All year people have been expecting a correction in the US Markets. For most of the year I have listened to portfolio managers discuss their “concern” about the high valuations of American companies. I have also listened to them point out that America remains the strongest economy and the most likely to see significant growth in the coming year.

All year people have been expecting a correction in the US Markets. For most of the year I have listened to portfolio managers discuss their “concern” about the high valuations of American companies. I have also listened to them point out that America remains the strongest economy and the most likely to see significant growth in the coming year.

Flash forward to late-September, early October and the markets have finally had their corrections. At the bottom every market was negative, including the TSX which had given up all of its YTD high of 15%. That was the bottom. The recovery was swift, money flowed back into the markets, and hedge fund managers managed to make a mockery of some otherwise nervous DIY investors. Now the markets look strong again, with the S&P 500 reaching new highs. Nobody is happy.

All of this comes on the news that US GDP was up 3.9% in the third quarter, a full .5% above analyst expectations (that sounds small, but it’s worth billions) while energy prices continue to decline, manufacturing is highly competitive and US consumers look poised for a significant Christmas bonanza. So what’s wrong with this picture? Why are both the Globe and Mail and the Financial Times worried about the US stock market?

https://twitter.com/Walker_Report/status/537581249440014337

The answer is a combination of fear, data, and the insatiable need for stories to populate the media everyday. First is the fear. Stocks are at all time highs. The problem is that “all time high” isn’t some automatic death sentence for a stock market. The stock market always hits new highs all the time, and a by-product of that is that corrections can really only happen after a high is reached. Look at the history of the S&P 500 since 1960:

As you can probably tell, there are a lot of “new highs” that had occurred over the last 40 years, but each new high did not automatically translate into some automatic correction. There were legitimate reasons why the economy could continue to grow, and in the process make those companies in the stock market more valuable. That isn’t to say that the stock market can’t be “frothy” or that their aren’t problems in the stock market today. It merely means that setting a new market high isn’t proof of an impending collapse.

As you can probably tell, there are a lot of “new highs” that had occurred over the last 40 years, but each new high did not automatically translate into some automatic correction. There were legitimate reasons why the economy could continue to grow, and in the process make those companies in the stock market more valuable. That isn’t to say that the stock market can’t be “frothy” or that their aren’t problems in the stock market today. It merely means that setting a new market high isn’t proof of an impending collapse.

The second issue is data. We live in an age of Big Data. Data is everywhere and there is so much it can be hard to separate the useful data from the useless. Some of the data is concrete, but much of it takes time to understand or even become clear. The first analysis of the higher than expected GDP numbers seemed great (more economy, Yay!) but upon closer inspection, there are reasons to be cautious. While the GDP was higher than expected, it was largely due to growth in government spending, not consumer spending. In fact consumer spending was lower quarter over quarter. In addition there are a number of concerns about how corporations are spending their profits and whether that is sustainable. Many of these concerns, when taken in context, seem to be the same from earlier in the year.

The third factor is the insatiable need to write something. Content is king in the news world and providing insight (read: opinion) means that you must constantly produce new stories to publish. That means that there is a need to be constantly suggesting that things are about to go wrong (or more wrong than they already have) to create a compelling story. It isn’t that these stories are wrong, just that constantly saying the stock market is going to go down isn’t insightful, since at some point we can expect the stock market to correct for one of a number of reasons.

So is America frothy? Are we poised an some kind of financial collapse? I don’t know, and nobody else does either. We are no more likely to correctly know when the market might correct again than we are to guess the future price of gas. The best response is to diversify, and remember some core elements of investing. Buy low and sell high. With that in mind sturdy investors should probably start giving the beat-up and maligned Europe a second look…

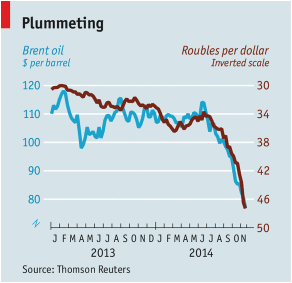

The answer has everything to do with the rising levels of oil production in the United States combined with what federal regulators are willing to do to encourage new growth.

The answer has everything to do with the rising levels of oil production in the United States combined with what federal regulators are willing to do to encourage new growth.

On more than one occasion I have been quizzed about the future of some stock market-or-other to the lack of satisfaction of the quizzer. Invariably the conversation goes something like: “What with all the money being printed and the new highs of the stock market, shouldn’t it all come down?” And my answer is usually, “No.”

On more than one occasion I have been quizzed about the future of some stock market-or-other to the lack of satisfaction of the quizzer. Invariably the conversation goes something like: “What with all the money being printed and the new highs of the stock market, shouldn’t it all come down?” And my answer is usually, “No.”