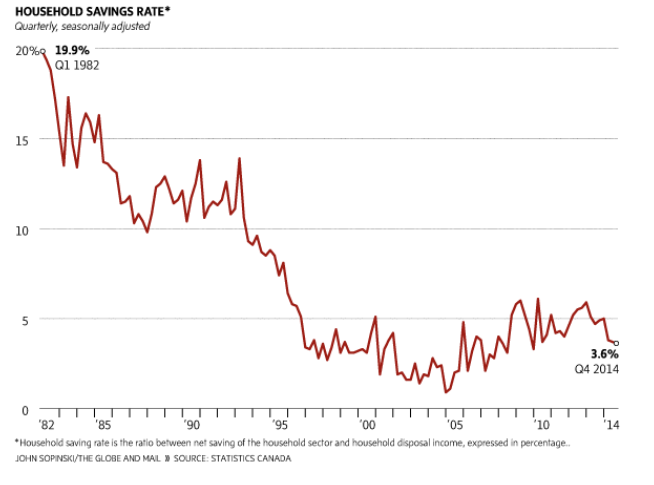

It is a common enough trope that people do not save enough, either for retirement or just generally in life. We are a society awash in debt, with some estimates showing Canadians carrying an astonishing $27000 of non-mortgage debt and an average of three credit cards. This financial misalignment, between how much we spend (bad) and how much we save (good) is a source of not just economic angst, but denouncements of sinfulness and failings of moral behavior.

This isn’t an exclusively Canadian problem. Pretty much everyone across the developed world has been accused of both not saving enough and carrying too much debt, and the remedy is usually the same, save more and spend less. Underneath that simplistic advice is the nuance that goes into managing money; the importance of paying down debt, of saving some of what you earn on payday (so you don’t see it) and a host of other little things that define good money habits.

But for young people trying to save and spend less they may find that the struggle is far greater than anticipated and the advice they are given can be frustrating in its obtuseness. For instance, one of the first solutions financial gurus give is “cut back on the lattes”. In one of our first articles we ever wrote was about the “Latte Effect”, (That Latte Makes You Look Poor) and how the math that underlies such advice, while not bad, isn’t going to fund a retirement.

In fact cutting costs is extremely difficult. Vox.com recently offered some advice for saving more. Pointing out that big ticket items are more useful in cost cutting than small items, the article made the improbable suggestion to “consider moving to a cheaper metropolitan area” if you are finding San Francisco or New York too expensive. Seriously. As though living in cities was a choice exclusively connected to cost, or that Minneapolis was simply New York with similar opportunities but cheaper.

In Canada this advice falls even flatter. While you can live many places, not all offer similar opportunities. Living in Windsor means (typically) making

cars. Thunder Bay offers both lumber production and a Bombardier plant. But if you are part of the 78% of Canadian GDP that is connected to the service sector, either through banking, finance, health services, government, retail, or high tech industries you are likely in one of four major cities, Toronto, Vancouver, Calgary or Montreal. It should be no surprise that young Canadians, facing ever increasing house prices haven’t actually abandoned major cities for “cheaper alternatives” since most of the jobs tend to be concentrated there.

So for young Canadians the challenge is quite clear. Cutting back on your expensive coffees could save you between $1000 – $2000 per year, but that won’t get you far in your retirement. Serious changes to costs of living are challenging since the biggest cost of living in cities is frequently paying for where you want to live. In between these extremes we can find some sound advice about budgeting and restraining what you spend, but it is fair to say that many young people aren’t saving because they enjoy spending their money, but because they don’t yet have enough money to cover their major costs and maintain a lifestyle that we generally aspire to.

So for young Canadians the challenge is quite clear. Cutting back on your expensive coffees could save you between $1000 – $2000 per year, but that won’t get you far in your retirement. Serious changes to costs of living are challenging since the biggest cost of living in cities is frequently paying for where you want to live. In between these extremes we can find some sound advice about budgeting and restraining what you spend, but it is fair to say that many young people aren’t saving because they enjoy spending their money, but because they don’t yet have enough money to cover their major costs and maintain a lifestyle that we generally aspire to.

It’s worth noting that most financial advice is pretty good and sensible, even things like watching how much you spend on coffee. Credit cards, lines of credit and overdrafts are all best avoided if possible. A solid budget that allows you to clearly see your spending habits won’t go amiss. And if you do choose to spend less on the small luxuries, it isn’t enough that the money stays in your purse or wallet. It must go somewhere so it can be both out of reach and working on your behalf or you risk spending it somewhere else.

But it is financially foolish to assume that people don’t want to save. The Globe and Mail recently ran a profile on the blogger “Mr. Money Mustache” – a man who retired at 30 with his wife and claims that the solution to retiring young is to wage an endless war on wasteful spending. And he means it. Reading his blog is like reading the mind of an engineer. From how he thinks about his food budget, to what cars you own, his advice is both sound and confounding. It might be best summed up as “live like your (great) grandparents”. Sound advice? Absolutely! Confounding? You bet, since the growth in the economy and our standard of living exists precisely because we don’t want to live like our grandparents.

There is no good solution or answer here. Young Canadians face a host of challenges on top of all the regular ones that get passed down. Raising a family and buying a home are complicated by financial peer pressure and inflated house prices. Choosing sensible strategies for saving money or paying down debt (or both) often means getting conflicting advice. And young Canadians have no assurances that incomes will rise faster than their costs, nor can they simply relax about money. They must be vigilant all the time and avoid financial pitfalls that are practically encouraged by the financial industry. Finding balance amidst all this is challenging, and young Canadians should be forgiven that they find today’s world more financially difficult than the generation previous.