As summer has worn on there have been a growing number of headlines focused on Toronto’s stagnant condo market. In short, the number of units for sale continues to grow as buyers refuse to pay the elevated prices being demanded by sellers. Interestingly sale activity has been stagnant and prices haven’t really moved despite the growing inventory.

The knock on effect has been a significant slow down in new developments. This has led to growing concern that prices will rise in the future as new supply is postponed or canceled, and pressure is growing to get interest rates lowered to help stimulate buyers.

All of this sounds a touch too convenient for me. One of the reasons (not the only reason, but a significant one) we face a “cost of living crisis” is that housing has increasingly been seen as an investment, one that people have had greater faith in than other traditional assets. But housing booms aren’t new, and it seems odd to me that our chief concern about a growing glut of over-priced condos will be that condo prices will be higher in five to ten years. A more pressing concern is likely that condo investors, and the banks that have provided the mortgages, are deeply concerned that if buying doesn’t resume property prices could take a serious decline, erasing Canadian wealth and forcing Canadian banks to write down balance sheets.

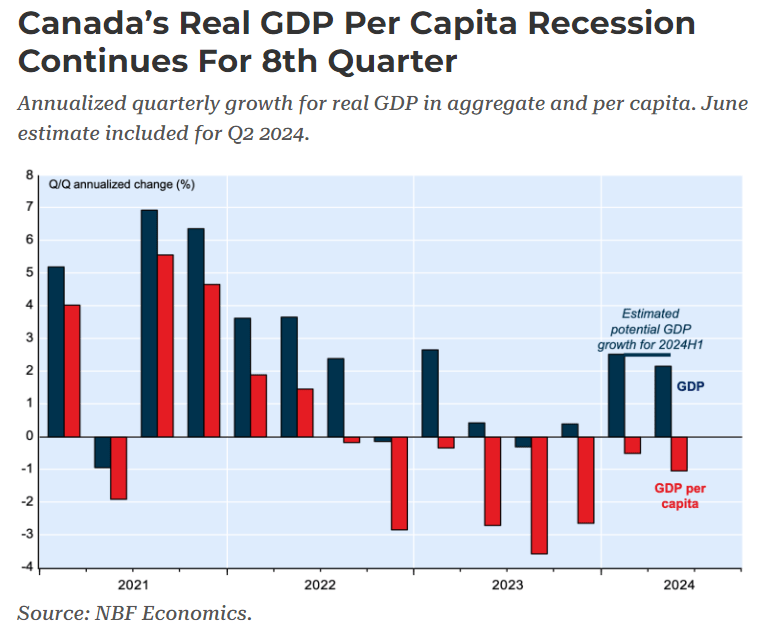

2024 has been a disappointing year for Canadian economic news. Aside from the headlines above, one of the most striking statistics is that Canada is losing economic ground per capita. Much of our GDP growth is coming from high immigration, in effect importing new economic activity but at a rate below what is needed to expand the economy on a per person basis, and it has been doing so for more than 2 years. We are, in effect, in a “per capita recession”.

Since 2022, interest rate increases have pummeled the economy, particularly real estate, which has grabbed a lot of headlines. But Canada’s real estate market has shown considerable resilience through the first few years. However, investors that over are extended and feel the building pain from higher borrowing costs are starting to exit their investments. That hasn’t been altered by the recent interest rate cut which has yet to stimulate much new buying activity. Pressure is building from sectors of the economy to see rates fall and hopefully ease or reverse the effects of higher borrowing costs, but it remains to be seen whether rate cuts can happen at a pace both responsibly and fast enough to substantially change the direction of Canada’s economy (if it can at all).

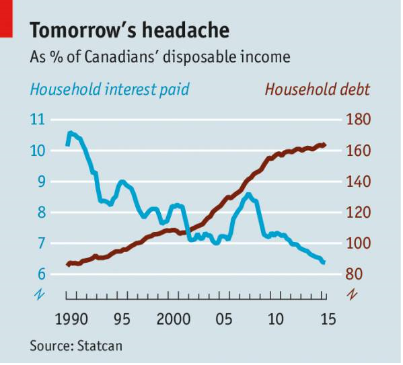

On Monday, August 5th, changes in interest rates from the Bank of Japan reportedly triggered an unwinding of a popular “carry trade”, in which large institutions borrowed money in Japan for low cost, and then invested that money in US stocks. A hike in the BoJ’s lending rate had forced up the value of the yen, forcing the sale of those same US investments to pay back the now more expensive Japanese loans. Markets have recovered quickly, but it shook investor confidence, and while the explanation may not be wholly accurate, it’s a useful reminder that debt, which offers real value when used in moderation, can make economies extremely fragile. For years Canada has had the highest level of household debt to disposable income of any G7 country, and much of that was tied up in housing. What happens next is anybody’s guess.

Aligned Capital Partners Inc. (“ACPI”) is a full-service investment dealer and a member of the Canadian Investor Protection Fund (“CIPF”) and the Canadian Investment Regulatory Organization (“CIRO”). Investment services are provided through Walker Welath Management, an approved trade name of ACPI. Only investment-related products and services are offered through ACPI/Walker Wealth Management and covered by the CIPF. Financial planning services are provided through Walker Wealth Management. Walker Wealth Management is an independent company seperate and distinct from ACPI/Walker Wealth Management.

In his book Fooled by Randomness, Nassim Taleb says of hindsight bias “A mistake is not something to be determined after the fact, but in the light of the information until that point.” With this guidance we can forgive some of the covid precautions and restrictions governments imposed on populations in 2020, a period of great uncertainty.

But in mid-2022 assessing the course of action by governments and central banks as they attempt to tackle a number of non-pandemic related crises (as well as still managing a pandemic that is increasingly endemic) I think its fair to say that mistakes are being made. From political unrest, to cost of living nightmares and finally inflation dangers, the path being plotted for us should be inviting closer scrutiny by citizens before we find ourselves with ever worsening problems.

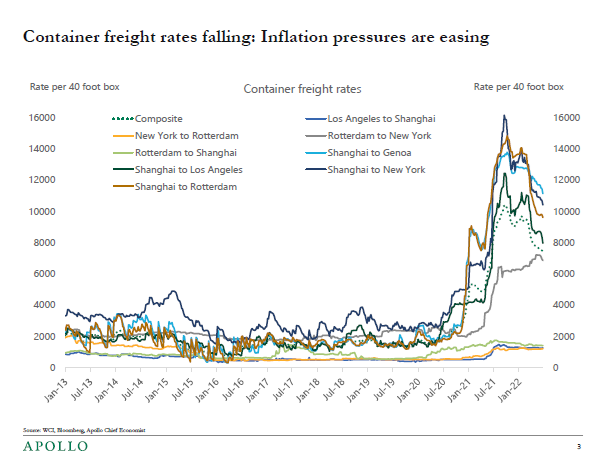

Let’s start with the twin risks of inflation and interest rates. Inflation is high, higher than its been in decades, and central banks the world over are attempting to stamp this out with aggressive rate hiking. It is easy to point to Turkey, a country whose inflation rate is 70%, and see that their recent cutting of interest rates is a mistake in the face of such crippling inflation. But what are we to make of North American efforts to slow inflation, even at the risk of a recession? Inflation for much of the West has been tied to economic stimulus (in the form of government action through the pandemic), supply chain disruptions and low oil and gas inventories. The economy is running “hot”, with lots of businesses struggling to find employees. But inflation, measured as the CPI is a rear-view mirror way of understanding the economy, also known as a lagging indicator. But here is one that is not. The price of container freight rates, which have fallen substantially from the 2021 highs.

We can count other numbers here too. The stock market, which is having a bad year, has fallen close to pre-pandemic highs. A $10,000 investment in the TSX Composite Index would have a return of 6.1% over the past 28 months, or an annualized rate of 2.6%. In February of this year that annualized rate was 8.85%, a 70% decline in returns. The numbers are worse for US markets. While US markets have performed better through the pandemic, the decline in the S&P500 is roughly 75% from its pandemic high in annualized returns (these numbers were calculated at the end of June, offering a recent low point in performance).

For many who felt that the stock market was too difficult to navigate but the crypto market offered just the right mix of “can’t fail” and “new thing”, 2022 has wiped out $2 trillion (yes, with a “T”) of value.

In fact speculative bubbles are themselves inflationary and their elimination will also help reduce inflation. Writes Charles Mackay in his famous book Extraordinary Popular Delusions and the Madness of Crowds (1841) on the Mississippi Bubble in France, “[John] Law was now at the zenith of his prosperity, and the people were rapidly approaching the zenith of their infatuation. The highest and lowest classes were alike filled with a vision of boundless wealth…”

“It was remarkable at this time, that Paris had never before been so full of objects of elegance and luxury. Statues, pictures, and tapestries were imported in great quantities from foreign countries, and found a ready market. All those pretty trifles in the way of furniture and ornament which the French excel in manufacturing were no longer the exclusive play-things of the aristocracy, but were to be found in abundance in the houses of traders and the middle classes in general.”

Evidence today indicates that supply chains are beginning to correct, an important component of taming inflation, while trillions of dollars have been wiped out of a speculative bubble. Even oil, which seems to be facing structural issues that would normally be inflationary has had a significant retreat, along with other commodities like copper, lumber and wheat. Some of these declines may only be temporary as markets react to recession threats, but these declines do not happen in a vacuum. They are disinflationary and should be treated as such.

But central banks seem ready to trigger a recession in the name of defeating the beast of inflation even as it seems to be bleeding out on the ground. In June the Federal Reserve raised its benchmark interest rate by 0.75%, and the current view is that the Bank of Canada is likely to do the same in July. All this is sparking deep recession fears that seem to be driving markets lower.

Average rents in the GTA in June were up 18% over last year

That’s an increase of over $400 per month in just one year

Rather than actually making renting affordable, @cafreeland thinks it’s a better idea to drive up rents and then just send renters a one time cheque for $500 pic.twitter.com/dgq1FAAJZi

In the background remain genuine issues that seem to be addressed at best haphazardly. Inflation is a real issue making food prices go up, but its been crushing people in housing for years. Even as interest rise and house prices moderate lower, average rents in the GTA were up 18% over the last year. The Canadian government’s response to the mounting costs of living has been to propose a one time payment of $500 to low income renters. That is just a little more than the average increase in rent over the previous 12 months.

In the face of such mounting housing pressure the city of Toronto has done the following things:

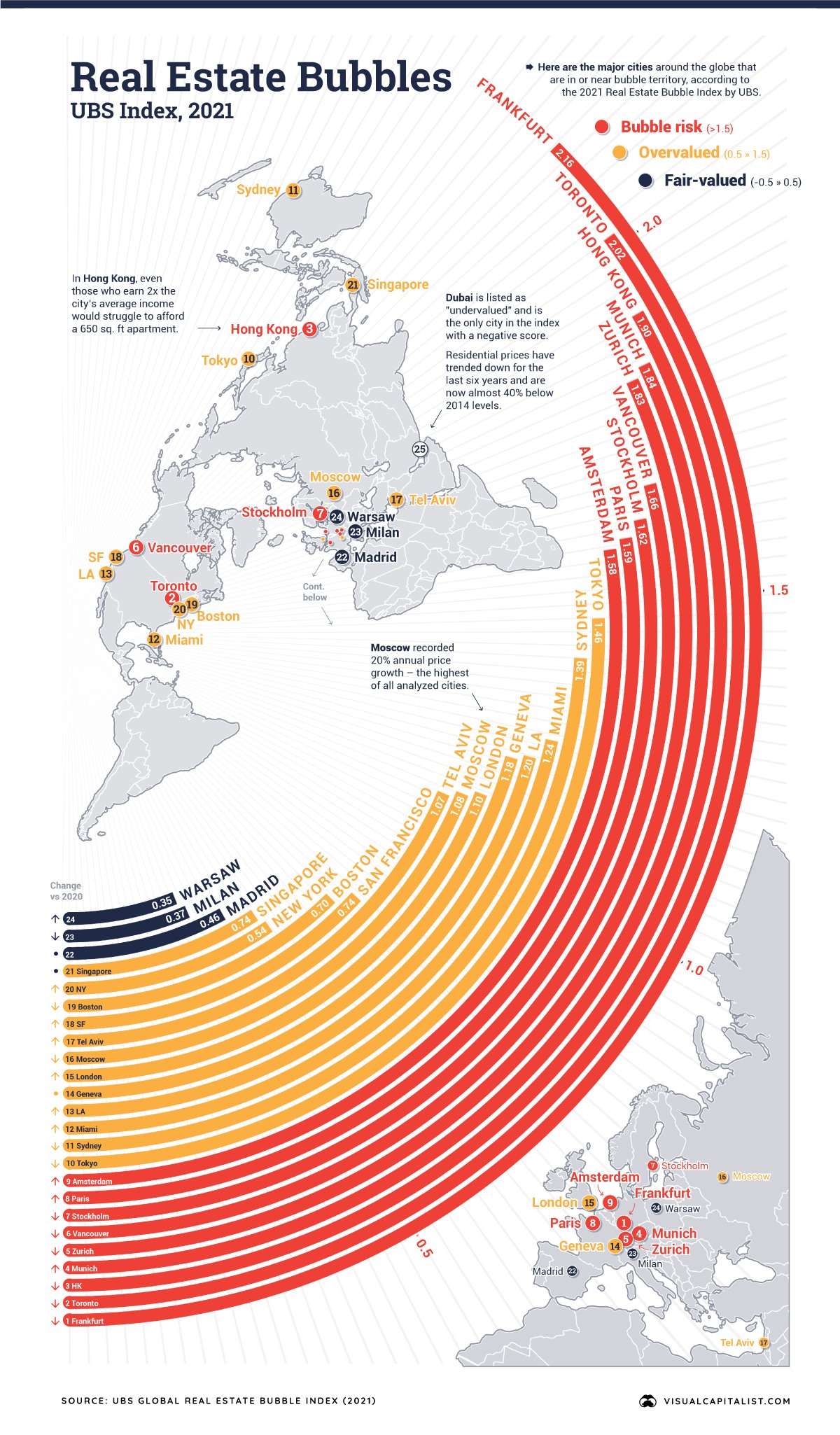

For the record, Toronto is believed to have the second biggest property bubble globally.

Globally Europe looks to be on the cusp of a serious recession. If North American central banks are looking too aggressive, Europe is struggling to chart a path for its shared currency. Rates have been at record lows but recently the ECB has said it will begin raising rates to tackle inflation. Across the continent the rate of inflation is over 8.1%, but it varies widely country to country, with Germany closer to the average, while Lithuania is at 22%. In the face of mounting inflation the ECB hasn’t raised rates once yet this year, though its expected to this month, even has the European economy and stock markets have been doing worse and worse.

Coincidentally, Germany, who is now both the linchpin in NATO support for Ukraine while simultaneously its weakest link, has seen its economic health crumble due to decisions made years ago to pin Germany’s energy needs to Russian energy supplies. Will Germany today be able to make political decisions that support NATO and the EU even if it means further economic pain for a country that has grown accustomed to being the beneficiary of these arrangements?

It is not just Western or developed nations that are struggling. China is in the middle of some kind of debt bubble in its real estate market, whose impact is harder to know, but will likely be long lasting given its size. Numerous developing nations are on the cusp of debt defaults, the tip of the iceberg being Sri Lanka.

A small island nation off the southern tip of India, Sri Lanka has been reasonably prosperous over the past few decades with an improving standard of living. Yet government mismanagement, graft and a haphazard experiment in organic farming have left the country destitute. Literally destitute. Out of money, gas and food. In the past few days protests have moved beyond general unrest into a full blown revolution, with the Sri Lankan people storming the government and the political leaders fleeing for their lives.

This year stands out for the complex problems that have grown out of the pandemic, but if we’re serious about the kinds of big problems politicians regularly say that must be tackled, then it raises a question as to whether we are handling them properly, or whether we are making mistakes given what we know right now.

For the last few years I have written or touched on many of these topics; on housing, inflation, crypto currencies and the fragile nature of many of our institutions. And while I am cautious about making grand predictions, it remains worth asking whether we are making smart choices given what we know, and if we are not we should be making greater demands of our elected leaders. And if our elected officials continue to make poor decisions, we as investors should plan accordingly.

Walker Wealth Management is a trade name of Aligned Capital Partners Inc. (ACPI)*

ACPI is regulated by the Investment Industry Regulatory Organization of Canada (www.iiroc.ca) and a Member of the Canadian Investor Protection Fund (www.cipf.ca). (Advisor Name) is registered to advise in (securities and/or mutual funds) to clients residing in (List Provinces).

This publication is for informational purposes only and shall not be construed to constitute any form of investment advice. The views expressed are those of the author and may not necessarily be those of ACPI. Opinions expressed are as of the date of this publication and are subject to change without notice and information has been compiled from sources believed to be reliable. This publication has been prepared for general circulation and without regard to the individual financial circumstances and objectives of persons who receive it. You should not act or rely on the information without seeking the advice of the appropriate professional.

Investment products are provided by ACPI and include, but are not limited to, mutual funds, stocks, and bonds. Non-securities related business includes, without limitation, fee-based financial planning services; estate and tax planning; tax return preparation services; advising in or selling any type of insurance product; any type of mortgage service. Accordingly, ACPI is not providing and does not supervise any of the above noted activities and you should not rely on ACPI for any review of any non-securities services provided by Adrian Walker.

Any investment products and services referred to herein are only available to investors in certain jurisdictions where they may be legally offered and to certain investors who are qualified according to the laws of the applicable jurisdiction. The information contained does not constitute an offer or solicitation to buy or sell any product or service. 16 Past performance is not indicative of future performance, future returns are not guaranteed, and a loss of principal may occur. Content may not be reproduced or copied by any means without the prior consent of the author and ACPI.

Amidst all the various news during this ongoing pandemic, reports that American billionaires are getting richer, particularly those focused in tech, is unlikely to bring anyone much comfort. Though much is often made of income inequality, I tend to believe that inequality in of itself is not a pressing concern for most people. What does stick in the minds of your average citizen is that no matter what tragedy seems to befall the world, the richest keep getting richer, while their own situation continues to erode.

There are two interconnected factors at play here. One is how billionaires continue to do so well. The other is related to declining fortunes and mobility for a middle class that is less middle, but increasingly more class orientated.

The rise of a super-rich has a great deal more to do the dominance of the stock market in an age of globalization than any other single factor. You’ve probably heard some statistic like this before, that in the past a CEO would only have made 20x more than their lowest paid employee, only to find now that the ratio is 278x more than the average worker. Much of this shift has been a result of moving compensation for CEOs and C-level executives into stock options, a move aimed at improving governance, but has instead hyper charged the importance of stock returns in an increasingly globalized world.

In his book Land of Promise by Michael Lind, he has this to say about globalization and global trade: “Between the end of the Cold War and the crash of 2008, globalization resulted in the organization of one global industry after another as an oligopoly, with most of the transnational enterprises headquartered in the United States, Europe, or Japan…Two companies, US-based Boeing and Europe’s Airbus, had 100 percent of the global market share in large jet airliners. Among their suppliers, the global market for jet engines was divided among three firms: GE, Pratt and Whitney, and Rolls-Royce. Microsoft enjoyed 90 percent of the global market share for PC operating systems. Four firms divided 55 percent of the PC market among themselves, while three companies shared 65 percent of the mobile handset phones. Three firms dominated the world market in agricultural equipment (69 percent) and ten companies dominated the global pharmaceutical market (69 percent). Ninety-five percent of microprocessors (chips) were made by four companies – Intel, Advanced Micro Devices, NEC, and Motorola. Four automobile companies – Gm, Ford, Toyota-Daihatsu, and DaimlerChrysler – manufactured 50% of all cars, while three firms – Bridgestone, Goodyear, and Michelin – made 60% of the tires. Owens-Illinois and Saint Gobin made two-thirds of all glass bottles in the world. Concentration in global finance was accelerated by US deregulation, which allowed the emergence of a small number of US megabanks, some of which grew even more during the Great Recession when, with the support of the US government, they absorbed failing banks, as Bank of America took over Merrill Lynch and JP Morgan Chase acquired Washington Mutual.”

However you may wish to slice it the system of globalization has been a huge boon to the wealthiest globally, consolidating wealth amongst an increasingly narrow group of companies and the people who own the bulk of the shares within those companies. And the more importance share holder returns have taken on, the more consolidated those companies have become.

The second problem I’ve mentioned is that of a middle class that is increasingly stratified. While the wealthiest keep getting wealthy, the middle class has followed suit, locking in wealth and reducing income mobility. While we may not consider life in the 1950s or 1960s particularly egalitarian, aspects about that more sexist and racist time in our past better facilitated economic mobility. For instance, a world where women did not hold many corporate positions of authority and didn’t work after marriage was also a world where women were more capable of “marrying up”. In contrast, today educated professionals marry other educated professionals. A surgeon is less likely to be married to a secretary and more likely to be married to another surgeon. The economist Tyler Cowen has called this “matching” in his book The Complacent Class, with people better able to “match” to those with similar interests and backgrounds. The effect of this “matching” has been to stratify wealth and decrease social mobility within the middle class.

Education represents another significant change that is stultifying the middle class. Education, particularly secondary education took on increasing importance in the 1980s, as those with university degrees started to out earn those with just high school, and those with professional designations (like lawyers and doctors) out paced those with just an undergraduate degree. Would more education fix this? Not really. As the cost of education continues to rise and new technologies filter into even white-collar jobs, young lawyers and accountants struggle to find work, while the management of major companies hangs in longer. The return on education continues to decline even as the costs go up, leaving those who come from wealthier educated families financially better off and better socially connected than those coming from lower income families trying leverage education into higher tax brackets.

Similarly, costs of living continue to climb in essentials. In Toronto, where housing prices have climbed steadily for the last two decades, it has given birth to an intransient NIMBYism. Homeowners, having taken on large amounts of debt to get into the housing market are generally protective of their neighborhoods and tend to push back hard on attempts to increase density for fear it pulls down housing value. Poorer neighborhoods in cities like Toronto find themselves pushed out by gentrification, an ironic blend of resistance to development that increases the price of living while denying the development that could keep prices lower for a more diverse group of residents to live together. The effect is one where neighborhoods may indeed be racially diverse, but not income diverse. The effect to a middle class is to be both more precarious and less open.

The response from governments to both these changes hasn’t been encouraging. Playing around with the tax rates, trying to force people into expensive four-year degrees, potentially embracing a universal basic income (UBI) amounts to tinkering with the system, not fixing it. And while UBI has garnered a lot of interest, it smacks of an acceptance of the current situation. If you can’t get ahead, here is some money to make life more tolerable. A population of people dependent of a government stipend is not a population that is very free. But if politicians efforts are well meaning, distrust of them remains understandable, as the political class and billionaire class rub elbows at places like Davos, recommitting to strengthening the very system that seems to be the source of many of the present issues.

Over the past several years I have dedicated this blog to the issues I think that remain most pressing from a financial standpoint to our society, frequently touching on issues of housing prices, technology, anti-urbanization, populism and the middle class. All these issues seem to be accelerating, and if there is a thought that might bind these ideas together it is a sense of loss of imagination on how we deal with major issues. In addition to a consolidation of corporate power and wealth amongst a smaller group of people, we also see fewer companies with IPOs, and fewer companies listed on the stock market in general. There is also less imagination from our political class, which remain wedded to a narrow set of ideas about how to deal with new problems.

Successful societies like Canada can be handcuffed by their past achievements, limiting options to things already tried before. But problems that do not get fixed don’t go away. Instead they fester, presenting themselves in other more threatening ways. As I write this there are riots in Minneapolis, ostensibly about the death of a citizen in police custody (part of a long list of Black Americans killed at the hands of police for nonviolent offences) but that riot has swiftly turned towards an affordable housing project and local big box stores in addition to the police. In a 2016 poll, only 30% of Americans born in the 1980s believed that living in a democracy is essential, the lowest since such polling had begun. In Europe polling showed that the core countries of the EU; Spain, France and Italy, had largely negative views about their current economic situation a decade on from the Great Recession.

Now, in the middle of this global pandemic, many of these fault lines are being exposed. There may be no better way to sum up our situation than to speak of Walmart, a store that exists and thrives because of the globalized order, importing products from China. According to Ian Bremmer, the largest employer among Fortune 500 companies is Walmart, employing 2.2 million people, easily out pacing any other single company. In 2003 the CEO of Walmart, H. Lee Scott, earned 1500 times as much as a full time Walmart employee.

This trend is not confined to Canada or the United States. It is global, and affects China and India as much as it does the West. But the effect on populations of an economic story that increasingly benefits the wealthiest, while making middle classes more precarious and defensive is to undermine the legitimacy of democracies. The backsliding of democratic countries, and the erosion of the international order is connected to these domestic economic challenges. The pandemic is speeding up this inequality effect, and how we rise to meet it will play a large roll in deciding who calls the shots in the 21st Century.

Author’s Note – In addition to the normally sourced articles I’ve relied on several books for this article, they include:

Plutocrats: The Rise of the New Global Super-Rich and the Fall of Everyone Else by Chrystia Freeland

The Retreat of Western Liberalism by Edward Luce

The Complacent Class by Tyler Cowen

Income Inequality, The Canadian Story (Volume 5), Edited by David A. Green, W. Craig Riddell and France St. Hilaire

Land of Promise by Michael Lind

Information in this commentary is for informational purposes only and not meant to be personalized investment advice. The content has been prepared by Adrian Walker from sources believed to be accurate. The opinions expressed are of the author and do not necessarily represent those of ACPI.

The economic fallout of the pandemic has garnered many shocking headlines, from concerns over how many restaurants may fail to the sheer number of people seeking unemployment insurance. Some of this is economic rubber necking, basking in the shocking and outlandish statistics generated by the lockdown and pandemic. The real test is still in front of us, determining what is temporary and what is permanent.

From the New York Times

Concern that a number of restaurants may not reopen seems a reasonable fear, since lots of restaurants don’t survive normally. The impact to the airline industry will take years to work out, since you can’t just put all those planes back in the sky. It will take time to determine which routes should be brought back first, how many people want to fly and the planes themselves will need considerable maintenance before any of them roll down a runway.

But hope springs eternal. Eight weeks into the lockdown and efforts remain underway to gradually reopen the economy, and in time we will see which parts of our society (not economy, but society) need real help to get back on its feet.

I remain largely optimistic about the speed of the recovery once it’s safe to reopen, but remain cautious regarding existing problems within the Canadian economy that the pandemic will likely accelerate. Problems that were hidden just under the surface will find themselves in the cold light of day, and those problems will have repercussions, many of which will not be easy to predict.

“Problems rarely exist in isolation, and a problem’s ability to fester, grow and become malignant to the health of the wider body requires an interconnected set of resources to allow its most pernicious aspects to be deferred. In Canada the problem has been long known about, a high level of personal debt that has grown unabated since we missed the worst of 2008. What has allowed this problem to become wide ranging is a banking system more than happy to continue to finance home ownership, a real estate industry convinced that real estate can not fail, and a political class that has been prepared to look the other way on multiple issues including short term rental accommodation, in favour of rising property values to offset stagnant wages”

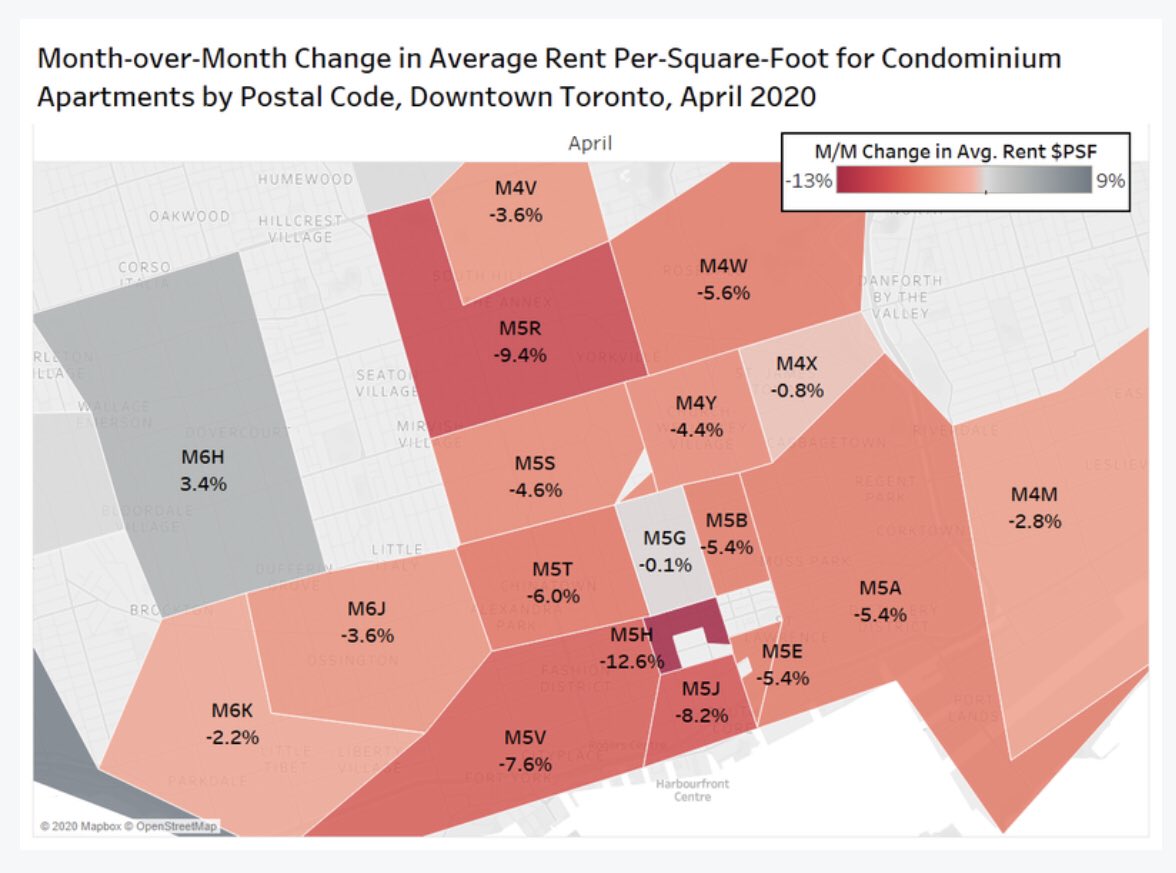

The issue of debt, real estate and short-term accommodations may be one issue undergoing a seismic shift in real time. The website MLS paints a surprisingly changed picture of the rental situation in downtown Toronto. Condominiums like the Ice Condos, located at the bottom of York Street were written about last year because so many of the units were being used for Airbnb. Today they offer hundreds of long-term rentals. The story is not limited to a few buildings either, much of the downtown condo scene, once reserved for Airbnb customers, has suddenly opened to long term accommodation.

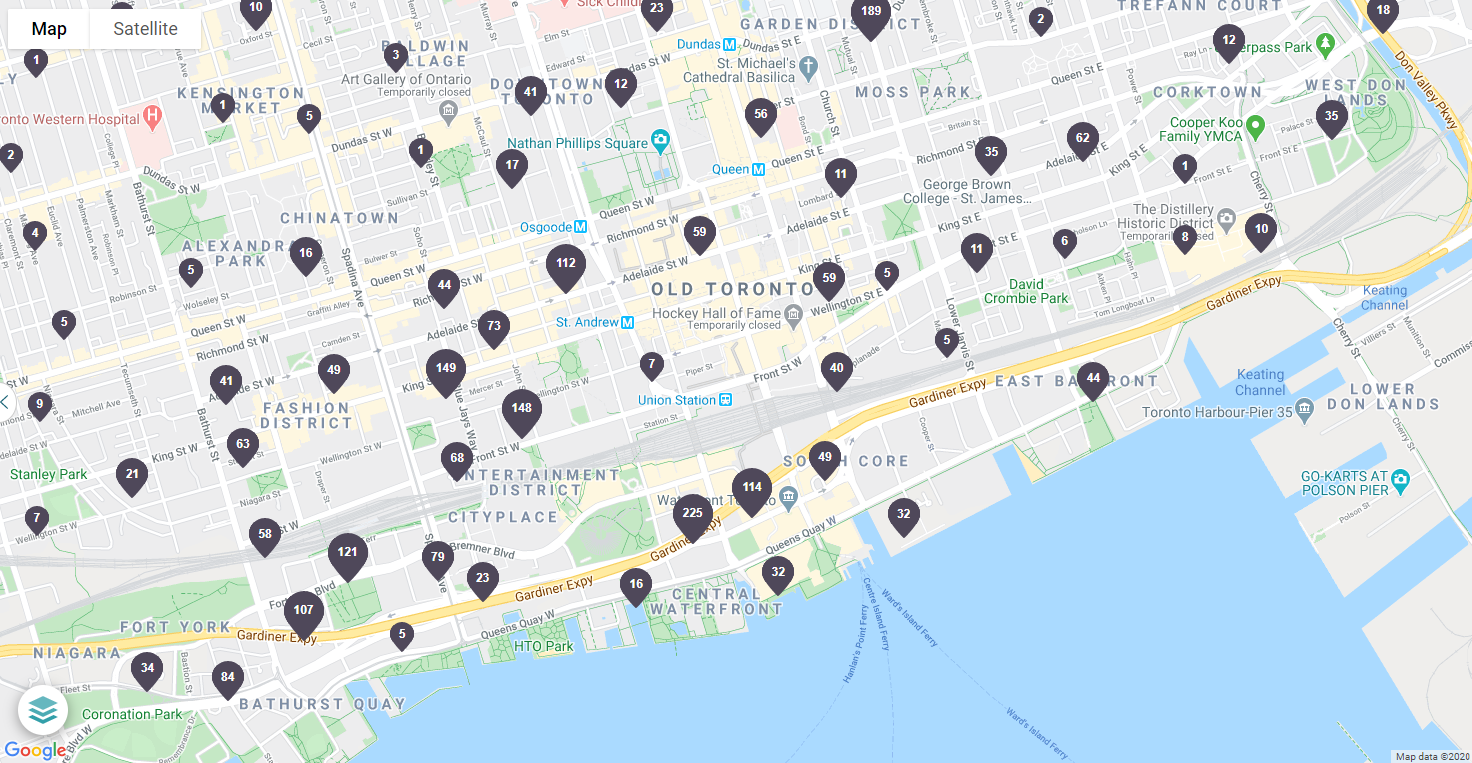

A snapshot of available rental in May 2020 in downtown Toronto

For a city that only a few months ago was running perpetually short of rentals this change has been rapid, but its fair to assume that many of these landlords are hoping that the crisis will pass and that things will return to normal, with lucrative business in short term rentals resuming. The effect of all these new rentals is not happening in a vacuum. According to Rentals.ca in their May 2020 report, the price of condo rentals in locations like the Ice Condos have dropped by 10%.

It is here that we should stop and consider a reality. In a few short weeks two major sectors of the Canadian economy within the city of Toronto (and Vancouver for that matter) have been radically altered. But this is also a period where we have seen the most government support and extensive economic intervention. Long term expectations have yet to shift. Airbnb hosts wish to remain Airbnb hosts. Homeowners hope to continue to use their houses to expand their financial footprint. But we should take a page from the city of Toronto reviewing its financial books, the real crisis has yet to truly unfold.

Our future contains, but has yet to have pass, the retreat of government financial support. It has yet to put people back to work, yet to reopen universities, yet to ramp up our manufacturing base, yet to know much of anything about moving past Covid-19. Clarity about what governments should or should not do are hindered by China’s resistance to openness and transparency, while other nations that have already faced the pandemic and seemed to recover are running into second waves. There is no clarity about the future.

Real estate remains at the heart of the Canadian economic story for the last 20 years. Appreciating housing prices are the chief source for growth in Canadian families’ net worth. Borrowing to buy houses and borrowing against home equity remain our chief sources of debt. Our politics revolves around the tension of needing more housing in certain highly desirable areas while preserving those areas from over development. That dynamic has revolved around a status quo that seemed to have no conceivable end. The pandemic may have radically altered the Canadian real estate landscape regardless of how people feel about it or what they want. Whether we can walk back changes of this magnitude remains very much unknowable. For now we can only watch the changes our society and economy are undergoing and hope that what we are witnessing will be for the best, those changes that have happened, and those yet to come.

Information in this commentary is for informational purposes only and not meant to be personalized investment advice. The content has been prepared by Adrian Walker from sources believed to be accurate. The opinions expressed are of the author and do not necessarily represent those of ACPI.

I‘ve just had a chance to watch the movie The Big Short, based on the book of the same name by Michael Lewis. Michael Lewis has made a name for himself as a writer for being able to explain complex issues, often involving sophisticated math that befuddles the general population but is responsible for much of the financial chaos that has defined the last decade.

The principle of our story is Dr. Michael Burry, a shrewd investor whose unique personal qualities gives him the patience to tear apart one of the most complicated financial structures in modern finance. Having done that he creates a new market for a few people who had the foresight to see the US housing bubble and how far the crash might reach. The story is captivating and the tension builds to what we know is the inevitable conclusion of the worlds biggest crash, but there is a problem with the story.

No matter what they do in the movie, we know how it all ends. That hindsight undercuts the real tension in the film, the risk that these few traders and hedge fund managers took with other people’s money to bet against what were largely considered to be safe investments. In some ways, the US housing crash is unique because of how much institutionalized corruption had seeped into the system. The ratings agencies who sold their AAA ratings for the business, the mortgage brokers who pushed through unfit candidates into subprime adjustable rate mortgages, the analysts and financial specialists that repackaged low grade mortgages into AAA rated bonds; it took all of them and more to create the biggest market bubble since the South Sea.

Their smart move seems like lock, but if you look past the drama the heroic brokers of our story were taking a huge gamble with other people’s money. From Dr. Michael Burry down through the rest of the characters, hundreds of millions, billions even, were tied up in investments that few understood but carried incredible potential for losses. The confidence that our heroes show in demanding “half a billion more” as they come to understand the scope of the problem seem smart in hindsight, but they were making big bets. Bets that could have easily ruined people’s lives and finances.

This is the true nature of risk. Things are only certain in hindsight. At the moment we need to make decisions rarely do we possess the kind of clarity that we believe we should have when dealing with markets. If we look to current markets what can we honestly say we know about tomorrow? Markets are chaotic, oil prices are in the tank, central bankers are talking about negative interest rates (while some have gone and done it), and then we will have 2 or 3 days of market rallies. What picture should we draw from this? What certainty do we have about tomorrow’s performance?

From Bloomberg

Our problem is that when we are inclined towards certainty we are also inclined towards fantastic risk. In fact we won’t even believe there is risk if we are certain of an outcome. And we are prone to lionizing people who risk it all and are proved to be right, while forgetting all those people who made similar gambles and lost everything, leading us to repeat a mistake that has undone many.

The story we need isn’t the one about the people who bet big and won. We need the story about the people who bet smart and navigated confusing and risky markets and came out fine. That story sadly won’t have the kind of impact or drama that we long for in a movie, but it’s the story that each and every investor should want to be part of.

Politics is personal and we are not in the game of telling you who to vote for, nor are we endorsing one party over another. These are our thoughts about three issues we find relevant to what we do on your behalf and how we look at the market.

Despite however sophisticated we may think we are, elections are still a confusing mess of promises, accusations and distractions. And making sense of what has been promised is quite difficult. Take for example the Liberals promise for an additional $20 billion in transit infrastructure spending over the next decade. That sounds great and will no doubt be welcome, but that works out to $2 billion a year nation wide (it is not being proposed to be allocated that way, but for simplicity purposes this will do). The cost of the controversial Toronto subway expansion is likely to exceed the $3.56 billion currently budgeted. Given the huge cost of transit infrastructure I’m at a loss to know how much difference $2 billion a year make across the country. Its a big sum, but I don’t know what it’s worth and I’d wager neither do you.

There are a lot of issues in this election, but some that could have a meaningful impact on your investments and retirement savings, and I thought I’d share some thoughts on them.

TFSAs

Tax Free Savings Accounts have been a popular new tool for investing since they were introduced in 2009. Originally allowing for a $5000 per year contribution, then raised to $5500 and finally to $10,000 per year in 2015, the Liberals and the NDP have both vowed to roll back the increased contribution room to the more modest $5500 arguing that the room only benefits the wealthy. I have previously written that I think this is a bad argument and that TFSAs are a valuable tool for saving regardless of income. Obviously the Conservatives have promised to keep the contribution levels where they currently are, and notably there has been no discussion yet as to how a roll back would affect existing contributions and future contribution room, nor how the CRA would track this year.

Pension & Income Splitting

Pension splitting has been reaffirmed as a necessary and vital tool for retirees by all the parties. Conservatives, Liberals and the NDP have sought to reassure Canada’s most reliable voting block seniors that pension splitting will remain a part of their income options. In a telling move that illustrates how cynical perhaps our politics are and who will reliably turn up to vote, pension splitting will stay, but the NDP and Liberals would like to see income splitting go.

Income splitting, if I’m being honest, makes a lot of sense to me. Designed to help families with a large income earner and where one parent stays at home to raise children, it balances taxes paid where a two income family would pay less even though their combined incomes are equal to one large earner. The tax benefit is only open to families with children under 18 and capped at $2000, so it isn’t a necessarily huge tax write-off.

Interestingly, the argument against income splitting isn’t a great one. According to the Liberals (and backed up by independent think tanks) the tax credit is really only available to about 15% of Canadian households, and so by that logic alone has been described as a $2 billion tax break for the rich. My math suggests otherwise.

According to the 2011 census, there are just over 13 million private households in Canada. Couples with children account for more than 3 million of those households (3,524,915) or around 28%. That means (and I’ll admit I may have this wrong) eligible families for income splitting account for more than half of all households with children. So the idea that it isn’t a useful or widely available tax credit may not be as accurate as portrayed given who it is targeting.

Housing

As you know, I hate Canadian housing, (but love talking about it). It’s a known disaster waiting to happen that consistently defies odds and makes everybody nervous. But while it’s where Canadians have accumulated the greatest amount of debt it hasn’t really been an election issue. The importance of reducing the cost of housing hasn’t really been recognized either. There are efforts from all parties to create more affordable housing, but that isn’t the same thing.

To this end both the Conservatives and the Liberals have brought some terrible ideas to the forefront. Conservatives have made their once temporary home renovation tax credit permanent, although they’ve cut it’s value in half to $5000 from the original $10,000 and have pledged to increase the maximum you can borrow from the Home Buyers Plan. The Liberals are offering to allow you to dip into the First Time Home Buyers plan more than once. Neither of these plans are great. The housing market is too hot and encouraging the use of RRSPs (you know, your private retirement savings) to encourage more homeownership highlights the complicity of Canada’s government in the soaring debt levels of Canadian families.

In the end we may long for a political party that advised caution against further home ownership in a country where it is already at record highs, and one of the highest in the developed world. Just a reminder, the view of the government is that while high debt is a natural byproduct of low rates, too much debt will still be your fault.

We aren’t trying to influence your vote, but we think it is important to understand that underneath the bluster and mudslinging are policies which can directly impact the financial well-being of Canada, and Canadians like you. So please remember, on October 19th, vote!

I can not find a better metaphor for Canada’s housing market than this image from the movie UP! (Which is a film I highly recommend)

If you’re looking for some good reading Google “Canadian Housing Bubble” and you could fill a library with the amount of material available. There isn’t a week that goes by without some new article somewhere screaming with alarm about Canada’s precarious and overvalued housing market. I’ve written many myself, but in conversation almost everyone admits that regardless of the danger nothing seems to abate the growth in home values.

The history of the average five year mortgage in Canada going back to the mid 1960s. It’s hard to believe that Canadians once paid interest rates in excess of 20% to buy a home. Today rates are at an all time low and unlikely to rise anytime soon. From the Globe and Mail, published May 13, 2015

This defying of financial gravity gives ammunition to those that doubt there is any real risk at all. The combination of low interest rates, willing banks, rising prices and an aggressive housing market has given a veneer of stability to an otherwise risky situation. Combined with the “sky is falling” talk about the house prices and it is easy to understand why many simply accept, or outright dismiss, the growing chorus of concerns about house prices.

Nissam Taleb’s book “The Black Swan” highlighted that negative Black Swan events tended to be fast, like 2008, while positive Black Swan events tended to be slow moving, like the progressive improvement in standards of living since the end of the Second World War. But it would be fair to say that creating a negative event requires a prolonged period of danger creep, a period where a known danger continues to grow but remains benign, fooling many to believe that there isn’t any real danger at all.

I would argue we are living in such a period now. The housing market is continuing to grow more precarious and many Canadians are finding that their own financial well being is connected to their home’s appreciating value. Between large mortgages and HELOCs, Canadians are deeply indebted and need their home prices to continue to inflate to offset the absurd level of borrowing that is going on.

As an example of how the “danger creeps” have a look at this article from last week’s Globe and Mail which highlights a young couple living in Mississauga with a burdensome debt and an unexpected pregnancy. They are classified as some of the “most indebted” of Canadians; house rich and cash poor. By their own estimates they are over budget every month and 100% of one of their incomes goes exclusively to pay the mortgage, stressful as that is they aren’t worried. It may seem irresponsible on their part to buy such a home, but they couldn’t do it if there weren’t many others complicit in making such a bad financial arrangement. Between lax rules from the government, a willing lending officer and well intentioned families that help out, it turns out that creating a financially fragile family takes a village.

A nation of debtors is a vulnerable one indeed. I’ve often said that financial strength comes through being able to withstand financial shocks, and this is exactly where Canadians are falling short. It’s the high debt load and minimal savings (and that these two issues are self-reinforcing) that make Canadians vulnerable. A change in the economic fortunes would force many Canadians to deleverage and in the process would inflict further damage to the economy and likely many homes onto the market.

Such an event is strictly in the “uncharted seas” sector of the economy. No one has a clear idea what it would take to shift the housing sector loose, or what would happen once it did. And that’s just the unknown stuff. With interest rates at an all time low it would also only take a small increase in the interest rate (say 2%) to bump up many people out of their once affordable mortgage and into unaffordable territory.

That’s the problem with slow growing danger, it has a glacial pace but when it arrives it is already too large to be dealt with easily. In one of my favorite movies, the Usual Suspects, Kevin Spacey utters the line “The greatest trick the devil ever pulled was convincing the world he didn’t exist”. That’s something we should all be wary of, the longer the housing market stays aloft the more convinced we become that not only is it not dangerous, but that there was never any danger at all.

Last week I published a piece on the dangers of the housing bubble in Canada. It caused a stir with a number of clients and followed many articles over the past two years about our concerns with the Canadian economy.

But on Wednesday I was at an industry lunch with another group of advisors talking about the Canadian housing market and was met with a curious objection over whether there was any real danger at all. Another advisor happily pointed out to me that while the indebtedness of Canadians may be high, it is still affordable, and we should be mindful of the famous investors you have been hoisted by their own doom saying petards.

While it’s true that many doom saying predictions don’t come to pass and we should be careful before signing on to one particular points of view, arguing that lots of debt is affordable and therefore no threat is similar to a drug addict arguing everything is under control because they still hold down a job. The job is irrelevant to the problem, although it’s absence is likely to make matters worse.

This is why it is somewhat irrelevant to worry about the Canadian housing market. Whether you believe there will be a soft landing, a hard landing or no landing at all, what Canadians have is a debt problem. Only it’s not a problem because it’s affordable. Also it’s a problem.

If that last sentence is confusing, don’t worry. It sounds worse coming from the Bank of Canada, who in their December Financial Systems Review pointed out that debt levels continue to climb but the relative affordability of the debt remains consistent. And while an economic shock to the system could make much of that debt unserviceable, for now that seems unlikely. They concluded this section of the report identifying the risk to Canadians as “elevated”.

How to best handle this problem will have to be left to others. There is no simple solution that will not trigger the bomb, and the goal of any government is to slowly reduce the average debt burden without hurting the economy or deflating the bubble. For my part I tend to advise people to pay their debts down, shy away from things they cannot afford and encourage saving rather than debt spending to limit risk. When it comes to saving for the future there is no reason to make many people’s problems your problems.

This past week I received an article from a client regarding ideas about “wealth preservation” that made some good sense, and offered advice about calculating how much money you need for retirement. But while the premise was sound; that it makes sense to pursue investment strategies that protect your nest egg when your financial needs are already met, a one off comment about the future of the stock market caught my attention.

You can read the article HERE, but the issue I wanted to look at was the not so subtle implication that the US markets were now due for a correction. A serious one. Quoting the Wall Street Journal contributing writer William J. Berstein,

“In March, the current bull market will be six years old. It might run an additional six years—or end in April.”

This isn’t the first time I’ve heard this point before. It isn’t unique and sits on top of many other market predictioner’s tools, but its use of averages gives a veneer of knowledge the writer simply doesn’t possess.

Obviously we would all like to know when a market correction is due, and it would be great to know how to sidestep the kind of volatility that sets our retirement savings back. But despite mountains of data, some of the most sophisticated computers, university professors, mathematicians and portfolio managers have yet to crack any pattern or code that would reveal when a market correction or crash should be expected.

Which is why we still rely on rules of thumb like the one mentioned above. Is the age of a bull market a good indication of when we will have a correction? Probably not as good of one as the writer intends. Counting since 1871, the average duration of a bull market is around 4.5 years, making the current bull run old. But averages are misleading. For instance the bull markets that started in 1975, and 1988 (ending in 1987 and 2000 respectively) lasted for 153 months each, or just shy of 13 years. Those markets are outliers in the history of bull markets, but their inclusion in factoring the average duration of the bull markets extends the average by an additional year. Interestingly if you only count bull markets since the end of the second world war the average length is just over 8 years, but that would only matter if you think our modern economy has significant differences from an economy that relied on sailing vessels and horses.

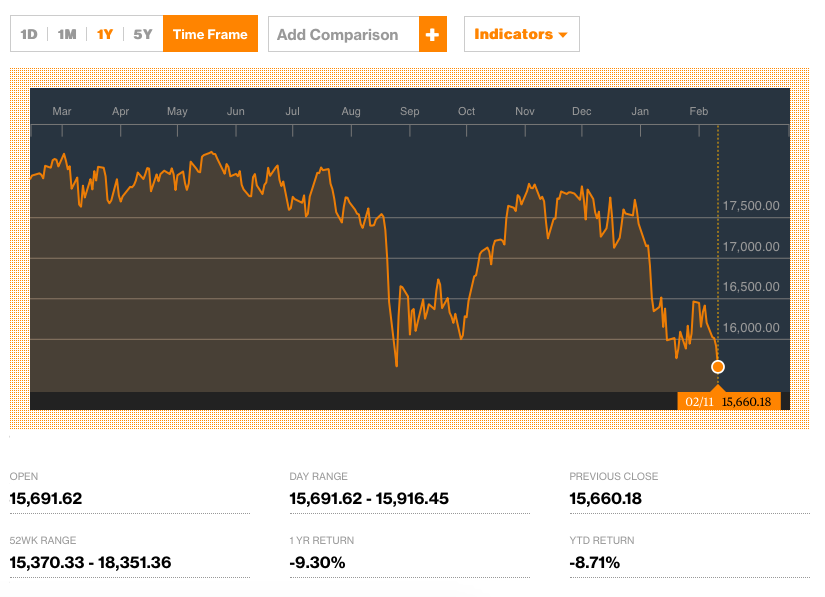

Last Friday I watched the TSX start to take a precipitous fall. The one stock market that seemed immune to any bad news and had easily outperformed almost every other index this year had suddenly shed 200 points in a day.

Big sell-offs are common in investing. They happen periodically and can be triggered by anything, or nothing. A large company can release some disappointing news and it makes investors nervous about similar companies that they hold, and suddenly we have a cascade effect as “tourist” investors begin fleeing their investments in droves.

This past week has seen a broad sell-off across all sectors of the market in Canada, with Financials (Read: Banks), Materials (Read: Mining) and Energy (Read: Oil) all down several percentage points. In the course of 5 days the TSX lost 5% of its YTD growth. That’s considerable movement, but if you were looking to find out why the TSX had dropped so much so quickly you would be hard pressed to find any useful information. What had changed about the Canadian banks that RBC (RY) was down 2% in September? Or that TD Bank (TD) was down nearly 5% in a month? Oil and gas were similarly effected, many energy stocks and pipeline providers found themselves looking at steep drops over the last month. Enbridge (ENB) saw significant losses in their stock value, as did other energy companies, big and small, like Crew Energy (CR).

The S&P TSX over the last five days

All this begs the question, what changed? The answer is nothing. Markets can be distorted by momentum investors looking to pile on to the next hot stock or industry, and we can quibble about whether or not we think the TSX is over valued by some measure. But if you were looking for some specific reason that would suggest that there was something fundamentally flawed about these companies you aren’t going to have any luck finding it. Sometimes markets are down because investors are nervous, and that’s all there is to it.

Market panic can be good for investors if you stick to a strong investment discipline, namely keeping your wits about you. Down markets means buying opportunities and only temporary losses. It help separates the real investors from the tourists, and can be a useful reminder about market risk.

So was last Friday the start of a big correction for Canada? My gut says no. The global recovery, while slow and subject to international turmoil, is real. Markets are going to continue to recover, and we’ve yet to see a big expansion in the economy as companies deploy the enormous cash reserves they have been hoarding since 2009. In addition, the general trend in financial news in the United States is still very positive, and much of that news has yet to be reflected in the market. There have even been tentative signs of easing tensions between Russia and the Ukraine, which bodes well for Europe. In fact, as I write this the TSX is up just over 100 points, and while that may not mean a return to its previous highs for the year I wouldn’t be surprised if we see substantial recoveries from the high quality companies whose growth is dependent on global markets.

Education represents another significant change that is stultifying the middle class. Education, particularly secondary education took on increasing importance in the 1980s, as those with university degrees started to out earn those with just high school, and those with professional designations (like lawyers and doctors) out paced those with just an undergraduate degree. Would more education fix this? Not really. As the cost of education continues to rise and new technologies filter into even white-collar jobs, young lawyers and accountants struggle to find work, while the management of major companies hangs in longer. The return on education continues to decline even as the costs go up, leaving those who come from wealthier educated families financially better off and better socially connected than those coming from lower income families trying leverage education into higher tax brackets.

Education represents another significant change that is stultifying the middle class. Education, particularly secondary education took on increasing importance in the 1980s, as those with university degrees started to out earn those with just high school, and those with professional designations (like lawyers and doctors) out paced those with just an undergraduate degree. Would more education fix this? Not really. As the cost of education continues to rise and new technologies filter into even white-collar jobs, young lawyers and accountants struggle to find work, while the management of major companies hangs in longer. The return on education continues to decline even as the costs go up, leaving those who come from wealthier educated families financially better off and better socially connected than those coming from lower income families trying leverage education into higher tax brackets.

Real estate remains at the heart of the Canadian economic story for the last 20 years. Appreciating housing prices are the chief source for growth in Canadian families’ net worth. Borrowing to buy houses and borrowing against home equity remain our chief sources of debt. Our politics revolves around the tension of needing more housing in certain highly desirable areas while preserving those areas from over development. That dynamic has revolved around a status quo that seemed to have no conceivable end. The pandemic may have radically altered the Canadian real estate landscape regardless of how people feel about it or what they want. Whether we can walk back changes of this magnitude remains very much unknowable. For now we can only watch the changes our society and economy are undergoing and hope that what we are witnessing will be for the best, those changes that have happened, and those yet to come.

Real estate remains at the heart of the Canadian economic story for the last 20 years. Appreciating housing prices are the chief source for growth in Canadian families’ net worth. Borrowing to buy houses and borrowing against home equity remain our chief sources of debt. Our politics revolves around the tension of needing more housing in certain highly desirable areas while preserving those areas from over development. That dynamic has revolved around a status quo that seemed to have no conceivable end. The pandemic may have radically altered the Canadian real estate landscape regardless of how people feel about it or what they want. Whether we can walk back changes of this magnitude remains very much unknowable. For now we can only watch the changes our society and economy are undergoing and hope that what we are witnessing will be for the best, those changes that have happened, and those yet to come. ‘ve just had a chance to watch the movie The Big Short, based on the

‘ve just had a chance to watch the movie The Big Short, based on the