***This post will refer to both a mutual fund company and a particular fund. This post should not be construed as endorsing that fund. We always make sure that we cite our sources and in this instance our source is a fund company, and we are not suggesting in any way that you should invest in or purchase this fund. If you are interested in any fund, please consult with your financial advisor first for suitability, especially if that financial advisor is us!***

Since the price of oil dropped there have been lots of reasons to be excited. First the price of gas at the pumps is so low that I don’t hate going there anymore. Second, investments in energy have suffered since oil lost close to $30 in value.

Since the price of oil dropped there have been lots of reasons to be excited. First the price of gas at the pumps is so low that I don’t hate going there anymore. Second, investments in energy have suffered since oil lost close to $30 in value.

And while energy stocks have recovered somewhat from their low points, they are still way off where they were earlier in the year. I’m not going to get into the finer points about the nuances of energy producers and the various types of oil and costs of production. It’s a worthwhile article, but will take up too much time here. Instead I wanted to focus on a different way that Canadians can participate in the energy sector.

Commodities can be volatile but also a valuable element of a portfolio. So how can Canadians play the energy sector while being mindful of the risks associated with it?

The answer may be by investing in what is called “Midstream MLPs”. Midstream MLPs (Master Limited Partnerships) are American operators that transport energy from the producers to the consumers. It’s a capital intensive business that is federally regulated but traded on the stock market. It therefore provides consistent cash flow while offering liquidity to investors. But Canadians already have opportunities for energy infrastructure, so why should they care about this in the United States? The answer has everything to do with the rising levels of oil production in the United States combined with what federal regulators are willing to do to encourage new growth.

The answer has everything to do with the rising levels of oil production in the United States combined with what federal regulators are willing to do to encourage new growth.

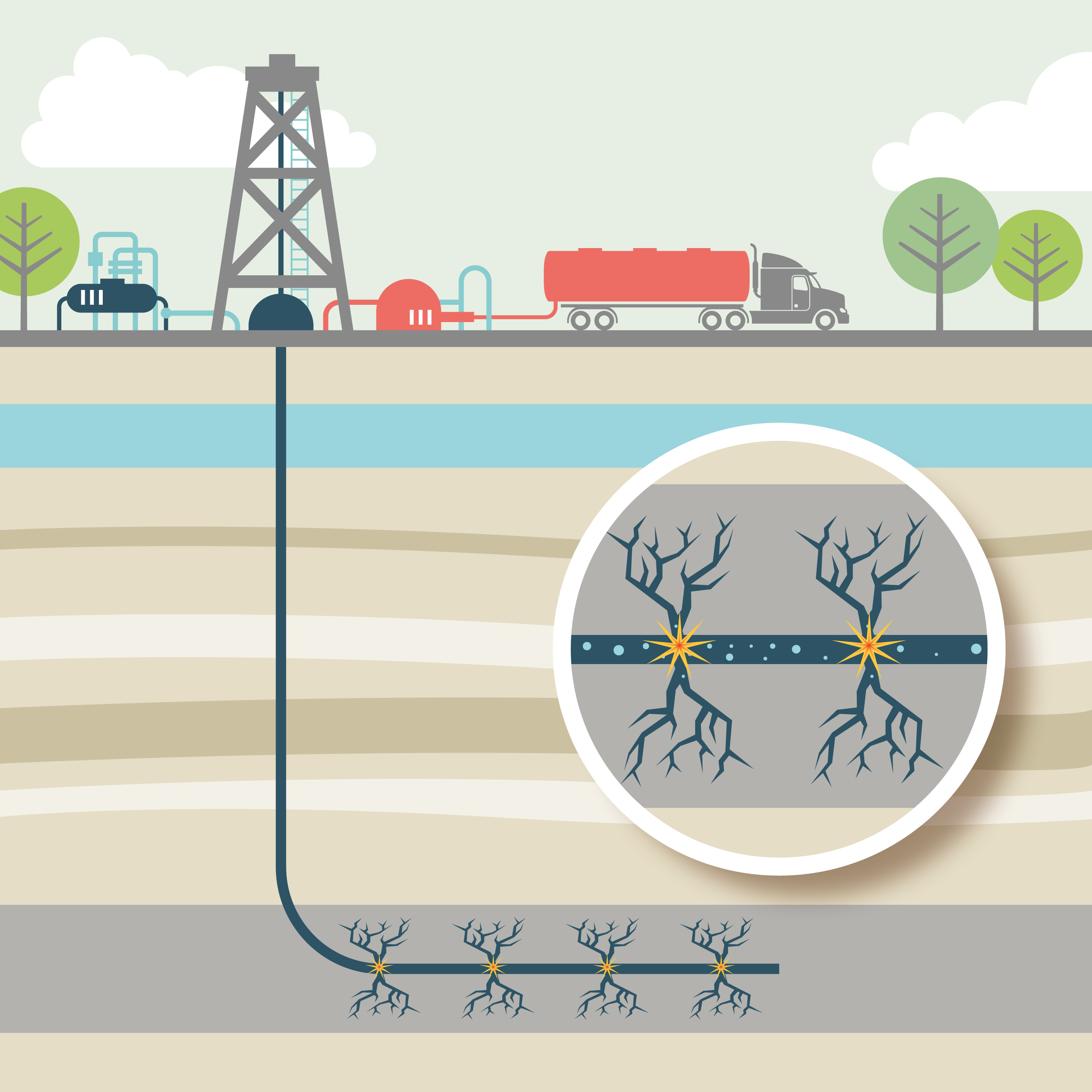

That brings us to the growth of the shale revolution in the United States. Newly discovered reserves (of significant size), improved technology and a dropping costs of production have set the US on a course to be the largest global energy provider in the coming years. This combination of efficiencies means that the United States is going to continue to increase its oil production over the next decade, while dropping the cost of extraction for each additional barrel. But each barrel produced has to go somewhere.

In the United States, Midstream MLPs are responsible for moving that oil. But it’s a sector that also must grow. Infrastructure to move oil efficiently from shale producers doesn’t exist yet, and regulators are eager to get MPLs in place with new development. New infrastructure is costly, and while the business model for an MLP doesn’t require a high price for energy to be profitable, it does need assurances about the consistency of the volume of oil to be moved. To encourage that growth regulators are allowing the price that MLPs charge to rise at a rate faster than inflation. Why are they doing that? Much of the shale oil is having to be shipped via rail to get to its right home. This causes price disparities that reduces producer margins and rankles federal governments.

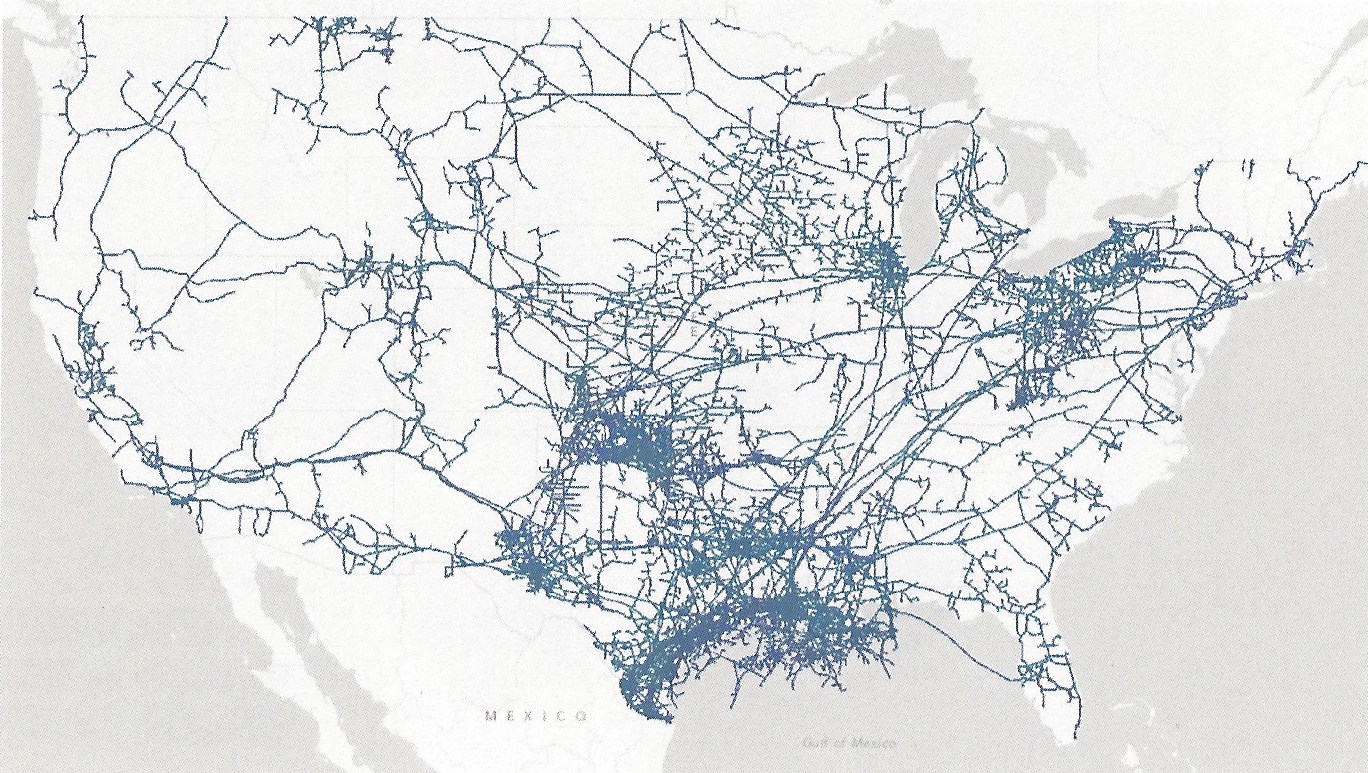

Pipelines in the US. Most of the pipelines direct energy to Texas, which isn’t set up to handle the ultra light crude from shale projects. that energy, coming out of North Dakota, needs to get to New Jersey. The lack of pipelines means it is being shipped by rail to Chicago and then via pipeline.

Currently there is only one fund option in Canada that we are aware of for investing in MLPs. We had an opportunity earlier this week to meet the managers of this fund and were greatly impressed by what they had to show us. I am already a big believer in the growing Shale Revolution, and am particularly pleased by the arrival of new opportunities for investment. Growth in the Canadian and American energy sectors is good news for not just investors, but also citizens. Russia, Saudi Arabia, Venezuela and a host of other despotic and semi-despotic regimes have been able to get by on the high price of oil. Now they are feeling the pinch of a decreasing price that has the benefit of bringing jobs back to North America while weakening their influence. In all, this is a good story for everyone.

Want to talk oil? Send us a message!