To many Canadians the CPP is something that you simply receive when you turn 65, (or 70, or 60, depending on when you want or need it) with little consideration for how the program works or is run. That’s too bad because the CPP is successful, enlightening and puts its American counterpart, Social Security, to shame.

You’ve probably heard American politicians decrying the state of Social Security, claiming that it is broken and will one day run out of money. That’s a frightening prospect for those who will depend on it in the future. Social Security is a trust that buys US debt, and its use of US Treasuries (low risk debt issued by the US government) is crippling that program and even puts it at odds with attempts to improve government financial health (it’s more complicated than this, but it’s a useful guide). In comparison the CPP isn’t bound by the same restrictions, and operates as a sovereign wealth fund.

A sovereign wealth fund is simply a fancy way to describe a program that can buy assets, which is exactly what the CPP does. The Canada Pension Plan may be larger and more elaborate than your RRSP, but it can look very similar. The CPP has exposure to Canadian, American, European and Emerging Market equity. It invests in fixed income both domestically and abroad, and while it may also participate in private equity deals (like when the CPP bought Neiman Marcus) in essence the investments in the CPP are aiming to do exactly what your RRSP does.

The big lesson here is really about risk though. The CPP is one of the 10 largest pension plans in the world. It’s wildly successful and is run in such a way as to be sustainable for the next 75 years. The same cannot be said for Social Security. But by taking the “safest” option Social Security is failing in its job and will run out of money by 2033. But by buying real assets and investing sensibly the CPP is far more likely to survive and continue to thrive through all of our lifetimes.

What’s also notable is what the CPP isn’t trying to do. It isn’t concentrated in Canada. It doesn’t need to get a substantial rate of return, and it doesn’t need every sector to outperform. It needs consistent returns to realize its goals, and that’s how it’s positioned. By being diversified and not trying to time the market, the CPP finds success for all Canadian investors.

I’ve said in conversation that if there was an opportunity to invest directly in the CPP I would take it. However until then the best thing investors can do is take the CPPs lessons to heart!

It may come as a real surprise to many Canadians but we have never been a strong economy. From the standpoint of most of the world we barely even register as an economic force. Yet a combination of global events have conspired to make Canadians far more comfortable with a greater sense of complacency about the tenuous position of Canada’s economic might.

Don’t get me wrong. It’s not that Canada and Canadians aren’t wealthy. We are. But having a high standard of living is largely a result of forces that have been as much beyond our control as any particular economic decisions we’ve made.

Consider for a second the size of Canada’s economy in relation to the rest of the world. While we may be one of the G8 nations, the Canadian economy only accounts for about 2-3% of the global GDP, and has (according to the IMF) never been higher than the world’s 8th largest economy. Even with the growth in the oil fields Canada hasn’t contributed more than 2.8% to global growth between 2000 and 2010.

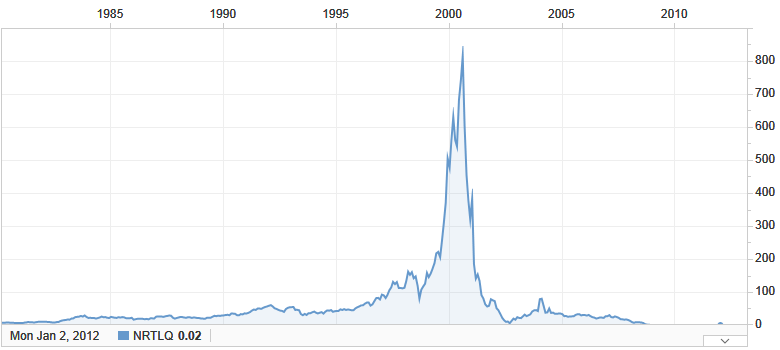

The Rise and Fall of Nortel Stock.

It’s not just that Canada isn’t a big economy, we’re also a narrow one. In the past we’ve looked at how the TSX is dominated by only a few sectors, but the investable market can play even crueler tricks than that. If you can remember the tech boom and the once great titan Nortel, you might only remember their fall from grace, wiping out 60,000 Canadian jobs and huge gains in the stock market. What you should know is that as companies get bigger in the TSX they end up accounting for an ever greater proportion of the index. At its peak Nortel accounted for 33% of the S&P/TSX, creating a dangerous weighting in the index that adversely affected everyone else and skewed performance.

Similarly much of Canada’s success through the 90s and early 2000s had as much to do with a declining dollar. While it may be the scourge of every Canadian tourist, it is an enormous benefit to Canadian industry and exports. Starting in 2007 the Canadian dollar began to gain significantly against the US dollar. This sudden gain in the dollar contributed to Canada’s relative outperformance against every global market. The dollar’s rise was also closely connected to the rise in the value of oil and the strong growth in the Alberta oil sands.

This mix of currency fluctuations, oil revenue and narrow investable market has created an illusion for Canadian investors. It has created the appearance of a place to invest with greater strength and security than is actually provided.

Some studies have shown that the average Canadian investor will have up to 65% of their portfolio housed in Canadian equities. This is insane for all kinds of obvious reasons. Obvious except for the average Canadian. This preference for investing heavily into your local economy has been coined “home bias” and there is lots of work out there for you to read if you are interested. But while Canadians may be blind to the dangers of over contributing to their own markets, it becomes obvious if you recommend that you place 65% of your money in the Belgium or the Swedish stock market. However long Canada’s relative market strength lasts investors should remember that all things revert to the mean. That’s a danger that investors should account for.

Falling inflation, terrible economic news and a general sense of dread for the future seems to have once again become the primary descriptive terms for Europe. Earlier this year things seemed to have improved dramatically for the continent. On the back of the German economic engine much of the concern about the EU had been receding. 2013 had been a good year for investors and confidence was returning to the markets. Lending rates were dropping for the “periphery nations” like Portugal, Greece and Ireland, giving them a fighting chance at borrowing at affordable rates. But first came the Ukrainian/Russia problem which caused a great deal of geo-political instability in the markets. Then came October.

I don’t know if Mario Draghi cries himself to sleep some nights, but I wouldn’t blame him. Despite the best efforts of the ECB, Europe looks closer to being in a liquidity trap then ever. Borrowing rates are not just low, they’re negative, with the ECB charging banks to now to deposit money with them. October also ushered in a string of bad news. For Germany, easily the biggest part of the Eurozone’s hopes for an economic recovery, sanctions against Russia have hurt the manufacturing sector. Germany began the month announcing a steep and unexpected decline in manufacturing of 5.7% in August, the biggest since 2009. This news was followed by criticisms of Germany’s government for not doing more infrastructure investment and being too obsessed with their strict budget discipline. Yesterday 25 banks in the Eurozone failed a stress test, a test that was meant to allay fears about the health of the financial sector.

For Europe then things look bad and even if the situation corrects itself over the next few months (sudden shifts in the economy may not always be permanent and can bounce back quickly) the concerns over Europe’s future will likely undermine any efforts by the ECB to properly stimulate the broad economy and encourage investment on a mass scale. By comparison it looks like the United States is having a party.

The coming months could be interesting for investors as we return to a time where once again focus is on the US as the world’s primary economy. The concerns of 2008, that the American consumer was done, the country had seen its best days and its corporations would never recover seem far fetched now. Worries over hyper-inflation are as distant as a the never arriving (but inevitable) rate hike from the Federal reserve. Worries about Great Depression levels of unemployment are problems of other nations, not the US with its now enviable 5.9%, now encroaching on full employment. Old villains seem vanquished and even Emerging Markets, long thought to be entering their own golden era, are now taking a back seat to the growing opportunities coming out of the US.

Investors should sit up and take note. It’s possible that the best is still yet to come for the US markets, and if market conditions continue to improve this bull market could prove to be a long one.

If 2008 was the financial apocalypse it is often written about, it is a zombie apocalypse for sure. It’s victims don’t die, they are merely resurrected as an infected horde threatening to infect the other survivors. And no matter how many times you think the enemy has been slain, it turns out there is always one more in a dark corner ready to jump out and bite you.

This past month has seen the return of the zombie of deflation, a menacing creature that has spread from the worst ravaged economies in Europe into the healthier economies of the Eurozone. Deflation is like the unspoken evil twin that lives in the attic. I’ve yet to meet an analyst, portfolio manager or other financial professional that wants to take the threat seriously and doesn’t insist that inflation, and with it higher interest rates are just around a corner.

The eagerness to shrug-off concerns about deflation may have more to do with the reality that few know what to do when deflation strikes. Keeping deflation away is challenging, but not impossible, and it has been the chief job of the central banks around the world for the last few years. But like any good zombie movie, eventually the defences are overrun and suddenly we are scrambling again against the zombie horde.

This. Except it’s an entire economy and it won’t go away.

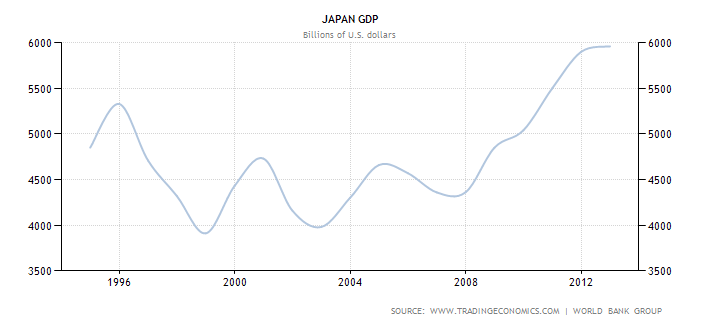

In the late 1990s, Japan was hit with deflation, and it stayed in a deflationary funk until recently. That’s nearly 20 years in which the Japanese economy didn’t grow and little could be done to change its fate. The next victim could be Europe, whose official inflation numbers showed a five year low in September of 0.3%. That’s across the Eurozone as a whole. In reality countries like Greece, Spain and Portugal all have negative inflation rates and there is little that can be done about it. Pressure is mounting on Germany to “do more”, but while the German economy has slowed over the past few months it is still a long way from a recession and there is little appetite to boost government spending in Germany to help weaker economies in the EU.

Japanese GDP from 1994-2014

Across the world we see the spectre of zombie deflation. Much has been made of China’s slowing growth numbers, but perhaps more attention should be paid to its official inflation numbers, which now sit below 2% and well below their target of 4%. The United States, the UK, the Eurozone and even Canada are all below their desired rates of inflation and things have gotten worse in this field over the summer.

For investors this is all very frustrating. The desire to return to normalcy (and fondly remembering the past) is both the hallmark of most zombie films and the wish of almost every person with money in the market. But as The Walking Dead has taught us, this is the new normal, and investing must take that into account. Deflation, which many have assumed just won’t happen, must be treated as a very likely possibility, and that will change the dynamics of opportunities for investment. It leads to lower costs for oil and different pressures for different economies. It will also mean different things for how people use their savings for retirement and how they will seek income in retirement. In short, the next zombie apocalypse can likely be defeated by paying attention and not keeping our fingers in our ears.

How expensive is this Big Mac? More expensive than you might think…

For the enormous wave of Canadians that are on course to retire over the coming few decades, retiring and planning for retirement is getting harder.

Here are the four big reasons why!

1. Inflation

Inflation is the scary monster under the bed when it comes to one’s retirement. People living off of fixed pensions can be crippled by runaway costs of living, and naturally retirees dread the thought that their savings won’t keep pace with the cost of their groceries. But while historic inflation rates have been around 3.2% over the last hundred years, and have been around 2% (and less) over the past few years, inflation has been much higher in all the things that matter. Since the inflation rate is an aggregate number made up of a basket of goods that include big things like computers, fridges and televisions that have been dropping in price over time, those drops offset the rising price of gas, food and home costs. Since you buy food all the time and fridges almost never, the rate of inflation is skewed lower than your pocket book reflects.

You can show this in a simple way by comparing the price of a McDonald’s Big Mac over time. When the Big Mac was first introduced to Canada the price was .45¢, today that price is $5.25. Inflation has fluctuated a great deal since then, but let’s assume the historic rate of 3.2% was an accurate benchmark. If you apply that rate the price of a Big Mac today would be $1.91, in reality the inflation rate on a Big Mac has been much closer to 5.5%.

Canadian Inflation Rate from 2008 – 2014

2. Interest Rates

The business of central bankers has gained greater attention since 2008, but for many making the connection between interest rates, the broader economy and their retirement is tenuous at best. The short story is that weak economies means low interest rates to spur borrowing. Borrowing, or fixed income products, have been the typical go-to engine for creating sustainable income in retirement, and low borrowing costs means low fixed income rates. The drying up of low risk investments that pay livable, regular income streams have left many retirees scratching their heads and wondering how they can keep market volatility at bay while still drawing an income. But as rates have stayed low, and will likely do into the future, bonds, GICs and annuities won’t be enough to cover most living costs, forcing retirees into higher risk sectors of the market.

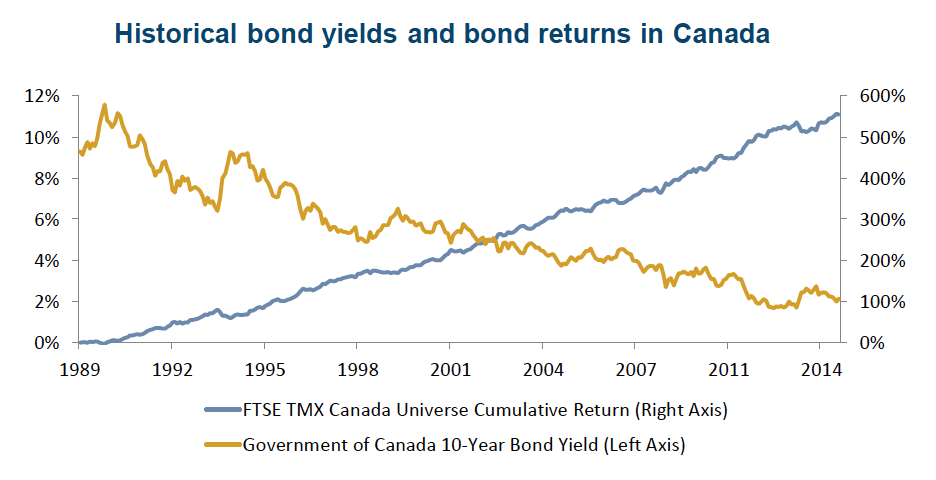

Source: Bloomberg and FTSE TMX Global Debt Capital Markets, monthly data from July 31, 1989 to September 30, 2014, Courtesy of NEI Investments

Don’t get me wrong, I’m not in a rush or anything; but the reality is that you are going to live a long time, and in good health. Where as retirement was once a brief respite before the angel of death swooped in to grab you maybe a year or two later, living into your 90s is going to be increasingly common, putting a beneficial, but very real strain on retirement plans.

In short, retirement is getting harder and harder to plan. You’re living longer, with higher costs and fewer low risk options to generate a steady income.

What Should You Do?

Currently the market itself has been responding to the low interest rate environment. A host of useful products have been launched in the past few years that are addressing things like consistent and predictable income for those currently transitioning into retirement. Some of these products are able to reduce risk, while others explore non-traditional investments to generate income. But before you get hung up on what product you should have you should ensure that your retirement plan is meeting your needs and addressing the future. There is no product that can substitute for a comprehensive retirement and savings plan, so call your financial advisor today if you have questions (and yes, that includes us!)

Want to discuss your retirement? Send us an email and we’ll be in touch right away!

The current market correction is about as fun as a toothache. Made up of a perfect storm of negative sentiment, a slowing global economy and concerns about the end of Quantitative Easing in the US have led to a broad sell-off of global markets, pretty much wiping out most of their gains year-to-date.

This is what my screen looked like yesterday (October 15th, 2014). The little 52L that you see to the left of many stock symbols means that the price had hit a 52 week low. The broad nature of the sell off, and indiscriminate selling of every company, regardless of how sound their fundamentals tells us more about market panic than it does about the companies sold.

One of the focal points of this correction has been the price of oil, which is off nearly 25% from its high in June. Oil is central to the S&P/TSX, making up nearly 30% of the index. Along with commodities, energy prices are dependent on the expectation of future demand and assumed levels of supply. As investor sentiment have come to expect that the global demand will drop off in the coming year the price of oil has taken a tumble in the last few weeks. Combined with the rise of US energy output, also known as the Shale Energy Revolution, or fracking, the world is now awash in cheap (and getting cheaper oil).

The price of Brent Crude oil – From NASDAQ

But as investors look to make sense out of what is going on in the markets they would be forgiven if all they learned from the papers, news and internet sites was a barrage of fear and negativity masquerading as insight and knowledge. The presumed benefit of having so much access to news would be useful and clear insight that could help direct investors on how to best manage the current correction. Instead the media has only thrown fuel on the fire, fanning the flames with panic and fear.

Contrast two similar articles about the winners and losers of a dropping price of oil. The lead article for the October 15th Globe and Mail’s Business section was “Forty Day Freefall”, which went to great lengths to highlight one big issue and then cloak it in doom. The article’s primary focus is the price war that is developing between OPEC nations and North American producers. Even as global demand is reportedly slowing Saudi Arabia is increasing production, with no other OPEC nations seemingly interested in slowing the price drop or unilaterally cutting production. The reason for this action is presumably to stem the growth of oil sand and shale projects, forcing them into an unprofitable position.

This naturally raises concerns for energy production in Canada, but it is not nearly the whole story. The Financial Times had a similar focus on what a changing oil price might mean to nations, and its take is decidedly different. For instance, while oil producing nations may not like the new modest price for oil, cheap oil translates into an enormous boon for the global economy, working out to over $600 billion a year in stimulus. In the United States an average household will spend $2900 on gas. Brent oil priced at $80 turns into a $600 a year tax rebate for households. Cheaper oil is also hugely beneficial to the manufacturing sector, helping redirect money that would have been part of the running costs and turning them into potential economic expansion. It’s useful as well to Emerging Economies, many of which will be find themselves more competitive as costs of production drop on the back of reduced energy prices.

A current map of shale projects, and expected shale opportunities within the United States and Canada.

Business Reporting isn’t about business, it’s about advertising revenues.

While Canada may have to take it on the chin for a while because of our market’s heavy reliance on the energy sector, weakening oil prices also tends to mean a weakening dollar, both of which are welcomed by Canadian manufacturers. Corrections and changing markets may expose weaknesses in economies, but it should also uncover new opportunities. How we report these events does much to help investors either take advantage of market corrections, or become victims of it. As we wrote back in 2013, business reporting isn’t about business, it’s about advertising revenues. Pushing bad news sells papers and grabs attention, but denies investors guidance they need.

A correction is typically defined as a drop of roughly 10% in the markets over a very short period of time. It’s often “welcomed” by investment professionals because it creates opportunities for new investments into liked companies that were previously trading above valuations considered appealing. Corrections are talked about as being necessary, beneficial and part of a normal and healthy market cycle, which all makes it sound somewhat medical. But in medical terms it falls under the category of being told your are about to receive 5 injections in short order and they are all going to hurt.

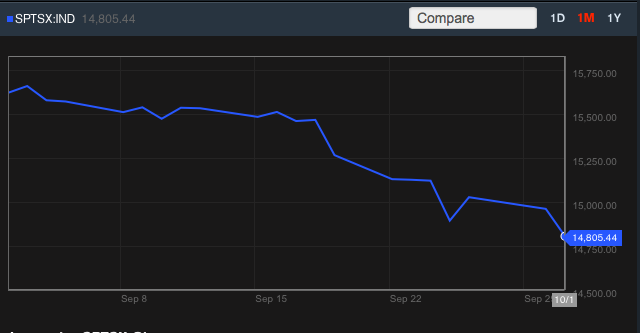

S&P TSX From Bloomberg – October 2, 2014

For investors the past couple of weeks in the market has felt like many such injections. The US markets have had a significant sell off, as have the global, emerging, and Canadian markets. All of it very quickly. The sudden drop has erased many of the gains in an already slow year and eaten dramatically into the TSX’s return which had been one of the best.

Dow Jones Industrial From Bloomberg – October 2, 2014

For many investors any sudden change in the direction of the markets can immediately give the sense that we are heading into another 2008. As Canadian (and American) investors are now 6 years older and closer to retirement the stakes also seem much higher. So here are some reasons why you shouldn’t be concerned about the most recent market volatility, and what you can do to make them work to your advantage.

1. Everyone is nervous.

For several months people have been calling for a correction. Investor sentiment is neutral and consumer confidence has dipped, meaning that overall atmosphere is somewhat negative for the markets. But that can be a good thing. Market crashes and bust cycles typically show up when people are exuberant and feel euphoric about markets. Bad news is swept aside and the four most dangerous words in investing “This time it’s different” become the hallmark of the new bubble. It’s rare that negativity breeds an over exuberant market.

3. Corporations are really healthy, and so are investors.

Canadians may still have bundles of debt, but the US is a different story. American corporations and households have been heavily deleveraging since 2008. In fact corporations in the US look to be some of the healthiest in decades, showing better earnings to debt ratios than previously thought. Crashes have as much to do with over-production as they do with out-of-control borrowing. The two go hand in hand and both factors are currently missing from the existing economic landscape.

4. Energy is cheap. Like, really cheap.

Remember when oil was more than $100 a barrel? High energy prices, and the expectation of future high energy prices can really put the kibosh on future returns and throw cold water all over the market. As we’ve previously said, energy is the lifeblood of civilizations and a steady supply of affordable energy is what separates great economies from poor ones. (Look, we tweeted this earlier! See, twitter is useful. Follow us @Walker_Report)

West Texas Crude Oil Price over the last 3 months – from NASDAQ – October 2, 2014

The arrival and growth of American gas production combined with changing technologies and increasing efficiencies on existing energy use means that global demand is slowing, while global supply is increasing. In fact in March of last year, the head analyst for energy at Citigroup published a paper describing exactly this trend of improved efficiency with new sources as a mix for lower energy prices in the long term. Whether this proves true over the next two decades is hard to say, but what is true is that cheap energy helps economies while expensive energy hinders it. Since economies have already adjusted to the higher price over the last few years, a declining price is a tailwind for growth.

Does this mean that there aren’t any risks in the market? Absolutely not. Europe is having a terrible year as a result of persistent economic problems and Russian intransience, and many Emerging Markets are showing the strain of continued growth, either through corruption or exceeding optimism about the future. Those pose real risks, but taken in the grand scheme of things our outlook remains positive for the markets.

How can I make this all work for me?

So what can you do as an investor to make a correction benefit you? The first piece of advice is always the same. Sit tight. Dramatic changes to your investments when they are down tends to lead to permanent losses. Secondly, rebalance your account periodically as the market declines. On the whole equity funds will lose a greater proportion of their value than fixed income, leaving a balanced portfolio heavier in conservative than growth investments. Rebalancing gives you a chance to buy more units of growth funds at a lower price while adding greater potential for upside as the market recovers. Lastly, if you have money sitting on the sidelines, down markets are great opportunities to begin Dollar-Cost-Averaging. For nervous investors this is a great way to ease into the markets even as markets look unstable. You can read about it here, but I recommend watching the movie below for a nice visual explanation. Now, take your medicine.

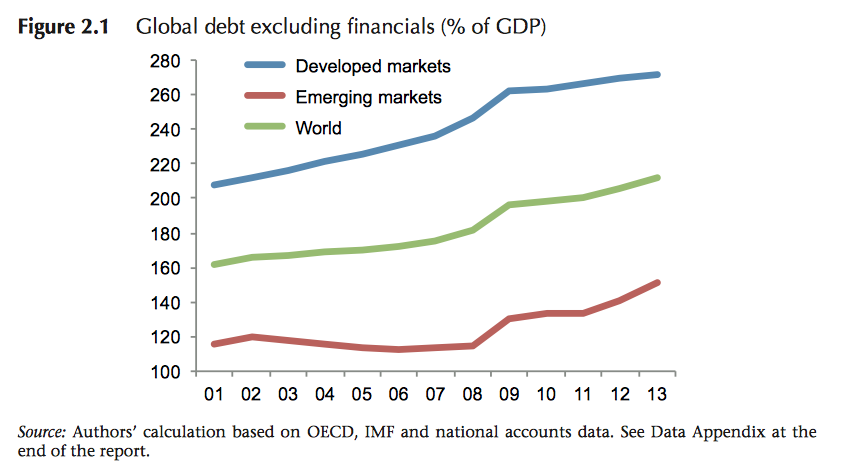

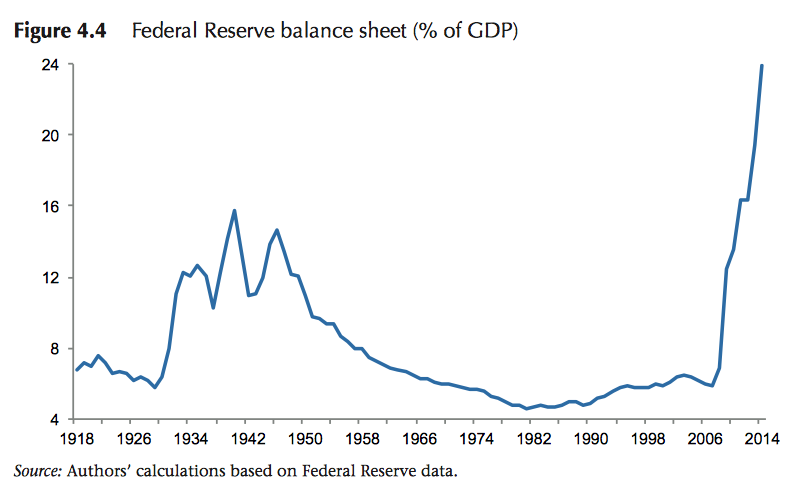

Yesterday the 16th Geneva Report was released bearing bad news for everybody that was hoping for good news. The report, which highlighted that debt across the planet had continued to increase and speed up despite the market crash of 2008, is sobering and seemed to cast in stone that which we already knew; that the global recovery is slow going and still looks very anemic.

The report is detailed and well over a hundred pages and only came out yesterday, so don’t be surprised if all the news reports you read about it really only cover the first two chapters and the executive summary. What is interesting about the report is how little of it we didn’t know. Much of what the report covers (and in great detail at that) is that the Eurozone is still weak, that the Federal Reserve has lots of debt on its balance sheets, but that it has helped turn the US

A look at the Fed’s Balance Sheet from the Geneva Report

economy around, that governments have been borrowing more while companies and individuals borrow less, and that economic growth in the Emerging Markets has been accompanied by considerable borrowing. All of this we knew.

What stands out to me in this report are two things that I believe should matter to Canadian investors. First is the trouble with low interest rates. Governments are being forced to keep interest rates low, and they are doing that because raising rates usually means less economic growth. But as growth rates have been weak, nobody wants to raise rates. This leads to a Catch-22 where governments are having to take direct measures to curb borrowing because rates are low, because they can’t raise rates to curb borrowing.

The second is the idea of “Economic Miracles” which tend to be wildly overblown and inevitably lead to the same economic mess of overly enthusiastic investors dumping increasingly dangerous amounts of money into economies that don’t deserve it just to watch the whole thing come crashing down. Economic miracles include everything from Tulip Bulbs and South Sea Bubbles to the “Spanish Miracle” and “Asian Tigers”, all of which ended badly.

All of this should not dissuade investors from the markets, but it should be seen as a reminder about the benefits of diversification and it’s importance in a portfolio. It is often tempting to let bad news ruin an investment plan, but as is so often the case emotional investing is bad investing.

I’ve added an investment piece from CI Investments which has been floating around for years. It pairs the level of the Dow Jones Industrial Average with whatever bad news was dominating the market that year. It’s a good way to look at how doom and gloom rarely had much to do with how the market ultimately performed. Have a look by kicking the link! I don’t want to Invest Flyer

***I’ve just seen that the Globe and Mail has reported on the Geneva Report with the tweet “Are we on the verge of another financial crisis” which is not really what the report outlines.

In the hunt for returns in the jungle of investing we rarely talk about “quality of life”, but it should be remembered that the whole reason for investing is precisely that; to preserve and improve one’s quality of life, either through retirement savings, covering and planning for education or making purchasing a house feasible. That’s what this is all for.

So it’s easy then to get lost in the mechanics of investing. At the charts (see #MarketGlance) the news and the conferences:

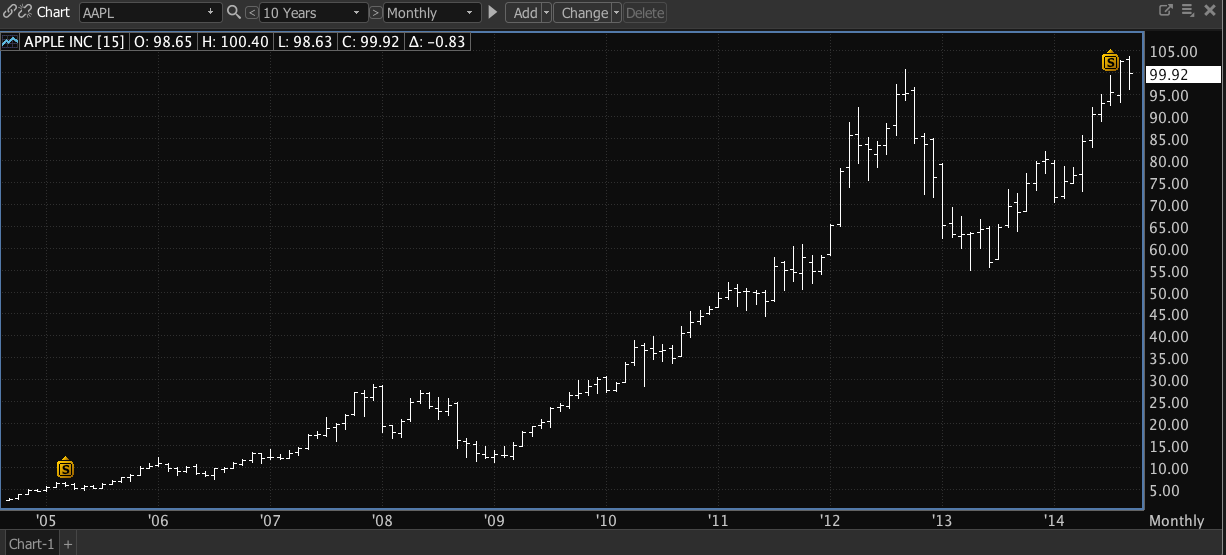

This tends to create a disconnect between how we experience the world and how we want our investments to work. For instance I am a big believer in Apple products. (AAPL). I like their phones and computers, I’m in their ecosystem, and as an investor I am impressed at their success as a company. But as a user of an iPhone I’ve started to wonder just how much time I waste under the pretence of having a highly capable phone.

Apple Stock over the last ten years

When the iPhone first came to Canada I was struck by the idea that I could look up directions easily, check the internet quickly for information and have access to my emails. When first introduced the iPhone was a tool of productivity. Since then the smart phone market has been flooded and “feature creep” is definitely a term I would use to describe what many of these phones can now do. Meanwhile productivity has taken a backseat to a host of other competing and primarily entertaining functions. In short, I was tired of wasting time on my phone doing nothing.

And along came Blackberry offering, in some ways, a phone that promises to do less fun stuff, and do more work stuff. And while I had shunned Blackberry for years, based largely on my own terrible experience with the older models and their tiny screens, the new Passport seemed to offer me not simply a useful phone for doing work, but also terrible one to watch Netflix on. Because why am I watching Netflix on my phone in the first place?

Are angry birds really the best use of your time on a $1000 phone?

We live in an age of giant flat TVs with instant movie watching capabilities, but for reasons beyond me I’ve taken to watching stuff on my phone. So while I love Apple, and believe that they have a great company, I’m hoping that I can improve my quality of life by degrading my phone experience somewhat.

Maybe there is hope for Blackberry yet.

Recommended Read: The End of Absence: What We’ve Lost in a World of Connection by Michael Harris

Last Friday I watched the TSX start to take a precipitous fall. The one stock market that seemed immune to any bad news and had easily outperformed almost every other index this year had suddenly shed 200 points in a day.

Big sell-offs are common in investing. They happen periodically and can be triggered by anything, or nothing. A large company can release some disappointing news and it makes investors nervous about similar companies that they hold, and suddenly we have a cascade effect as “tourist” investors begin fleeing their investments in droves.

This past week has seen a broad sell-off across all sectors of the market in Canada, with Financials (Read: Banks), Materials (Read: Mining) and Energy (Read: Oil) all down several percentage points. In the course of 5 days the TSX lost 5% of its YTD growth. That’s considerable movement, but if you were looking to find out why the TSX had dropped so much so quickly you would be hard pressed to find any useful information. What had changed about the Canadian banks that RBC (RY) was down 2% in September? Or that TD Bank (TD) was down nearly 5% in a month? Oil and gas were similarly effected, many energy stocks and pipeline providers found themselves looking at steep drops over the last month. Enbridge (ENB) saw significant losses in their stock value, as did other energy companies, big and small, like Crew Energy (CR).

The S&P TSX over the last five days

All this begs the question, what changed? The answer is nothing. Markets can be distorted by momentum investors looking to pile on to the next hot stock or industry, and we can quibble about whether or not we think the TSX is over valued by some measure. But if you were looking for some specific reason that would suggest that there was something fundamentally flawed about these companies you aren’t going to have any luck finding it. Sometimes markets are down because investors are nervous, and that’s all there is to it.

Market panic can be good for investors if you stick to a strong investment discipline, namely keeping your wits about you. Down markets means buying opportunities and only temporary losses. It help separates the real investors from the tourists, and can be a useful reminder about market risk.

So was last Friday the start of a big correction for Canada? My gut says no. The global recovery, while slow and subject to international turmoil, is real. Markets are going to continue to recover, and we’ve yet to see a big expansion in the economy as companies deploy the enormous cash reserves they have been hoarding since 2009. In addition, the general trend in financial news in the United States is still very positive, and much of that news has yet to be reflected in the market. There have even been tentative signs of easing tensions between Russia and the Ukraine, which bodes well for Europe. In fact, as I write this the TSX is up just over 100 points, and while that may not mean a return to its previous highs for the year I wouldn’t be surprised if we see substantial recoveries from the high quality companies whose growth is dependent on global markets.

To many Canadians the CPP is something that you simply receive when you turn 65, (or 70, or 60, depending on when you want or need it) with little consideration for how the program works or is run. That’s too bad because the CPP is successful, enlightening and puts its American counterpart, Social Security, to shame.

To many Canadians the CPP is something that you simply receive when you turn 65, (or 70, or 60, depending on when you want or need it) with little consideration for how the program works or is run. That’s too bad because the CPP is successful, enlightening and puts its American counterpart, Social Security, to shame.