Tesla is all over the news. Most recently I have seen several postings about the new P85D Tesla’s Insane Mode, a setting in the car that delivers the maximum amount of power to the car (a big thanks to my client who sent me the link).

Tesla is all over the news. Most recently I have seen several postings about the new P85D Tesla’s Insane Mode, a setting in the car that delivers the maximum amount of power to the car (a big thanks to my client who sent me the link).

Tesla, and it’s CEO Elon Musk (who is a real life bond villain) has made quite a splash, building a high quality and competitive electric car with a solid range. A real first. And while his current offerings in the market remain decidedly high end, his ambitions include creating a more affordable middle class version as well.

But the economics of electric vehicles remain challenging at best. There are more options than ever, from Chevrolet, to Ford to Toyota. But these cars all tip the scales at the upper end of the car market, and are not sensible economically on a three year lease.

Awesome, right?

But the problem for electric cars may be best explained by the new Formula E series that is currently in it’s inaugural season. Using a newly designed electric race car I was surprised to learn that there are limits on the power that drivers can use in races, (while fans can vote to give some drivers an addition 50 bhp to boost speed each race via twitter). Why is this? Ostensibly it is to help preserve the life of the battery, already the heaviest part of the car and not powerful enough to get a car through a single race without a second car. In other words, the economics of the battery is still the biggest challenge facing all auto producers.

By some good fortune my brother in law is a driver in Formula E for team Mahindra. Mahindra & Mahindra isn’t as well known in Canada, but is a large conglomerate and a significant auto producer that sells in many countries. This past year they have launched India’s first electric passenger vehicle, the Reva e2o, which they had loaned to Karun and afforded me the opportunity to test drive while visiting my extended family in India. It’s a good car, and I could see that Karun had enjoyed driving it. But he pointed out the first challenge to electric cars in India was that the Indian government is only just introducing an electric car subsidy (having previously canceled one in 2012). In fact it is government subsidies that have helped foster the boom in electric cars.

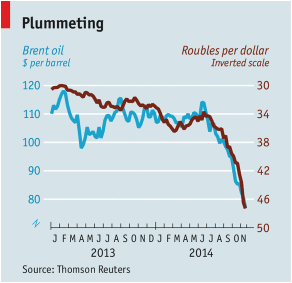

What this all leads to is the inevitable challenge poised by the sudden drop in the price of oil. Electric cars sit at the top of the market in terms of cost, and many aren’t even viable until after you both:

- Don’t have to buy gas anymore when oil is over $100 a barrel.

- Are given money by the government to help afford the car.

So if high gas prices underly the business case for electric cars, then a sudden cut in the price of oil does significant damage to that business case. It makes traditional petrol cars more cost effective, more competitive and more profitable compared to their e counterparts.

This tells us two things about oil and electric cars. The first is that while oil prices may stay depressed compared to previous market highs, the demand for oil is unlikely to decline and will likely recover as cheap oil spurs economic growth. The second issue is whether the rise of companies like Tesla is overstated. As exciting as they may appear, the market valuation of TESLA is the real insane mode, and certainly not in line with a traditional auto maker. The reality at least is that the end of oil, and the growth of electric cars is going to be dependent on considerable innovations in battery technology and will not be viable in the long term with cheaper oil and government subsidies. But who knows, next year’s Formula E series will allow teams to design their own cars and we may begin seeing some interesting innovations start in battery development.

The answer has everything to do with the rising levels of oil production in the United States combined with what federal regulators are willing to do to encourage new growth.

The answer has everything to do with the rising levels of oil production in the United States combined with what federal regulators are willing to do to encourage new growth.