If you’re looking for some good reading Google “Canadian Housing Bubble” and you could fill a library with the amount of material available. There isn’t a week that goes by without some new article somewhere screaming with alarm about Canada’s precarious and overvalued housing market. I’ve written many myself, but in conversation almost everyone admits that regardless of the danger nothing seems to abate the growth in home values.

This defying of financial gravity gives ammunition to those that doubt there is any real risk at all. The combination of low interest rates, willing banks, rising prices and an aggressive housing market has given a veneer of stability to an otherwise risky situation. Combined with the “sky is falling” talk about the house prices and it is easy to understand why many simply accept, or outright dismiss, the growing chorus of concerns about house prices.

Nissam Taleb’s book “The Black Swan” highlighted that negative Black Swan events tended to be fast, like 2008, while positive Black Swan events tended to be slow moving, like the progressive improvement in standards of living since the end of the Second World War. But it would be fair to say that creating a negative event requires a prolonged period of danger creep, a period where a known danger continues to grow but remains benign, fooling many to believe that there isn’t any real danger at all.

Nissam Taleb’s book “The Black Swan” highlighted that negative Black Swan events tended to be fast, like 2008, while positive Black Swan events tended to be slow moving, like the progressive improvement in standards of living since the end of the Second World War. But it would be fair to say that creating a negative event requires a prolonged period of danger creep, a period where a known danger continues to grow but remains benign, fooling many to believe that there isn’t any real danger at all.

I would argue we are living in such a period now. The housing market is continuing to grow more precarious and many Canadians are finding that their own financial well being is connected to their home’s appreciating value. Between large mortgages and HELOCs, Canadians are deeply indebted and need their home prices to continue to inflate to offset the absurd level of borrowing that is going on.

As an example of how the “danger creeps” have a look at this article from last week’s Globe and Mail which highlights a young couple living in Mississauga with a burdensome debt and an unexpected pregnancy. They are classified as some of the “most indebted” of Canadians; house rich and cash poor. By their own estimates they are over budget every month and 100% of one of their incomes goes exclusively to pay the mortgage, stressful as that is they aren’t worried. It may seem irresponsible on their part to buy such a home, but they couldn’t do it if there weren’t many others complicit in making such a bad financial arrangement. Between lax rules from the government, a willing lending officer and well intentioned families that help out, it turns out that creating a financially fragile family takes a village.

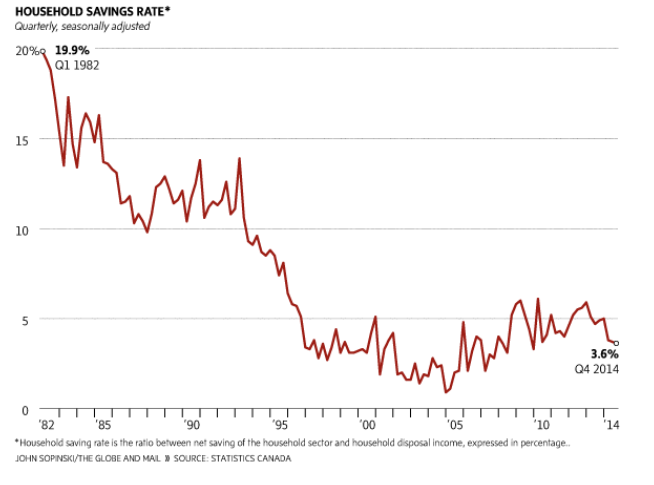

A nation of debtors is a vulnerable one indeed. I’ve often said that financial strength comes through being able to withstand financial shocks, and this is exactly where Canadians are falling short. It’s the high debt load and minimal savings (and that these two issues are self-reinforcing) that make Canadians vulnerable. A change in the economic fortunes would force many Canadians to deleverage and in the process would inflict further damage to the economy and likely many homes onto the market.

Such an event is strictly in the “uncharted seas” sector of the economy. No one has a clear idea what it would take to shift the housing sector loose, or what would happen once it did. And that’s just the unknown stuff. With interest rates at an all time low it would also only take a small increase in the interest rate (say 2%) to bump up many people out of their once affordable mortgage and into unaffordable territory.

That’s the problem with slow growing danger, it has a glacial pace but when it arrives it is already too large to be dealt with easily. In one of my favorite movies, the Usual Suspects, Kevin Spacey utters the line “The greatest trick the devil ever pulled was convincing the world he didn’t exist”. That’s something we should all be wary of, the longer the housing market stays aloft the more convinced we become that not only is it not dangerous, but that there was never any danger at all.