Earlier this year we wrote that Russia’s economy was fundamentally weaker than Europe’s and that their decision to start a trade war in retaliation for economic sanctions over the Ukraine would hurt Russia far more than Europe. As it happened Russia has suffered that fate and had a helping more. The collapsing price of oil was a mortal wound to the soft underbelly of the Russian economy, leading to a spectacular collapse in the value of the Ruble and an estimated 4.5% contraction in their economy for 2015.

Earlier this year we wrote that Russia’s economy was fundamentally weaker than Europe’s and that their decision to start a trade war in retaliation for economic sanctions over the Ukraine would hurt Russia far more than Europe. As it happened Russia has suffered that fate and had a helping more. The collapsing price of oil was a mortal wound to the soft underbelly of the Russian economy, leading to a spectacular collapse in the value of the Ruble and an estimated 4.5% contraction in their economy for 2015.

The Ruble’s earlier decline this year had already made the entire Russian stock market less valuable than Apple Computers, but as the price of Brent oil continued to slide below $60 (for the first time since 2008) investors began to loose confidence that Russia could do much to prop up the currency, prompting an even greater sell-off. That led to an unprecedented hike in the Russian key interest rate by its central bank, moving it from 10.5% to 17% yesterday. Moves like that are designed to reassure investors, but typically they only serve to ensure a full market panic. The Ruble, which had started the year at about 30 RUB per dollar briefly dropped to 80 before recovering at around 68 to the dollar by the end of trading yesterday.

Cheap oil seems to be recasting the economic story for many countries and millions of people. The Financial Times observes that oil importing emerging markets stand to be big winners in this. Dropping the cost of manufacturing and putting more money in the pockets of the growing middle class should continue to help those markets. The same can be said of the American consumer, who will be benefiting from the sudden drop in gas and energy prices.

Losers on the other hand seem easy to spot and piling up everywhere. Venezuela is in serious trouble, so is Iran and the aforementioned Russia. Saudi Arabia should be okay for a while, as it has significant foreign currency reserves, but as the price drops other member states of OPEC will likely howl for a change in tactic. But along with the obvious oil producing nations, both the United States and Canada will likely also be victims, just not uniformly.

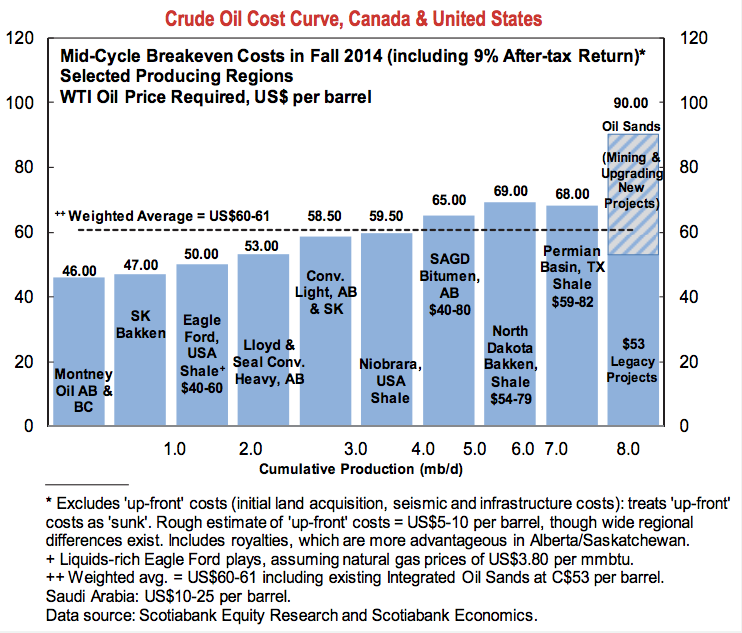

Manufacturers may be breathing a sigh of relief in Ontario, but Canadian oil producers are sweating it big. Tar sand oil requires lots of refining and considerable cost to extract. Alberta oil sands development constitute some of the most expensive projects around for energy development and a significant drop in the price of energy, especially if it is protracted, could stall or erase some future investments. This is especially true of the Keystone Pipeline which many now fear isn’t economically viable, in addition to being environmentally contentious.

Saudi Arabia has continued to allow the price of oil to fall with the intention of hurting the shale producers in the United States. This price war will certainly claim some producers in the US, but it will difficult to know at which point that market will be effectively throttled. Certainly new projects will likely slow down but the continued improving efficiency of the fracking technology may make those producers more resilient to cheap energy.

But there is one more potential victim of the falling price of oil. That could be all of us. I, like many in the financial field, believe that cheap energy will enormously benefit the economy. But our biggest mistakes come from the casual confidence of things we assume to be true but prove not to be. A drop in energy should help the economy, but it doesn’t have to. If people choose not to spend their new energy windfall and save it instead, deflationary pressure will continue to grow. As I’ve previously said, deflation is a real threat that is often overlooked. But even perceived positive forms of deflation, like a significant reduction in the price of oil, can have nasty side effects. The loss to the global economy in terms of the price of oil is only beneficial if that money is spent elsewhere and not saved! For now confidence is that markets will ultimately find the dropping price of oil helpful to global growth, regardless of the early losers in the global price war for oil.