A series of bad days, a moment of respite, and then more selling. This was the story of 2008, and it lasted for months. The rout lasted until finally investors felt that enough was going to be done to save the economy that people stopped selling. Massive quantitative easing, an interest rate at 0%, aggressive fund transfers, bailouts to whole industries, and the election of a president who seemed to embody the idea of “hyper competence”. That’s what it took to save the economy in 2008. Big money, an unconditional promise to save businesses and people, and the rejection of a political party that oversaw the bungled early handling of a crisis and had lost the public confidence.

I don’t think Donald Trump has never had been viewed as hyper competent. I doubt even his most ardent supporters see him as incredibly clever, but instead a thumb in the eye of “elites” who have never cared to take their concerns seriously, and to an establishment that seemed incapable of making politics work. Trump was a rejection of the status quo and a “disruptor in chief”. A TV game show host who played the role of America’s most sacrosanct character, the self made man, asked now to play the same role in politics.

There’s nothing I need to cover here you don’t already know. A history of bad business dealings, likely foreign collusion to win an election, surrounded by sycophants and yes men with little interest or understanding of the machines they have been put in charge of, and an endless supply of criminal charges. Like a dictator his closest advisors are members of his own family, and perhaps more shockingly he fawns over and publicly admires the dedications of respect other dictators get from their oppressed populations. Never has a person been so naked in their desires and shortfalls as Donald Trump.

Markets have played along with this charade because Trump seemed, if anything, largely harmless to them. Indifference to the larger operation of the government and the laser like focus on reduced regulations and tax cuts made Trump agreeable to the Wall Street set. If he could simply avoid a war and keep the economy humming, Trump was a liveable consequence of “good times”. Until the coronavirus issue, Trump had not done terribly. The economy wasn’t exactly humming. It had a bad limp due to a trade war with China. It had a chest cold because wealth inequality was continuing to worsen despite decreasing unemployment. And its general faculties were diminished as issues around health care, deficit spending, and other aspects of the society began to languish. But as far as unhealthy bodies go, the American economy still had its ever strong beating heart, the American consumer.

Whatever name you prefer; COVID-19, the coronavirus, SARS-CoV-2, or the #Chinesevirus (as Trump is now busy trying to get it renamed) has exposed the fault lines in the administration and the danger of such blinkered thinking by Wall Street. Having spent the last few weeks downplaying the severity of the outbreak and hoping China would be able to contain it, until finally, grudgingly, acknowledging its seriousness. Markets have suddenly come face to face with a problem that bluster and bravado can’t fix. Trump is a political liability for markets, and his leadership style, which is heavy on cashing in on good times with little management for rainy days, means that markets may not really have any faith that he can properly address these problems.

Other efforts to calm markets, largely through the federal reserve, have not reassured anyone. Two emergency rate cuts are not going to fix the economy but did spook investors globally (it did signal to banks that they should take loans to cover potential shortfalls). The promise of a massive set of repo loans to provide liquidity will keep markets open and lubricated, but again won’t save jobs and won’t prop up the physical economy. What will fix markets is an end to the pandemic, a problem with the very blunt solutions of “social distancing”, “self isolation” and the distant hope of a vaccine.

What investors are facing are three big problems. First, that we don’t know when the virus will be contained. Optimistically it could be a month. Realistically it could be three. Pessimistically people are talking about the rest of the year. Even under the best conditions we are also likely facing a recession in most parts of the globe, and even then stimulus spending and financial help won’t be as effective until people can leave their homes and partake in the wider market (postponing tax filings and allowing deferrals on mortgages are good policies for right now, but at some point we need to spend money on things). But the last problem is one of politics. The Trump administration is uniquely incompetent, has shown little interest in the mechanisms of government, and in a particularly vicious form of having something come back to bite you, dismantled the CDC’s pandemic response team.

The best news came last week, when it seemed a switch had been flicked and the general population suddenly grasped the urgency of the situation and people began self isolating and limiting social engagements (I am now discounting Florida from this statement). Those measures have only been strengthened by government action over the last few days. Similarly, while I write this, Trudeau has announced a comprehensive financial package to come to the aid of small businesses and Canadian families. All this is welcome news, and I expect to see more like this over the coming weeks as Western governments take a more robust and wide ranging response to the crisis. So there is just one issue still unaddressed. The political mess in Washington.

I can’t say that markets will improve if Trump is voted out of office, but its hard to imagine that they could be made worse by his exit. Markets, and the investors that drive them, are emotional and it is confidence, the belief that things will be better tomorrow, that allow people to invest. Trump promised a return to “good times”, to Make America Great Again, and it is his unique failings that have left it, if anything, poorer.

Information in this commentary is for informational purposes only and not meant to be personalized investment advice. The content has been prepared by Adrian Walker from sources believed to be accurate. The opinions expressed are of the author and do not necessarily represent those of ACPI.

As proof that the robot revolution will spare no one, even our industry is feeling the intense weight of cheap human alternatives in the form of “robo-advisors”. Given some glowing press by the Globe and Mail over the last weekend, robot advisors now represent a real and growing segment of the financial services markets and are forcing many advisors, including us, to ask how they and we will live together and what our respective roles will be.

As proof that the robot revolution will spare no one, even our industry is feeling the intense weight of cheap human alternatives in the form of “robo-advisors”. Given some glowing press by the Globe and Mail over the last weekend, robot advisors now represent a real and growing segment of the financial services markets and are forcing many advisors, including us, to ask how they and we will live together and what our respective roles will be. To say that robo-advisors are a hot topic among financial advisers is to understate the collective paranoia of an industry that has come to see itself as besieged with critical and often unfair press. We haven’t been to a conference, meeting or industry event that doesn’t at some point involve financial advisors attempting to rationalize away the looming presence of cheap and impersonal financial advice. While there are some good questions that get asked at these events, there is a whiff of denial that must have given false hope to autoworkers in the 80s and 90s in these conversations.

To say that robo-advisors are a hot topic among financial advisers is to understate the collective paranoia of an industry that has come to see itself as besieged with critical and often unfair press. We haven’t been to a conference, meeting or industry event that doesn’t at some point involve financial advisors attempting to rationalize away the looming presence of cheap and impersonal financial advice. While there are some good questions that get asked at these events, there is a whiff of denial that must have given false hope to autoworkers in the 80s and 90s in these conversations.

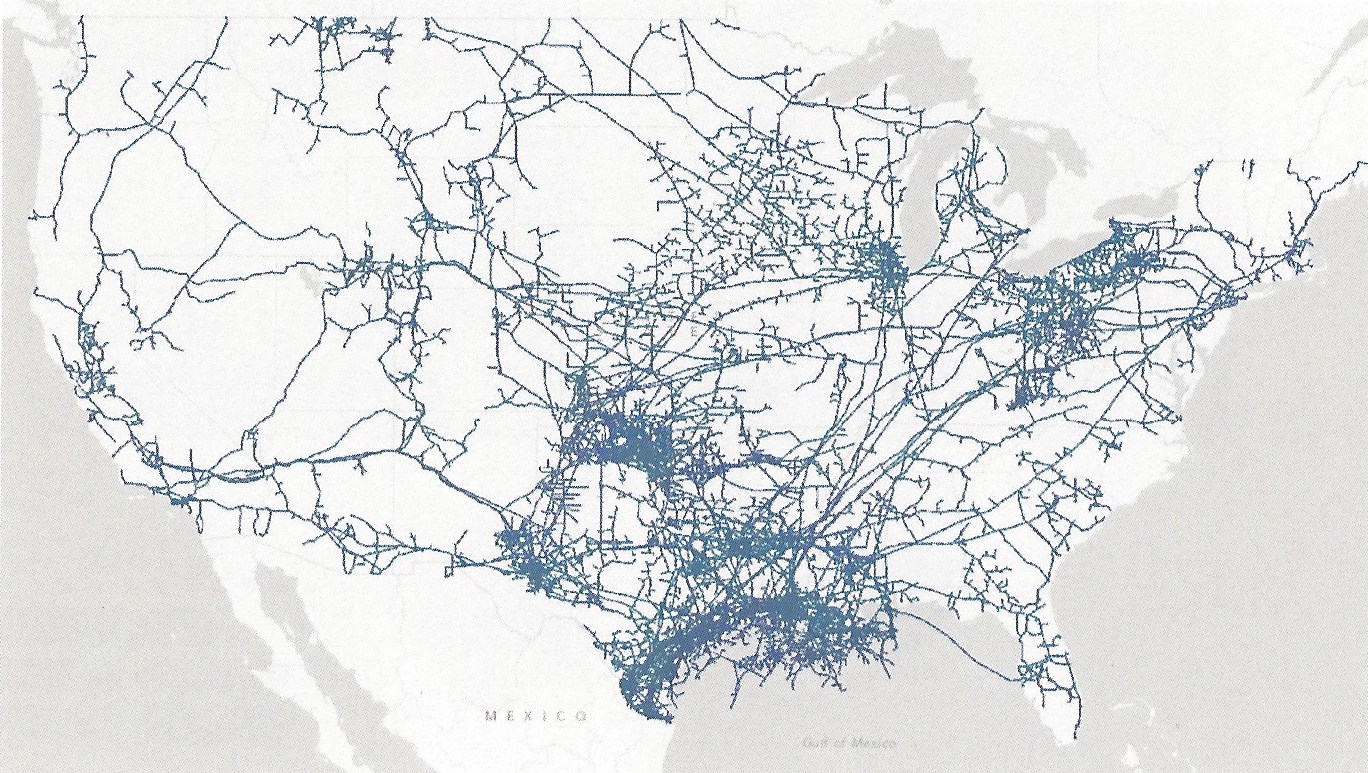

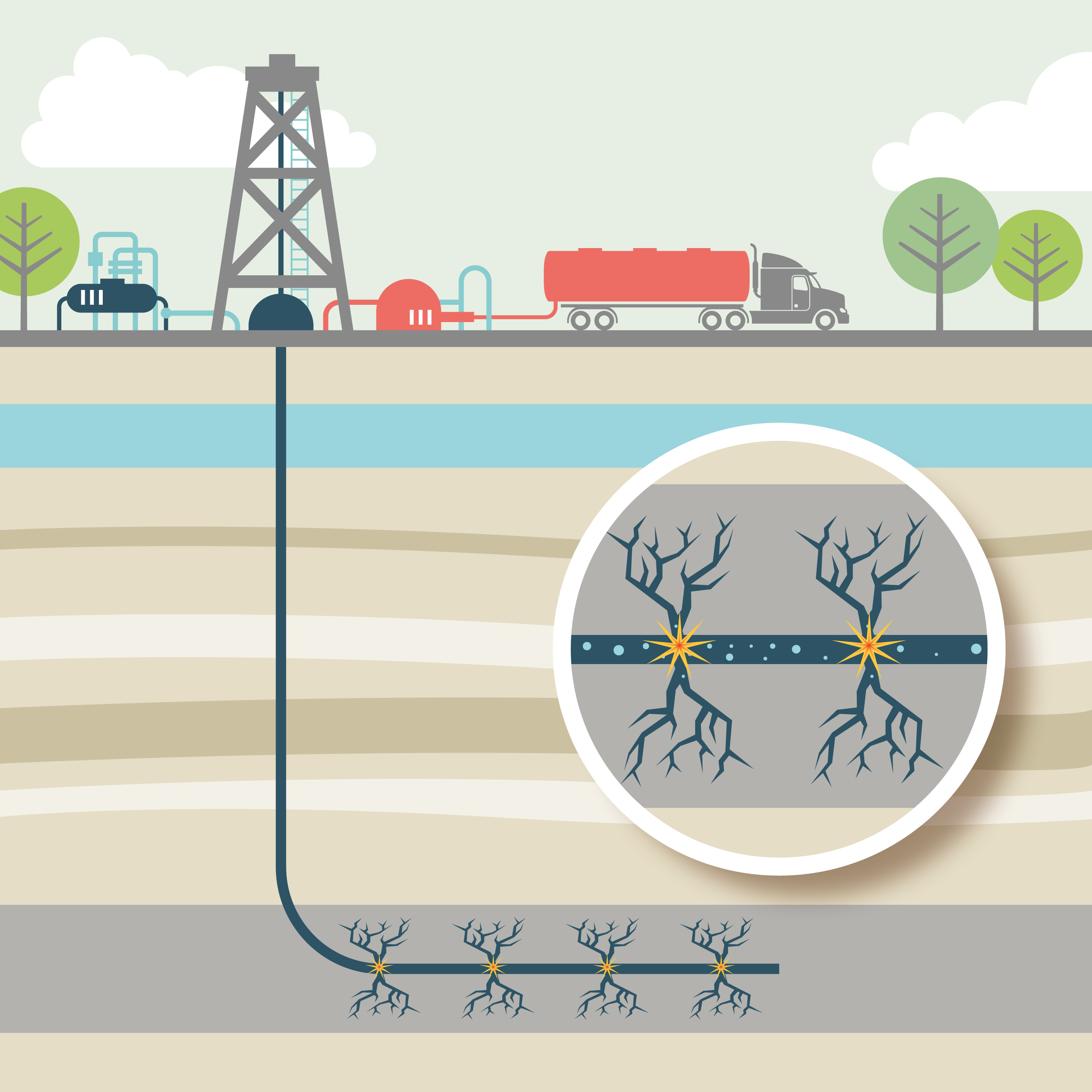

The answer has everything to do with the rising levels of oil production in the United States combined with what federal regulators are willing to do to encourage new growth.

The answer has everything to do with the rising levels of oil production in the United States combined with what federal regulators are willing to do to encourage new growth.