Its traditional that the end of a year should stimulate some reflection on the past and the future, and so in the spirit of tradition I thought I’d take some time to look over some of the stranger and more surprising aspects of 2021.

China

While 2021 brought the pandemic *closer* to an end through the distribution of vaccines, markets underwent some fairly dramatic reversals over the course of the year. For instance China looked to be the principal economy in January. Following its own strict enforcement of Covid restrictions and solid economic performance, China seemed to be an earlier winner by the beginning of 2021, and set to enjoy robust growth through the year.

By March the tide was shifting however. China’s leader, Xi Jinping, proved to be every bit committed to his past comments about protecting and strengthening the CCP over free market concerns. Several billionaires, notably Jack Ma the founder of Alibaba, disappeared for long periods before reemerging only to publicly announce that they would be stepping down from their roles.

However, even while China was shaking down its billionaires and upsetting foreign nations, a new economic threat appeared in the form of a housing bubble looking ready to burst. Evergrande, one of the country’s largest property developers announced that it could not finance its debt anymore and looked likely to default. This news was unwelcome for markets, but for China hawks it fit their long standing belief that China’s strength has been built on a mountain of unsustainable debt, with property one of the most vulnerable sectors of the economy.

The finer points of China’s housing market are too nuanced to get into here, but it’s enough to know that the property bubble in China is large, built on sizeable debt and could take some time to deflate (if it does) and no one is sure what the fallout might be. Combined with China’s ongoing policy of “Covid Zero” – an attempt to eradicate the virus as opposed to learning to live with and manage it, we head into 2022 with China now a major outlier in the Asian region.

Inflation

Inflation was probably the other most discussed and worrying trend of 2021. Initially inflation sceptics seemed to win the argument, as central banks rebuffed worries over rising prices and described inflation as transitory. That argument seemed to wane as we entered late Q3 and prices were indeed a great deal higher and didn’t seem to be that “transitory” anymore. Inflation hawks took a victory lap while news sites began to fill up with worrying stories about rising prices on household goods.

The inflation story remains probably the worst understood. Inflation in Canada, as in other Western nations has been going on for sometime, and its effects have been under reported due to the unique nature of the CPI. But some of the concern has also been overwrought. Much of the immediate inflation is tied to supply chains, the result of “Just-in-time” infrastructure that has left little fat for manufacturers in exchange for lower production costs. Bottlenecks in the system will not last forever and as those supply chains normalize that pressure will recede.

The other big pressure for inflation is in energy costs, but that too is likely to recede. Oil production isn’t constrained and prices, while higher than they were at the beginning of the pandemic are lower than they were in 2019. In short, many of the worries with inflation will not be indefinite, while the issues most worrying about inflation, specifically what it costs to go to the grocery store, were important but underreported issues before the pandemic. Whether they prove newsworthy into the future is yet to be seen.

*Update – at the time of writing this we were still waiting on more inflation news, and as of this morning the official inflation rate for the US over the past year was 7%. Much of this is still being chalked up to supply chains squeezed by consumer demand. An unanswered question which will have a big impact on the permanence of inflation is whether this spills into wages.

Housing and Stocks – Two things that only go up!

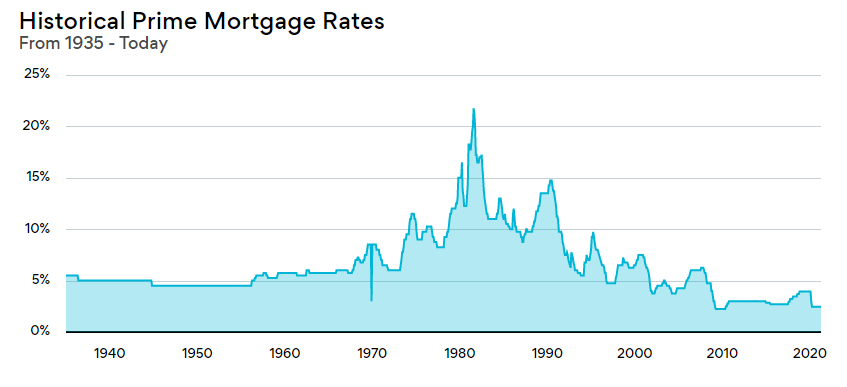

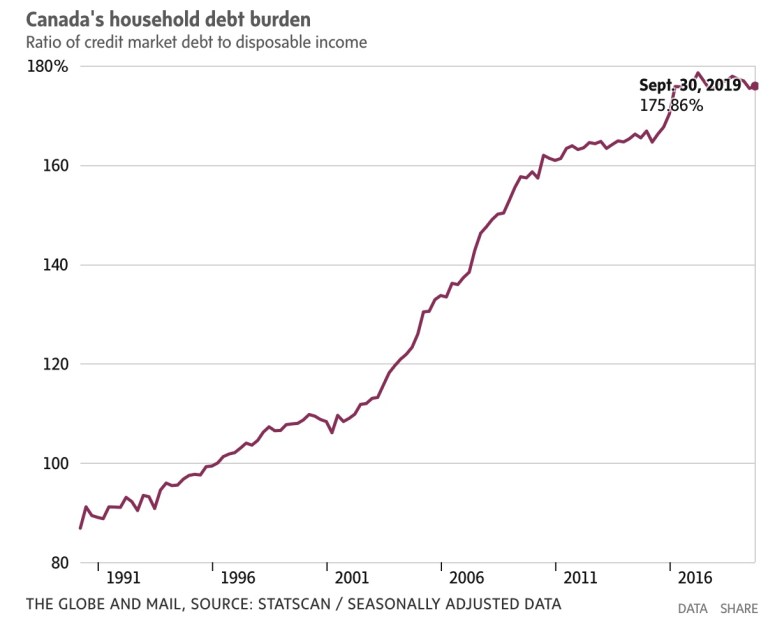

If loose monetary policy didn’t make your groceries more expensive, does that mean that central bankers were right not to worry about inflation distorting the market? The answer is a categorical “No”. As we have all heard (endlessly and tediously) housing prices have skyrocketed across the country, particularly in big cities like Toronto and Vancouver, but also in other countries. The source of this rapid escalation in prices has undoubtedly been the historically low interest rates which has allowed people to borrow more and bid up prices.

In conjunction with housing, we’ve also seen a massive spike in stock prices, with even notable dips lasting only a few days to a couple of weeks. The explosion of new investors, low-cost trading apps, meme-stocks, crypto-currencies, and now NFTs has shown that when trapped at home for extended periods of time with the occasional stimulus cheque, many people once fearful of the market have become quasi “professional” day traders.

Market have been mercurial this past year. Broadly they’ve seemed to do very well, but indexes did not reveal the wide disparities in returns. Last year five stocks were responsible for half the gains in the S&P 500 since April, and for the total year’s return (24%), Apple, Microsoft, Alphabet Inc, Tesla and Nvidia Corp were responsible for about 1/3 of that total return. This means that returns have been far more varied for investors outside a tightly packed group of stocks, and also suggests markets remain far more fragile than they initially appear, while the index itself is far more concentrated due to the relative size of its largest companies.

Suspicious Investment Practices In addition to a stock market that seems bulletproof, houses so expensive entire generations worry they’ve been permanently priced out of the market, the rapid and explosive growth of more dubious financial vehicles has been a real cause for concern and will likely prompt governments to begin intervening in these still unregulated markets.

Crypto currencies remain the standout in this space. Even as Bitcoin and Etherium continue to edge their way towards being mainstream, new crypto currencies trading at fractions of the price, have gotten attention. Some have turned out to be jokes of jokes that inadvertently blew up. Others have been straight-up scams. But all have found a dedicated group of investors willing to risk substantial sums of money in the hope of striking it rich.

NFTs, or non-fungible tokens have also crept up in this space, making use of the blockchain, but instead of something interchangeable (like a bitcoin for a bitcoin, i.e. fungible) these tokens are unique and have captured tens of thousands, sometimes hundreds of thousands of dollars for unique bits of digital art. Like cryptocurrencies, much of the value is the assumed future value and high demand for a scarce resource. However, history would show that this typically ends poorly, whether its housing, baseball cards or beanie babies.

Lastly, there has been a number of new investment vehicles, the most unusual of which is “fractional ownership”. The online broker Wealth Simple was the first to offer this in Canada and it has been targeted to younger investors. The opportunity is that if your preferred stock is too expensive, you can own fractions of it. So if you wanted to invest in Amazon or Tesla, two stocks that are trading at (roughly) $3330 and $1156 respectively at the time of writing, those stocks might be out of reach if you’re just getting started.

This is a marketing idea, not a smart idea. The danger of having all your assets tied up in one investment is uncontroversial and well understood. The premise behind mutual funds and exchange traded funds was to give people a well-diversified investment solution without the necessity of large financial position. The introduction of fractional ownership ties back to the market fragility I mentioned above, with younger investors needlessly concentrating their risk in favour of trying to capture historic returns.

The End

For most investors this year was largely a positive one, though markets went through many phases. But while the pandemic has remained the central news story, the low market volatility and decent returns has kept much of us either distracted or comfortable with the state of things. And yet I can’t help but wonder whether the risks are all the greater as a result. Many of these events, the large returns in an ever tightening group of stocks, the growth of investors chasing gains, the sudden appearance of new asset bubbles and the continued strain on the housing market and household goods add up to a worrying mix as we look ahead.

Or maybe not. Market pessimists, housing bears, and bitcoin doubters have garnered a lot of attention but have a bad track record (I should know!) Many of the most pressing issues feel as though they should come to a head soon, but history also teaches us that real problems; big problems that take years to sort out and lead to substantial changes are often much longer in the making than the patience of their critics. The test for investors is whether they can stand by their convictions and miss out on potential windfalls, or will they become converts right as the market gives way?

Next week, we’ll examine some of the potential trends of 2022.

Real estate remains at the heart of the Canadian economic story for the last 20 years. Appreciating housing prices are the chief source for growth in Canadian families’ net worth. Borrowing to buy houses and borrowing against home equity remain our chief sources of debt. Our politics revolves around the tension of needing more housing in certain highly desirable areas while preserving those areas from over development. That dynamic has revolved around a status quo that seemed to have no conceivable end. The pandemic may have radically altered the Canadian real estate landscape regardless of how people feel about it or what they want. Whether we can walk back changes of this magnitude remains very much unknowable. For now we can only watch the changes our society and economy are undergoing and hope that what we are witnessing will be for the best, those changes that have happened, and those yet to come.

Real estate remains at the heart of the Canadian economic story for the last 20 years. Appreciating housing prices are the chief source for growth in Canadian families’ net worth. Borrowing to buy houses and borrowing against home equity remain our chief sources of debt. Our politics revolves around the tension of needing more housing in certain highly desirable areas while preserving those areas from over development. That dynamic has revolved around a status quo that seemed to have no conceivable end. The pandemic may have radically altered the Canadian real estate landscape regardless of how people feel about it or what they want. Whether we can walk back changes of this magnitude remains very much unknowable. For now we can only watch the changes our society and economy are undergoing and hope that what we are witnessing will be for the best, those changes that have happened, and those yet to come.

But what of the predictions we keep hearing about? That life will be forever changed by the events we’re living through? While I have a great deal more to say about the nature of prognostication, I’ll keep my comments here brief. In general history shows that humans don’t tend towards radical changes following big, but temporary upheavals. Instead, crises like the one we are living through emphasize existing weaknesses within the society.

But what of the predictions we keep hearing about? That life will be forever changed by the events we’re living through? While I have a great deal more to say about the nature of prognostication, I’ll keep my comments here brief. In general history shows that humans don’t tend towards radical changes following big, but temporary upheavals. Instead, crises like the one we are living through emphasize existing weaknesses within the society.