While curves continue to be bent and geopolitics continues to become both more silly and more frightening than anyone ever thought possible, populations of countries remain unsure and troubled about whether they have made the correct choice of trying to beat COVID-19 through lockdowns and aggressive social distancing. Predictions of economic doom run rampant, ranging from serious recessions to the potential for a depression not unlike that of the 1930s.

With nothing to do but sit at home and twiddle our thumbs, either letting our house fall into total chaos or be cleaner than ever (a battle largely determined by how tired I am and how many cookies my kids have had) making predictions and considering alternative paths to beating this virus occupy considerable mental space. How will we know whether the unprecedented steps we have taken were the correct steps to take? What dark and strange future awaits us on the other side? I’m here to put your mind at ease, both because this situation is not unprecedented, and because we may not have had any other choice.

Let’s start with precedent. In an interview with Australian talk show host John Anderson, historian Niall Ferguson mused that future historians would regard our response to the pandemic as a mistake. This is an understandable position given the continued uncertainty around much of the virus. Is it very dangerous? Does it only affect the elderly? Do we even know how many people have it? Undoubtedly the biggest threat from the virus is what we don’t know about it.

But the assumption that it is the lockdown that is hindering the economy are belied by the available evidence. For instance, Sweden has been a focus through much of this since it hasn’t locked down its economy fully. Though schools have been closed and people have been advised to socially distance, restaurants and bars have been allowed to remain open. But estimates are that business has dropped off dramatically. In fact, despite having more of their economy not under lock and key does not seem to have materially changed the country’s fate, with early economic predictions of the contractions expected to be around 7% of GDP. That’s in line with other European neighbors.

In a similar story, the state of Georgia’s efforts to open early were met with disappointing results. People, worried about a virus that has a surprising amount of variability and high level of infection simply don’t want to go axe throwing, drink in crowded bars and go bowling. With the virus still being prevalent the thing restricting economic activity is not the lockdown, it is the virus.

Much is being made of the 1918 Spanish Influenza and this is an understandable place to jump to; the last memorable global pandemic that seriously interrupted the lives of people. Economists studying that event have concluded that “cities that implemented early and extensive non pharmaceutical interventions (like physical distancing and forbidding large gatherings) suffered no adverse economic effects over the medium term. On the contrary, cities that intervened earlier and more aggressively experienced a relative increase in real economic activity after the pandemic subsided.” Other lessons drawn from the 1918 pandemic were not to give up too early on restrictions and that a multi-layered approach was what worked best.

But precedent exists much farther back. In Daniel Defoe’s work “Memories of a Plague Year”, a book once thought to be a work of fiction, but now believed to be based on the diaries of Defoe’s uncle who lived through the last great plague in London of 1665, all the hallmarks of our modern response can be found in that bygone era. Wealthier people escaping to their cottages? From Defoe: “It is true, a vast many people fled, as I have observed, yet they were chiefly from the West End of the Town; and from that we call the Heart of the City, that is to say, among the wealthiest of the people.”

How about our daily obsession to see if the curve is “being bent” and watching the infection rates? In 1665 concern over the spread of the plague (called the distemper) caused people to look “towards the east end of town; and the weekly Bills showing the Increase of Burials in St. Giles’s Parish…the usual number of burials in a week, in the parishes of St Giles’s in the fields, and St. Andrew’s Holborn, were from 12 to 17 or 19 each, few more or less; but from the time that the Plague first began in St. Giles’s parish, it was observed that the ordinary burials increased in number considerably.”

What of economic activity? It has been estimated that somewhere between 25%-30% of the economy has been restricted, but in 1665 “All Master Workmen in Manufactures; especially such as belonged to Ornament, and the less necessary parts of the people’s dress, cloths, and furniture for houses; such as Riband Weavers, and other Weavers; Gold and Silverlace-makers, and…Seemstresses, Milleners, Shoemakers, Hat-makers and Glove Makers: also Upholserers, Joiners, Cabinet-Makers, Looking Glass Makers; and innumerable trades which depend upon such as these; I say the Master Workmen in such , stopped their work, dismissed their journeymen and workmen, and all their dependents.” You get the idea. The economy shut down.

Worried that people believe lunatic conspiracies, burning 5G towers across the world? Conspiracies depend on context, and in 1665 there were plenty of people pushing nonsense ideas, including astrologers spinning stories, and a host of charlatans that were “a worse sort of deceivers…for these petty thieves only deluded them to pick their pockets, and get their money; in which their wickedness, whatever it was, lay chiefly on the side of the deceiver’s deceiving, not upon the deceived.” Amulets, charms and potions, signs of the zodiac and any number of other bogus ways to defend the person from the plague were sold widely to a gullible public desperate for protection.

But what of the predictions we keep hearing about? That life will be forever changed by the events we’re living through? While I have a great deal more to say about the nature of prognostication, I’ll keep my comments here brief. In general history shows that humans don’t tend towards radical changes following big, but temporary upheavals. Instead, crises like the one we are living through emphasize existing weaknesses within the society.

But what of the predictions we keep hearing about? That life will be forever changed by the events we’re living through? While I have a great deal more to say about the nature of prognostication, I’ll keep my comments here brief. In general history shows that humans don’t tend towards radical changes following big, but temporary upheavals. Instead, crises like the one we are living through emphasize existing weaknesses within the society.

In his book “The Great Leveler: Violence and the History of Inequality from the Stone Age to the Twenty First Century”, author Walter Scheidel points out that during the first big years of the plague, which came in the 1300s, the high death rates from plague changed the existing relationship between land and labour. For a society of feudal serfs this meant that serfs could demand wages from their lords, and the lords felt compelled to pay lest their lands remain fallow. Behaviours changed too, but only in as much that hedonism and charity increased to match the scale of the devastation people were living through. In response to our own situation charity, certainly that sanctioned by the government, has been widespread. Whether we might count the volume of baking as a form of hedonism will be left to others to decide.

But we should largely discount predictions of an economy collapsing and a society that will not wish to do anything ever again. Cruise ships, house sales, air traffic and eating out will return as confidence returns, though there will be losses along the way. But the real damage to the economy, and the people within it, will likely remain along lines that have already been established. As fewer Canadians work in good manufacturing jobs and more work in the service sector, earning marginal wages, they will continue to take the brunt of the economic hit of the lockdown. Just as likely will be that efforts to decouple production from China will lead to greater automation in manufacturing. In other words, more of the ingredients at the heart of the widening inequality gap.

The response to the coronavirus feels novel, to us. But in the scheme of history there doesn’t seem to be many other viable options. Life will return to normal not when the lockdowns are lifted, but when the virus is gone. But if we’re going to do something with our time it would be better spent figuring out how we’re going to address a worsening crisis of inequality, or brace ourselves for the next round of populist agitation.

Information in this commentary is for informational purposes only and not meant to be personalized investment advice. The content has been prepared by Adrian Walker from sources believed to be accurate. The opinions expressed are of the author and do not necessarily represent those of ACPI.

The temptation to assume that everything is about to go wrong is therefore not the most far-fetched possibility. Investors should be cautious because there are indeed warning signs that the economy is softening and after ten years of bull market returns, corrections and recessions are inevitable.

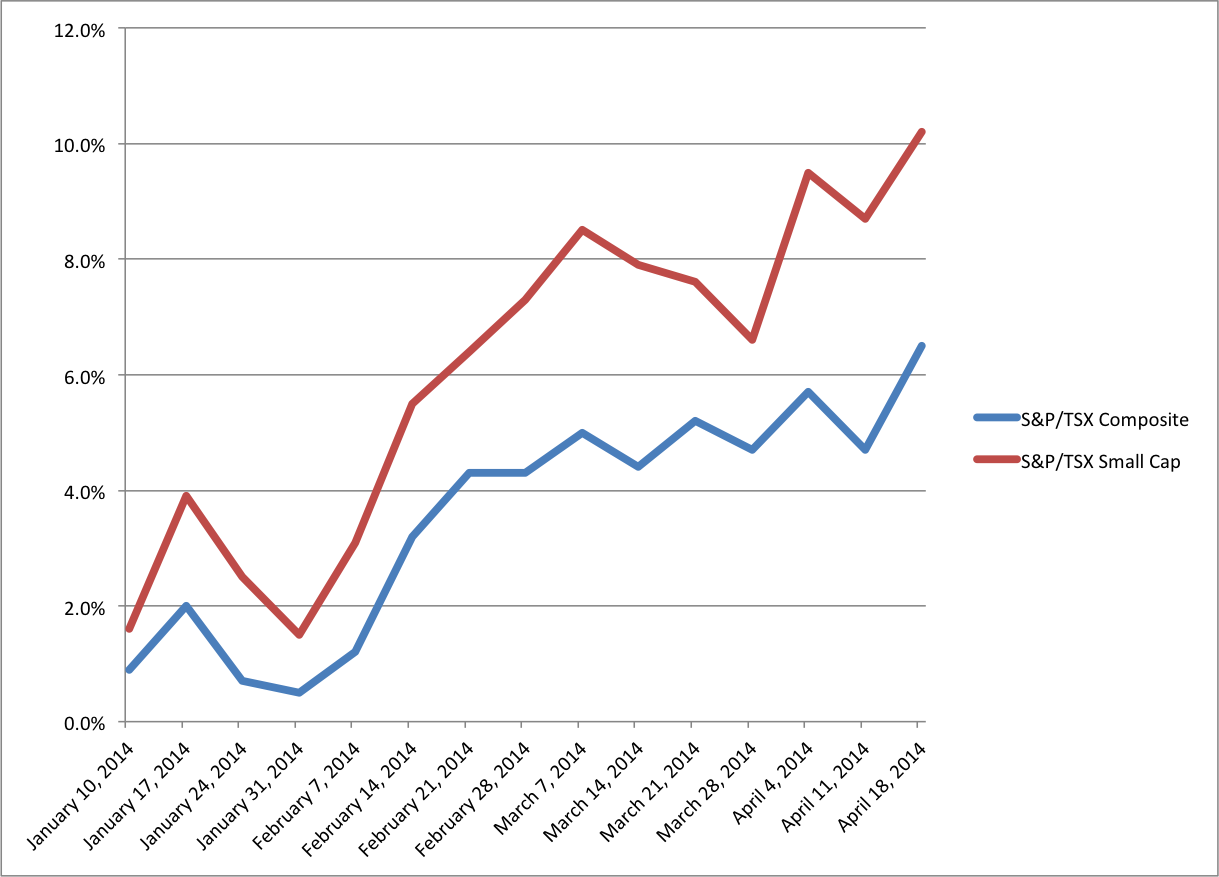

The temptation to assume that everything is about to go wrong is therefore not the most far-fetched possibility. Investors should be cautious because there are indeed warning signs that the economy is softening and after ten years of bull market returns, corrections and recessions are inevitable. The first (and so far only) good day in the markets for 2016 shouldn’t go by without instilling some hope in us investors. The latter half of 2015 and the first weeks of 2016 have many convinced that the market bull is thoroughly dead, having exited stage left pursued by a bear (appropriate for January). The toll taken by worsening news out of China, falling oil, and the rising US dollar have left markets totally exhausted and despondent. But is the bull dead, or just mostly dead? Because there’s a big difference between all dead and mostly dead. In other words, is there a case to be made for a resurgence?

The first (and so far only) good day in the markets for 2016 shouldn’t go by without instilling some hope in us investors. The latter half of 2015 and the first weeks of 2016 have many convinced that the market bull is thoroughly dead, having exited stage left pursued by a bear (appropriate for January). The toll taken by worsening news out of China, falling oil, and the rising US dollar have left markets totally exhausted and despondent. But is the bull dead, or just mostly dead? Because there’s a big difference between all dead and mostly dead. In other words, is there a case to be made for a resurgence?

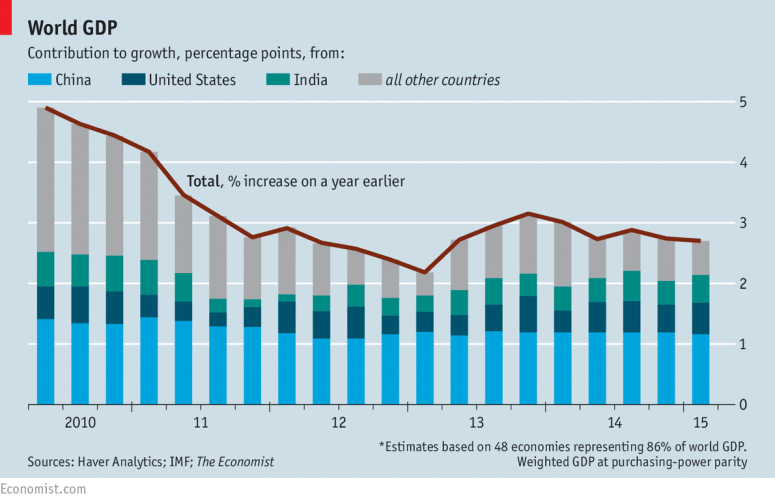

Since 2008 governments the world over have tried to fight the biggest banking collapse since the great depression with modest success. Eight years on and you would be loath to say that the world has turned a corner, ushering in a return of unrestrained economic growth.

Since 2008 governments the world over have tried to fight the biggest banking collapse since the great depression with modest success. Eight years on and you would be loath to say that the world has turned a corner, ushering in a return of unrestrained economic growth.