Possibly the most significant news in the last 24 hours was that Barack Obama had used his veto for the first time in five years to end the Keystone XL Pipeline. The pipeline, delayed by 6 years carried with it the hopes of the Canada’s Conservative party and oil executives in Alberta. The pipeline had been opposed, studied and debated, being bounced back and forth through the US government. It had been primarily opposed by environmentalists who object to the environmental impact of Alberta Tar Sand oil and hoped that by killing the pipeline less of it would be extracted, alternative fuels would fill some of the gaps and the world would be a healthier place as a result. It’s subsequent (and rather final) cancelation is being heralded as a victory by many environmental activists.

Possibly the most significant news in the last 24 hours was that Barack Obama had used his veto for the first time in five years to end the Keystone XL Pipeline. The pipeline, delayed by 6 years carried with it the hopes of the Canada’s Conservative party and oil executives in Alberta. The pipeline had been opposed, studied and debated, being bounced back and forth through the US government. It had been primarily opposed by environmentalists who object to the environmental impact of Alberta Tar Sand oil and hoped that by killing the pipeline less of it would be extracted, alternative fuels would fill some of the gaps and the world would be a healthier place as a result. It’s subsequent (and rather final) cancelation is being heralded as a victory by many environmental activists.

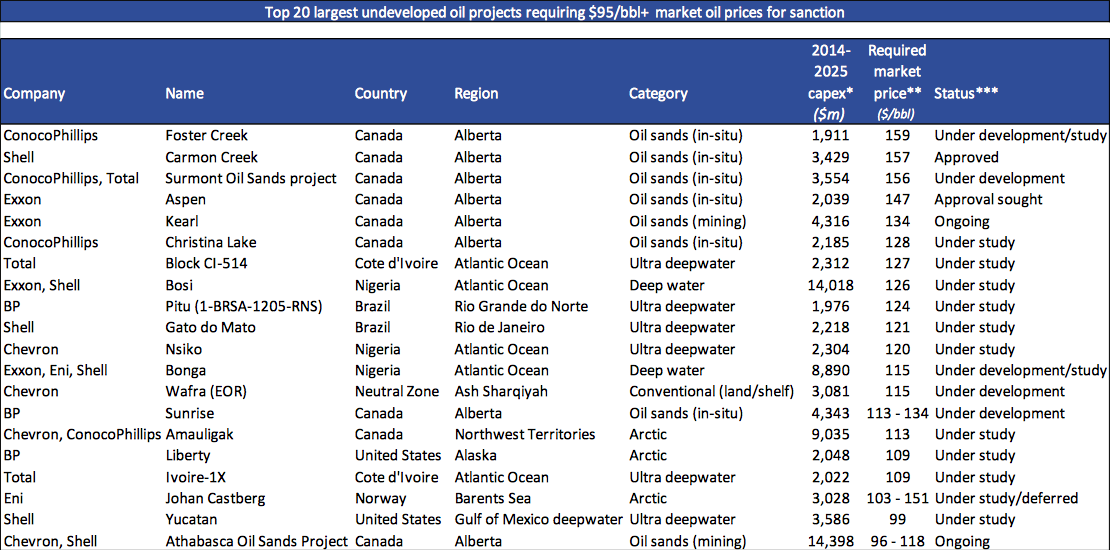

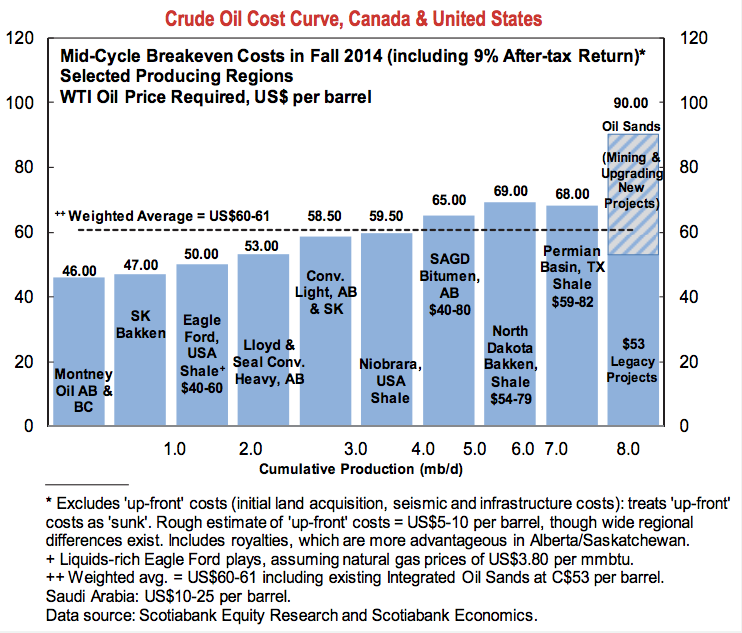

As we’ve already written, this was not case. While the pipeline hadn’t been built it hadn’t slowed the development of the oil sands, or impeded its movement to refineries. Instead it had simply been supplanted by rail cars. Although more expensive, the roughly $9 a barrel premium was well worth it when oil was above $100 a barrel.

The current price of oil helps explain why there was little real political risk to anybody in the veto of the pipeline. While oil was expensive there was real incentive to get Canadian oil to US markets. It helps offset oil from more troubling parts of the world and makes the economy run a little smoother. But the rise of US shale, the falling price of oil, the use of train cars, an improving economy and rising dollar has wrecked the economics of building the pipeline. By the time the Obama had vetoed the bill there was very little at stake politically except to satisfy his environmental base of voters. The pipeline may yet be still resurrected, but six years on and a new economic reality will likely mean little will get done soon.

The death of the pipeline is troubling most of all for Canada. Shipping oil by train is more expensive, and considerably more dangerous. It also reflects the new found reality that the government cannot rely on oil prices to bolster the economy. But most of all it reflects the continuing declining fortunes of Alberta and returns focus to Ontario, the once and future king of the broad economy.