Politics is personal and we are not in the game of telling you who to vote for, nor are we endorsing one party over another. These are our thoughts about three issues we find relevant to what we do on your behalf and how we look at the market.

Despite however sophisticated we may think we are, elections are still a confusing mess of promises, accusations and distractions. And making sense of what has been promised is quite difficult. Take for example the Liberals promise for an additional $20 billion in transit infrastructure spending over the next decade. That sounds great and will no doubt be welcome, but that works out to $2 billion a year nation wide (it is not being proposed to be allocated that way, but for simplicity purposes this will do). The cost of the controversial Toronto subway expansion is likely to exceed the $3.56 billion currently budgeted. Given the huge cost of transit infrastructure I’m at a loss to know how much difference $2 billion a year make across the country. Its a big sum, but I don’t know what it’s worth and I’d wager neither do you.

For this reason elections regularly fall victim to the desire of political parties and the media for an easier story to tell. And disappointingly this election spent far too much time talking about the niqab, an issue that, despite how you may feel, has only affected two people since the 2011 ban was first introduced.

There are a lot of issues in this election, but some that could have a meaningful impact on your investments and retirement savings, and I thought I’d share some thoughts on them.

TFSAs

Tax Free Savings Accounts have been a popular new tool for investing since they were introduced in 2009. Originally allowing for a $5000 per year contribution, then raised to $5500 and finally to $10,000 per year in 2015, the Liberals and the NDP have both vowed to roll back the increased contribution room to the more modest $5500 arguing that the room only benefits the wealthy. I have previously written that I think this is a bad argument and that TFSAs are a valuable tool for saving regardless of income. Obviously the Conservatives have promised to keep the contribution levels where they currently are, and notably there has been no discussion yet as to how a roll back would affect existing contributions and future contribution room, nor how the CRA would track this year.

Pension & Income Splitting

Pension splitting has been reaffirmed as a necessary and vital tool for retirees by all the parties. Conservatives, Liberals and the NDP have sought to reassure Canada’s most reliable voting block seniors that pension splitting will remain a part of their income options. In a telling move that illustrates how cynical perhaps our politics are and who will reliably turn up to vote, pension splitting will stay, but the NDP and Liberals would like to see income splitting go.

Income splitting, if I’m being honest, makes a lot of sense to me. Designed to help families with a large income earner and where one parent stays at home to raise children, it balances taxes paid where a two income family would pay less even though their combined incomes are equal to one large earner. The tax benefit is only open to families with children under 18 and capped at $2000, so it isn’t a necessarily huge tax write-off.

Interestingly, the argument against income splitting isn’t a great one. According to the Liberals (and backed up by independent think tanks) the tax credit is really only available to about 15% of Canadian households, and so by that logic alone has been described as a $2 billion tax break for the rich. My math suggests otherwise.

According to the 2011 census, there are just over 13 million private households in Canada. Couples with children account for more than 3 million of those households (3,524,915) or around 28%. That means (and I’ll admit I may have this wrong) eligible families for income splitting account for more than half of all households with children. So the idea that it isn’t a useful or widely available tax credit may not be as accurate as portrayed given who it is targeting.

Housing

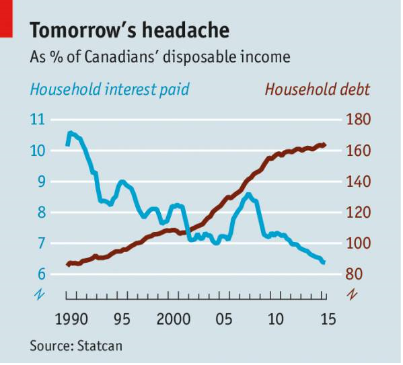

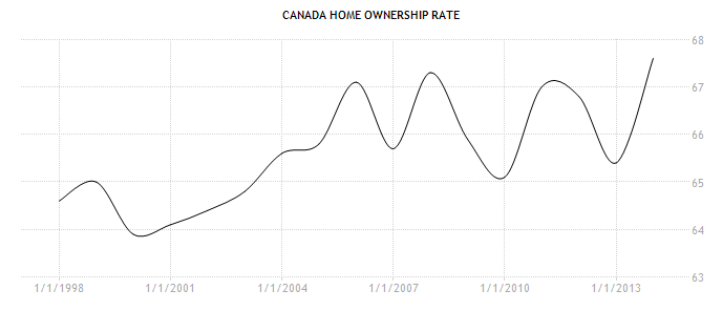

As you know, I hate Canadian housing, (but love talking about it). It’s a known disaster waiting to happen that consistently defies odds and makes everybody nervous. But while it’s where Canadians have accumulated the greatest amount of debt it hasn’t really been an election issue. The importance of reducing the cost of housing hasn’t really been recognized either. There are efforts from all parties to create more affordable housing, but that isn’t the same thing.

As you know, I hate Canadian housing, (but love talking about it). It’s a known disaster waiting to happen that consistently defies odds and makes everybody nervous. But while it’s where Canadians have accumulated the greatest amount of debt it hasn’t really been an election issue. The importance of reducing the cost of housing hasn’t really been recognized either. There are efforts from all parties to create more affordable housing, but that isn’t the same thing.

https://twitter.com/Walker_Report/status/655065283007225856

To this end both the Conservatives and the Liberals have brought some terrible ideas to the forefront. Conservatives have made their once temporary home renovation tax credit permanent, although they’ve cut it’s value in half to $5000 from the original $10,000 and have pledged to increase the maximum you can borrow from the Home Buyers Plan. The Liberals are offering to allow you to dip into the First Time Home Buyers plan more than once. Neither of these plans are great. The housing market is too hot and encouraging the use of RRSPs (you know, your private retirement savings) to encourage more homeownership highlights the complicity of Canada’s government in the soaring debt levels of Canadian families.

In the end we may long for a political party that advised caution against further home ownership in a country where it is already at record highs, and one of the highest in the developed world. Just a reminder, the view of the government is that while high debt is a natural byproduct of low rates, too much debt will still be your fault.

https://twitter.com/Walker_Report/status/654734014243205124

We aren’t trying to influence your vote, but we think it is important to understand that underneath the bluster and mudslinging are policies which can directly impact the financial well-being of Canada, and Canadians like you. So please remember, on October 19th, vote!