As we bring this year to a close, markets continue to frustrate. The US markets, along with most global markets and especially Canada, are all negative. Over the past few weeks Canada has dipped as low as -13% on it’s year-to-date (YTD) return. In speaking with some people within my industry, expectations to finish flat for the year will be sufficient for a pat on the back and considered solid performance.

As we bring this year to a close, markets continue to frustrate. The US markets, along with most global markets and especially Canada, are all negative. Over the past few weeks Canada has dipped as low as -13% on it’s year-to-date (YTD) return. In speaking with some people within my industry, expectations to finish flat for the year will be sufficient for a pat on the back and considered solid performance.

Years are ultimately an arbitrary way of organizing time. January 1st will simply be another day from the standpoint of the earth and the sun. Neither China’s nor Canada’s problems will have solved themselves when markets reopen in 2016, but from the perspective of investors a new year gives us a chance to reframe and contextualize opportunities and risks in the markets. The surprises of 2015 will now be part of the fabric of 2016, new stories will come to dominate investor news and new narratives will popup to explain the terrain for Canadians.

So when we do get to our first trades in January, what kind of world will we be looking at? What opportunities and risks will we be considering?

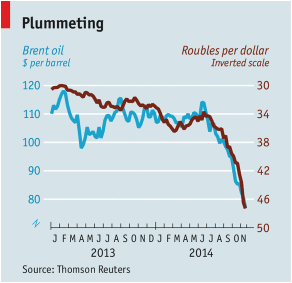

The risks are very real. After a steep sell off in Canada we may be tempted to think that the Canadian market is cheap and ideal for investment. I’ve had more than one conversation with market analysts that suggests that things could change very quickly. Cheap oil, a cheap dollar and rising consumer spending to the south could all spell big opportunities for Canada.

But this argument has another side. Since 2007, despite lots of volatility, the TSX has barely moved. In February of 2007 the TSX was at 13083, and at close on Friday last week the market was 13024. The engines of Canada’s economic growth from the past few years have largely stalled. Commodity prices have fallen and may be depressed for some time, with exports of everything from timber to copper and iron being reduced significantly. Oil too, as we have previously said, is unlikely to bounce back quickly. Even if oil recovers to around $60, the growth of cheap shale energy will likely eclipse Canadian tar sands, and will not be enough to restart some previously canceled projects.

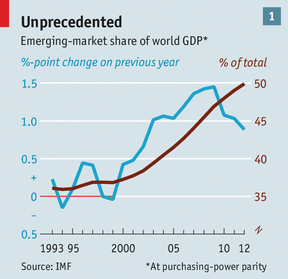

Similarly, the Emerging Markets have been badly beaten this year, driving down the MSCI EM Index to levels well below the early year highs. But those levels also reflect the ongoing and worrying trend. The MSCI EM Index (a useful tool to look at Emerging Markets) isn’t just lower than it’s previous year’s high, it’s lower than it was back in 2011, and in 2007. In other words we’ve yet to surpass any previous highs, and when faced with the reality that the United States will likely be raising rates for the next few years, the EM will likely continue to lose investments to safer and higher yielding returns in the United States.

In an ideal world a new year would be a chance to wipe the slate clean, mark the previous year’s failings as in the past and move forward. But what drives markets (in between bouts of panic selling and fevered buying) are the fundamentals of economies and the companies within them. So as celebrations of December 31st give way to a return of regular business hours, investors should temper any excitement they have about last year’s losers becoming the new year’s winners. The ground has shifted for the Canadian economy, as it has for much of the Emerging Markets. Weaknesses abound as debt levels are at some of their highest and global markets have largely slowed.

It is a core belief that investors should seek “discounts”. The old adage is buy low and sell high. That advice holds, but investors should be wary as they walk the tightrope between discounted opportunities, and realistic market danger. Faced with a world filled with worrying trends and negative news an even handed and traditional approach to investments should be at the top of every investor’s agenda for 2016.