Since late February the bulk of global attention has been focused on the Russian invasion of Ukraine. The invasion remains ongoing, and will likely last for months, potentially even years, and represents the most dangerous geopolitical situation we are likely to face until China tries to enforce control over the South China Seas or invades Taiwan.

But while our attention has been narrowly focused, interest is growing about how the world’s second largest economy is choosing to mange the late stages of the pandemic, a series of choices that have ramifications for much of the world.

China has had mixed luck with Covid. By the end of 2020 it looked as though China might be the only winner economically from the pandemic, but 2021 turned out to be a year for the West. First, Western vaccines, particularly the mRNA vaccines were highly effective, while the Chinese vaccine produced domestically had only a 50% success rate. The Chinese government also was hyper critical of the more effective Moderna and Pfizer vaccines, essentially precluding them from Chinese use. This has left the country in a difficult spot. Chinese mandated lockdowns have been brutal but effective, leading to uneven vaccine use. The low infection rates that the “Covid Zero” policy has delivered has also robbed the country of natural immunity. Today China, already struggling economically, is still locking down whole cities in the hopes of containing outbreaks.

Shanghai is the current major city to be shut down, but the lockdowns are spreading. Complaints about food shortages and people trapped in apartment buildings, offices, and closed off from their places of work have led to some fairly strange places, including protests and at least once the use of “speaking drones” urging citizens to comply with rules and reprimanding the citizens singing in protest one night to “Control your soul’s thirst for freedom. Do not open your windows and sing.”

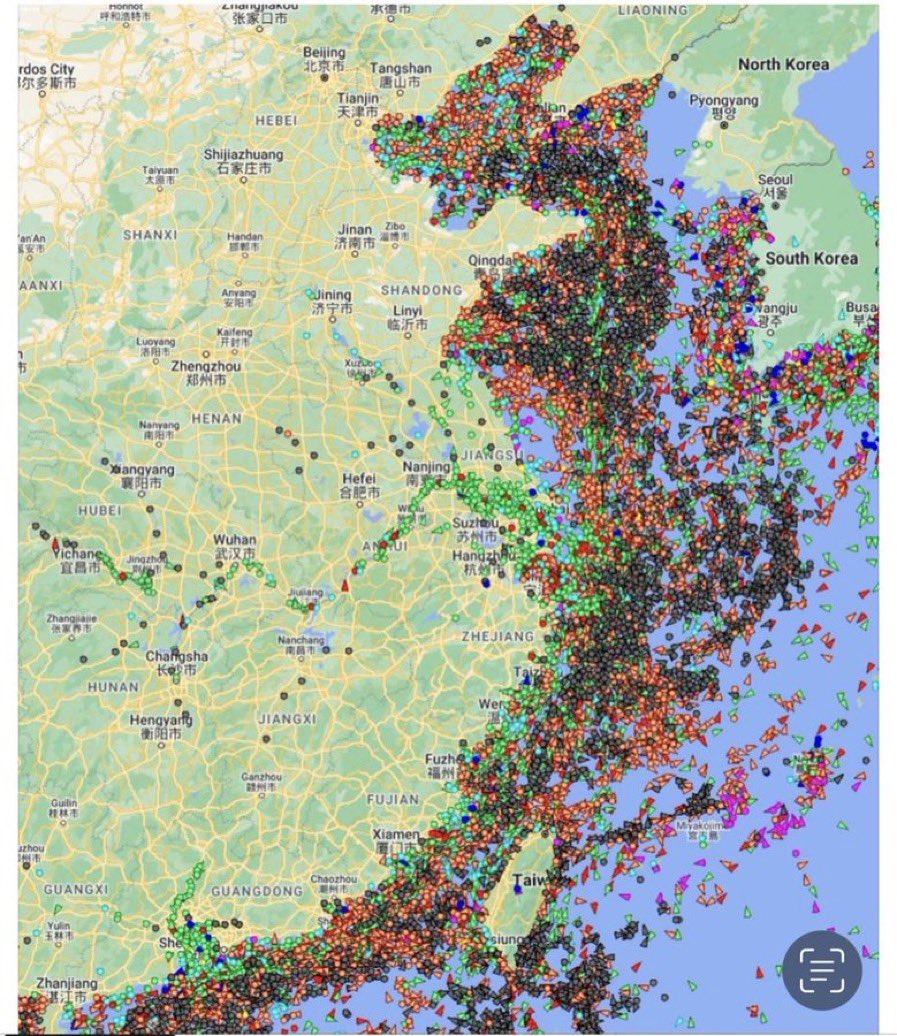

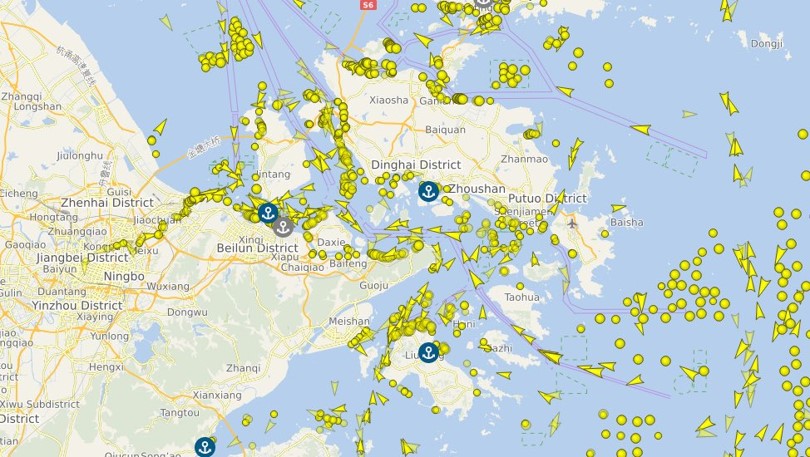

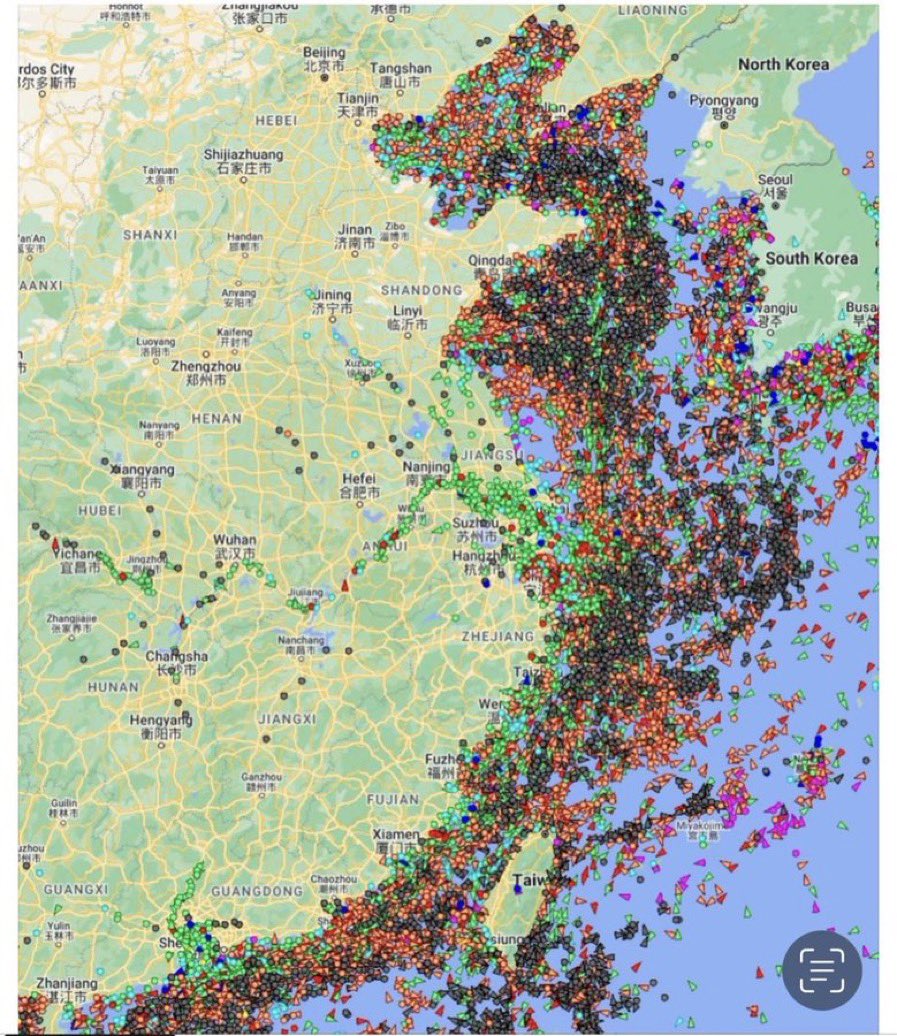

Chinese lockdowns are also worsening global inflation. The supply chain disruptions caused by the most recent lockdowns in Shanghai are dramatic to say the least. In the above picture each yellow dot represents one cargo ship waiting to be docked and unloaded. Supply chains were already deeply stressed when Shanghai went into lockdown last month, and the global impact of further supply disruptions is something we’re very likely to notice.

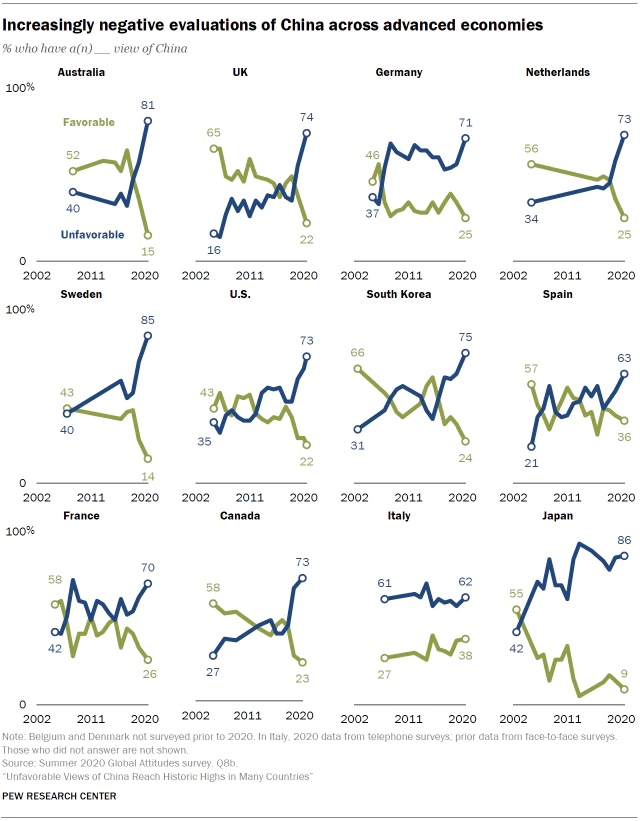

Lastly, some months ago (October 2020) I had detailed how China’s foreign policy, which was heavy handed and often petulant, was angering nations all across the globe. China may not view the world the way its geopolitical rivals do, but its inability to grasp at least what might be considered fair or just by other nations is damaging its own ability to wield soft power, an essential part of being a global hegemon. China’s decision to back Russia in its invasion of Ukraine likely reflected China’s near-term goals of retaking Taiwan and its general contempt for the current world order. However, the global resistance to the Russian invasion, the support shown Ukraine and the barrage of negative publicity (as well as realizing that an untested military in countries with lots of corruption may not be able to score quick military victories) must serve as a wake-up call to China’s ruling class. As of 2022 China seems to have squandered much of its international good will and is unlikely to find many willing allies for its global ambitions.

China seems to be suffering on all fronts. 2021 was a bad year for China’s economy, cumulating in the public meltdown of one of its biggest developers in November. But everything, from its politics to its public health policies are working against it. The world’s second largest economy, one that is the largest trading partner to 130 countries, can’t seem get out of its own way, and as it falters it can’t help but impact us.

Walker Wealth Management is a trade name of Aligned Capital Partners Inc. (ACPI)*

ACPI is regulated by the Investment Industry Regulatory Organization of Canada (www.iiroc.ca) and a Member of the Canadian Investor Protection Fund (www.cipf.ca). (Advisor Name) is registered to advise in (securities and/or mutual funds) to clients residing in (List Provinces).

This publication is for informational purposes only and shall not be construed to constitute any form of investment advice. The views expressed are those of the author and may not necessarily be those of ACPI. Opinions expressed are as of the date of this publication and are subject to change without notice and information has been compiled from sources believed to be reliable. This publication has been prepared for general circulation and without regard to the individual financial circumstances and objectives of persons who receive it. You should not act or rely on the information without seeking the advice of the appropriate professional.

Investment products are provided by ACPI and include, but are not limited to, mutual funds, stocks, and bonds. Non-securities related business includes, without limitation, fee-based financial planning services; estate and tax planning; tax return preparation services; advising in or selling any type of insurance product; any type of mortgage service. Accordingly, ACPI is not providing and does not supervise any of the above noted activities and you should not rely on ACPI for any review of any non-securities services provided by Adrian Walker.

Any investment products and services referred to herein are only available to investors in certain jurisdictions where they may be legally offered and to certain investors who are qualified according to the laws of the applicable jurisdiction. The information contained does not constitute an offer or solicitation to buy or sell any product or service. 16 Past performance is not indicative of future performance, future returns are not guaranteed, and a loss of principal may occur. Content may not be reproduced or copied by any means without the prior consent of the author and ACPI.