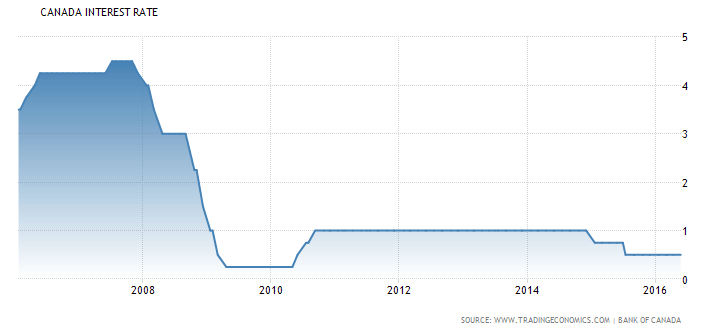

The issue of debt is one that the government and the BoC take seriously, yet despite the potential impact of high debt levels on Canadians and the looming threat it poses to the economy the mood has remained largely indifferent. The BoC, under the governorship of Stephen Poloz, has said that it isn’t worried too much about Canada’s housing market. This isn’t because there isn’t a huge risk that it could implode, but because even if it does it is unlikely to start a run on the banks. By comparison the view of Stephen Poloz on the debt levels of Canadians is that its your problem. A curious stance given that the BoC’s position has been to try and stimulate the economy with low borrowing rates.

There will probably never be as full throated a reason for my job than the burden the Toronto housing market places on Canadians. From experience we know that concentrating wealth inside a home contributes to economic fragility, potentially robbing home owners of longer term goals and squeezing out smart financial options. But far more important now is that city councillors and home owners come to realize that the housing market is more prison than home, shackling the city to ever more tenuous tax sources and weakening the finances of the middle class. Until then, smart financial planning alongside home ownership is still in the best interests of Canadian families.